I'm trying to find the right balance between ETFs and individual stocks.

My long-term goal is to build wealth steadily over the next 20–30 years, while still owning a handful of individual companies that I believe in.

Over time, I'd also like to shift my portfolio towards a stronger dividend focus, without sacrificing too much long-term growth.

Looking at this portfolio:

- Is there anything that stands out to you?

- Are there any positions you think are unnecessary, overweight, or missing?

I invest €3,500 every month through my ETF savings plan:

$VWRL (+0,12%) = 800 euro

$WSML (-0,29%) = 300 euro

$PRAM (-0,13%) = 300 euro

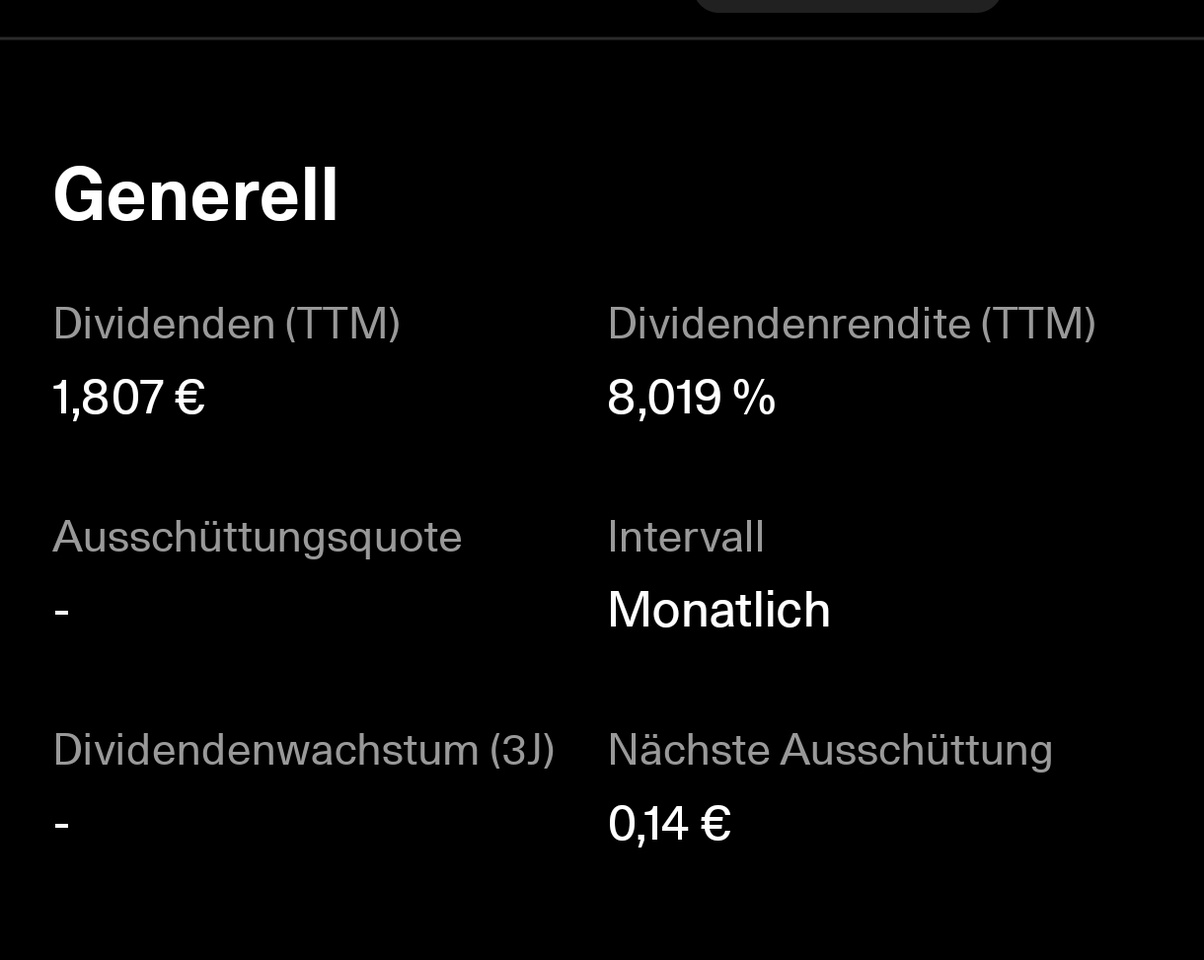

$JEGP (+0,56%) = 325 euro

$STHE (-0,01%) = 325 euro

$BTCE (+0,33%) = 100 euro

$SDIP (+0,06%) = 300 euro

$WINC (+0,04%) = 350 euro

$LDGL (-0,22%) = 350 euro

$TDIV (-0,22%) = 350 euro

What would you change first, and why?

Always interested in constructive feedback.