$BAYN (+1,64 %)

$LDO (+2,92 %)

$FCT (+0,55 %)

$VOW (+0,03 %)

$SAN (-0,71 %)

$VWRL (+1,67 %)

$ENI (-1,33 %)

$SHEL (-1,39 %)

$KO (-0,51 %)

$ISP (+0,48 %)

$INTC (+7,92 %)

$SL (+1,4 %)

$GOOGL (+2,02 %) .

SL

Sanlorenzo

Action

Action

ISIN: IT0003549422

Ticker: SL

IT0003549422

SL

Price

Discussion sur SL

Postes

112Sem.·

Portfolio Update

18Positions

9 195,48 €

17,77 %

33

6Mo·

Sanlorenzo: strong numbers behind a premium luxury story

Sanlorenzo stands out not just for its brand, but for the quality of its financials, which in my view justify a bullish stance on the stock.

Over the last few years, the company has delivered double-digit revenue growth, with annual sales now well above €800 million and a clear trajectory toward the €1 billion mark. What matters even more is profitability: EBITDA margins have consistently moved into the mid- to high-teens, a strong result for a company operating in a highly customized manufacturing business.

The order backlog is another key strength. Sanlorenzo typically reports a backlog covering more than one year of production, providing strong revenue visibility and reducing short-term cyclicality risk. This is not a company selling hope — it is selling yachts already contracted.

Cash generation is solid. Operating cash flow remains positive even during periods of heavy investment, while net debt is under control. In some years, leverage has remained close to 1x EBITDA or below, giving management flexibility to invest, pay dividends and absorb potential macro slowdowns.

Return on capital is also attractive. ROIC levels comfortably above the cost of capital indicate that growth is value-accretive, not just growth for the sake of size. This is a crucial point in luxury manufacturing.

Finally, valuation. Despite its quality and growth profile, Sanlorenzo has often traded at lower multiples than global luxury peers, especially when adjusted for balance sheet strength and backlog visibility. For a company combining premium pricing, strong margins and disciplined execution, this creates an appealing risk-reward profile.

In my view, Sanlorenzo is not a cyclical trade — it is a high-quality luxury compounder backed by real numbers.

👉 Do you think the market is still underestimating Sanlorenzo’s ability to compound earnings over the next cycle?

1313

8Mo·

What is risk? My strategy and portfolio - and your recommendations!

Everyone perceives risks individually. Everyone tries to independently assess the risk of a share or the current economic situation on the stock market.

In portfolio theory, risk is primarily measured using the standard deviation. In simple terms, this is the extent to which a share price moves. If this movement is correlated with the "market", this results in a beta. If this is < 1 bedeutet das, dass der Kurs einer Aktie geringer als der Markt schwankt. > 1, the result is a disproportionate fluctuation. The "market" is an elastic term. For example, an MSCI World, S&P 500 or the DAX can be used as a reference. The result is different betas depending on the index. However, I do not want to go into this topic any further at this point.

Why beta is not relevant for me

- Price fluctuations are not a problem in my current life situation (24 years old; student).

- Every share that grows faster than the market has a beta > 1. As my portfolio is set to grow, a high beta is desirable.

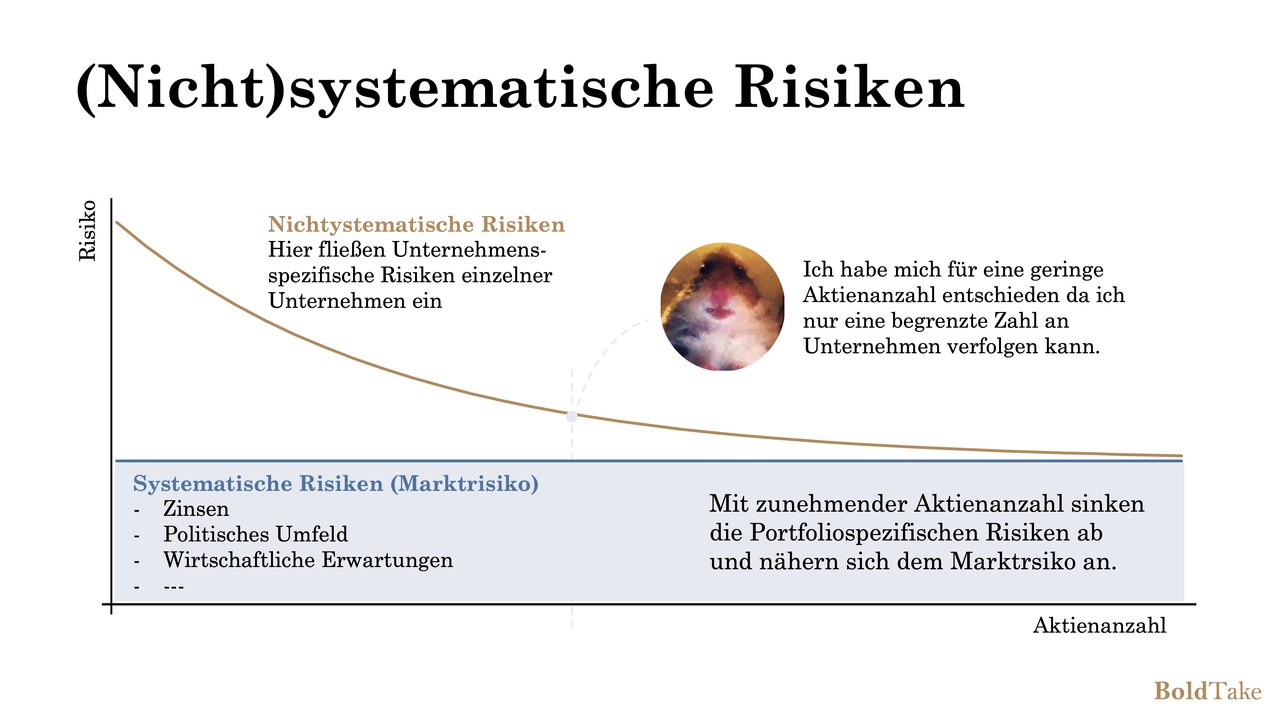

Diversification as a risk?

I often see portfolios with 30+ companies on Getquin. The aim behind this is to minimize risk. In my view, however, what gets lost in the process is the overview - or leisure time, because every share in the portfolio should be tracked and scrutinized.

I have therefore opted for a clearly structured portfolio. There are currently 11 companies (but the number is not set in stone). There are two reasons for this:

I want to know and follow each company in my portfolio well

The impact of a price increase should be significant

My strategy for less drawdown despite fewer shares

- Cover as many sectors as possible

- Consider regional sales distribution

- Know a company as well as possible

Why these companies?

- Heidelberg Materials $HEI (+0,94 %). Local monopolies with strong pricing power

- Medpace$MEDP (+0,1 %). Enabler of small research/pharma teams. Enables research outside of Big Pharma

- Hims and Hers$HIMS (+3,54 %). Generics seller with "cool brand". Enables better margins in the long term.

- MercadoLibre $MELI (-0,62 %). The Amazon and bank of Latin America. To benefit from the rise of emerging markets.

- Meta Platforms$META (-0,36 %). Monopoly in communication/social media.

- Prada$1913 (+2,5 %). One of the few luxury companies that is constantly growing (and not highly valued). More on this in my last post.

- BATS$BATS (-0,83 %). Non-cyclical business model. Bought at the time due to significant undervaluation. Now I hold the share to stabilize the portfolio somewhat.

- Sanlorenzo$SL (+1,4 %). Yacht manufacturer and thus part of the luxury sector, which I find attractive due to its high margin and low cyclicality.

- Solaria $SLR (+1,31 %). My conservative bet on rising energy demand through AI.

- Metaplanet $3350 (-2,85 %). Bitcoin gamble with play money.

My criteria for buying shares

Basically, I hardly set myself any limits when investing. I like to invest in shares that are rather unpopular at the time of purchase. The sector doesn't matter, although I prefer high-margin business models.

I like to buy cheap - high P/E ratios put me off (even if FOMO sometimes kicks in). I don't feel comfortable with it because of the potential drop.

Wow. Thank you for reading this!

Now that you know my strategy, I would really appreciate some stock tips tips, that could fit my strategy.

By the way, can you see the portfolio? Because it's my own post I can't check it👀

11Positions

90,88 %

1111

11 Commentaires

TheWorst@TheWorst

8Mo

•

22

•Afficher la réponse

9Mo·

Diversify with few shares

In my opinion, you can diversify at these levels:

Local (by headquarters, by turnover)

By currency

By industry

By company size (influences volatility)

I try to have as little overlap as possible in several areas in order to keep my portfolio robust.

Example:

$DRO (+13,15 %) and $PARRO (+2,43 %) : Similar industry, so both are driven by the same news, but have different locations and currencies.

$CACI (+2,02 %) Also has some correlation with the two, but is mainly dependent on the movements of the US military.

$8001 (+1,87 %) As a boring anchor

$SL (+1,4 %) As a "real" luxury play to profit from rising inequality and to have more euro/Italy in the portfolio.

$GRE (+0,45 %) Because I see great potential in Greece, see old post

9Positions

23 359,63 €

11,20 %

11Mo·

A nearly one year review

Hi everyone!

I’ve been building this portfolio for almost a year now, following a long-term growth approach rather than chasing short-term explosive gains. So far, it’s up +5.30%. I’ve focused more on the italian and american markets with stoks such as $ISP (+0,48 %)

$KO (-0,51 %)

$BRK.B (+0,46 %) that make more than half my portfolio. What do you think about my strategy and approach?

$VOW3 (+0,17 %)

$PLTR (+13,75 %)

$FCT (+0,55 %)

$LDO (+2,92 %)

$RHM (+1,28 %)

$INTC (+7,92 %)

$CPR (-1,68 %)

$AXP (+0,83 %)

$BMPS (+1,25 %)

$FBK (+1,59 %)

$G (+0,44 %)

$GS (+2,45 %)

$MCD (-0,11 %)

$SL (+1,4 %)

$ENI (-1,33 %)

$BBAI (+8,43 %)

$PRY (+3,56 %)

34Positions

5,30 %

22

2 CommentairesPortfolio as interesting as it is peculiar, having intesa as the main share is not exactly a move I agree with but I understand that high dividends attract. If I were you I would increase the weighting of etf over individual stocks so that you have a steady growth and not too volatile (which is exactly what I am trying to do as well).

Otherwise I've noticed a lot of interesting stocks and also a small exposure on cryptos, I haven't ventured into them yet but a small percentage on the portfolio I would share.

Otherwise I've noticed a lot of interesting stocks and also a small exposure on cryptos, I haven't ventured into them yet but a small percentage on the portfolio I would share.

•

22

•11Mo·

A quality compounder in a niche market

I have recently opened a position in Sanlorenzo SpA $SL (+1,4 %) , a leading player in the luxury yacht and superyacht market.

It is currently trading at ~P/E 9.8, below its historical average and in line with peers. The company combines a strong brand, disciplined production (exclusivity & craftsmanship), and strategic geographic expansion (US & Asia) with a solid financial profile — low leverage, strong interest coverage, and net debt essentially under control.

Key points:

- Valuation: Market is pricing in modest FCF growth (~6%) compared to historical double-digit levels.

- Financial strength: Low debt/equity, high interest coverage, prudent capital allocation.

- Order book: Backlog covering over a year of revenues, 88% from final clients, providing visibility and stability.

- Growth prospects: Expansion in US and Asia, addition of Nautor Swan to the portfolio, investment in sustainable technologies, and a buyback program of up to 10% of shares.

The combination of a resilient business model, predictable revenues, and measured growth initiatives positions Sanlorenzo as a potentially interesting long-term opportunity that I decided to catch.

This post is for informational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.

88

1Année·

Depot Check

My goal is to beat the market, I'm still relatively young and want to see if I can do it, if not I'll put everything in an etf in 5 years.

Regarding my portfolio, I currently have a cash ratio of 23-25% depending on the fluctuations in the last month.

Purchases of existing stocks:

I plan to increase the financial stocks by 50%, $CG (+3,31 %)

$KKR (+0,93 %)

$APO (+1,95 %)

$TPG (+5,52 %) .

In addition, a little $DMP (+0,91 %) by 25%.

Sales:

I made the mistake of wanting to $EVO (+1,52 %) and $CPRX trade, but then I was too greedy.

I am convinced of both positions in the long term but not in this size in the portfolio, which is why I will reduce both stocks by 33%.

Potential purchases:

$HALO (+1,01 %)

$CUV (-0,98 %) - Will invest a little extra, otherwise just the 33% from sale of $CPRX. Both around 50 - 50

$SL (+1,4 %) - the same as $TISG (-1,59 %)

$KSPI (-0,75 %) - about as high as $MUM (-1,82 %)

$FIH.U (+3,45 %) - about as high as $MUM (-1,82 %)

$2GB (+1,84 %) - about as high as $MUM (-1,82 %)

$M12 (+1,82 %) - about as high as $MUM (-1,82 %)

$CPR (-1,68 %)

$DGE (-1,52 %)

$RI (-1,62 %) - I'll wait and see, but I can imagine that they will develop in a similar way to the tobacco shares. Since I don't want to decide, I'll just buy three for the sum of one. And divide the amount between these 3.

In general:

I'm generally a fan of putting together baskets like with alcohol or the yacht builders.

What would you change because you see a high risk? I am relatively poorly positioned in the tech sector, do you have any other titles that I could take a closer look at in this area?

12Positions

4,14 %

33

6 CommentairesHollow you definitely Amazon, Microsoft and Alphabet.

However, I would be interested to know how you came up with the companies mentioned in your article.

However, I would be interested to know how you came up with the companies mentioned in your article.

•

11

•1Année·

Update 01/25

As announced, here's a little update on January today, nothing long, don't want to bore you

Yield

Yield: 6.82% (FTSE All World: 4.23%)

TTWROR: 7.29%

Thus slightly outperformed, hopefully I can extend this lead further

transactions

Sales:

- Shimano $7309 (-0,42 %)

Medpace $MEDP (+0,1 %)

Apple $AAPL (+2,28 %)

Domino's Pizza $DPZ (-0,32 %)

McDonald's $MCD (-0,11 %)

Purchases

- Norbit $NORBT (+2,56 %) (subsequent purchase)

- Frosta $NLM (+0,24 %) (initial purchase)

- RCS Mediagroup $RCS (-0,48 %) (initial purchase)

- Uber Technologies $UBER (+1,07 %) (initial purchase)

- Sanlorenzo $SL (+1,4 %) (initial purchase)

- Charles River Labs $CRL (+1,2 %) (subsequent purchase)

- Simply Better Brands $SBBC (initial purchase)

Looks like a lot of back and forth for now, but with this my portfolio conversion continues and will soon be completed

31Positions

46 048,34 €

8,99 %

55

4 Commentaires

1Année

Does the FTSE All Wolrd have Bitcoin in it? Maybe you should separate for honest stock returns 😊

•

55

•Titres populaires

Meilleurs créateurs cette semaine

Données en temps réel par LSX · Données financières de FactSet