$BAYN (+2.45%)

$LDO (+1.2%)

$FCT (-1%)

$VOW (-1.13%)

$SAN (+0.06%)

$VWRL (-0.21%)

$ENI (-2.28%)

$SHEL (-2.3%)

$KO (-0.2%)

$ISP (-0.42%)

$INTC (+2.91%)

$SL (+1.01%)

$GOOGL (-5.21%) .

Sanofi

Stock

Stock

ISIN: FR0000120578

Ticker: SAN

FR0000120578

SAN

Price

Discussion about SAN

Posts

362Wk·

Portfolio Update

18Positions

€9,195.48

17.77%

33

2Mon·

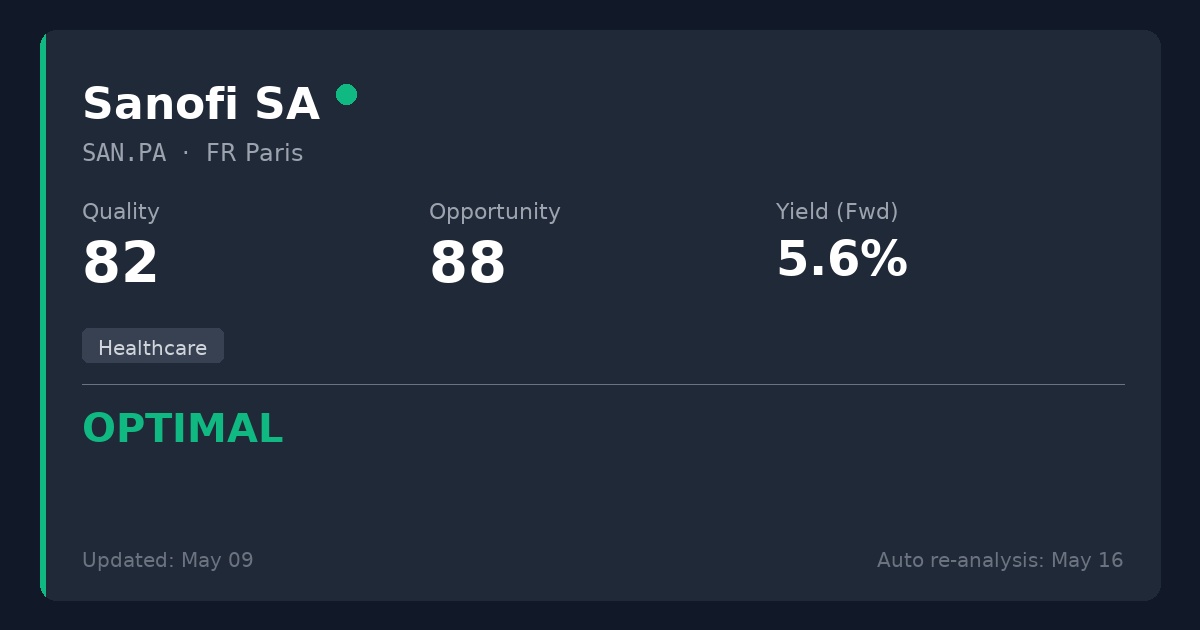

Sanofi (SAN.PA): A Value Trap or the Ultimate Contrarian Play?

The market doesn't like Sanofi $SAN (+0.06%) right now. Between the fears of the Dupixent patent cliff, weak pipeline results, margin drops from their R&D pivot, and political fears in the US healthcare sector, the stock has taken a serious beating.

But when we ran Sanofi through our algorithm in this week's batch, the cold math told a very different story.

Quadrant: 🟢 OPTIMAL

Quality Score: 82.0/100

Opportunity Score: 88.0/100

Why the engine is flagging this as a deep discount:

* The 99% payout ratio on basic screeners is a lie. This is just accounting noise. The actual cash flow payout ratio (FCF) is a very conservative 44.4%. The 5.6% dividend is strictly protected.

* The balance sheet is a fortress. Net Debt to EBITDA is just 1.33x, well below our 3.0x danger limit. They have the financial flexibility to execute their R&D pivot.

* It trades at an exceptional P/E of 8.69x.

The algorithm's verdict: The market is pricing Sanofi as if its entire pipeline will fail. Now that the Opella consumer health sale is closed and Sanofi is a pure-play biopharma, there is obvious execution risk. But their core cash generation remains completely intact. Top business at a great price.

88

3Mon·

This time it's my favorite asset class that I'm reporting on for the first time

Hello everyone.

Today I'm not going to analyze my $ALV (+0.36%) or $BATS (-0.41%) . By the way, I'm currently looking for a really cool dividend stock, but the final analysis is not yet complete, a few exciting companies are still on the longlist (e.g. $ABT (-1.14%) , $NOVO B (+0.57%) , $SAN (+0.06%) ) - no matter. That's not what we're talking about today, but P2P loans. Do you know this class? I've been using this class for almost 6 years and just wanted to report on it and then go into more detail about my "third oldest" platform - Income Marketplace. If you want to see nice graphics and my portfolio charts, you should go to my free blog post, if the text is enough, stay here ;) - Otherwise here: https://steady.page/de/finanzen-anders/posts/7f29f472-572d-49aa-98da-bd0978640036

Why I invest a lot of money without deposit protection - and still sleep soundly

"Imagine someone offering you a permanent 12% return per year."

"The first question is not where can I sign upbut:

Who actually bears the risk here?"

I myself have been investing since 2022 part of my assets in P2P loans (€ 88,064 as at the end of April 2026)specifically via Income Marketplace - Income is my third oldest platform. I've been invested in Bondora for almost 6 years.

This is not a self-experiment out of boredom, but a deliberate addition - and yes, so far with returns well over 10 % p.a.

This means that the investment beats both my call money and most of my broadly diversified ETFs in difficult market phases.

But:

If double-digit returns beckon anywhere on a sustained basis, then the same applies in accounting as in real life:

"If it looks too good to be true, someone is obviously taking risk."

So the question is not whether risk exists - but who bears it, how it is structured and whether you are fairly rewarded for it.

P2P is not a savings product.

Rather, it is the asset class for people who know that returns do not fall from the sky, but from assumed risk.

If you are interested in the P2P asset class in video form, please watch my video:

I have also written about the P2P asset class in great detail on my financial blog (in 7 parts). Here is the link to part 1:

Why I like to invest in P2P loans? Take a look at this graphic - in my financial blog :)

The purple curve is my main stock portfolio at ScalableThe purple curve is my main stock portfolio at , strong highs and when Donald Trump declares tariffs, my portfolio plummets. Not for the faint-hearted.

The yellow curve is my investment in P2P loans as a whole, a really nice yield ladder. And Income? In light green, significantly higher returns than the yellow curve. In other words, I have a relatively predictable passive income here!

What is the business model - quite soberly?

With P2P loans, we give investors money to lendersmostly fintechs in Europe or emerging markets.

These lenders grant (among other things) consumer loans with high interest rates - and we get part of it.

👉 We are replacing the bank to a certain extent.

With the small difference that we:

- no deposit protection

- no state protection

- and no guarantee have.

- We take over but also parts of the credit risk,

- but in return get we also higher interest rates.

That is uncomfortable - but honest.

Income Marketplace is thereby not a lenderbut a marketplacethat connects investors with fintech lenders (loan originators) brings them together.

👉 Anyone who invests here is not in loans in Germanybut in loan portfolios from Europe, Central and South America, Asia. And I personally find that very exciting.

Income

So why Income of all things?

Income Income differs from many P2P platforms in a way that you can only appreciate if you have experienced early P2P crises:

A buyback guarantee is only as good as the lender who can pay it in an emergency.

That is why Income on a multi-level security concept:

- Lenders retain 20-35 % of the loans themselves,

- but subordinated - we are serviced first.

- If a lender defaults entirely, the portfolio can Income take over the portfolio

- and continue to process it via debt collection.

This is not a magic trick.

But it is structurally cleaner than the classic "Trust me, I'll buy it back later".

Now the honest part

Income is:

- not regulated

- not profitable

- and the security mechanisms have never been tested in a real major crisis

And yet I invest.

Why?

Because I:

- understand the risk understand

- it limit it

- and don't confuse it with "safe money"

In other words:

This money doesn't have to be there in three years - but it is very welcome to work.

The most important distinction

The officially reported defaults are less than 2 %.

Depending on the country, the real borrower defaults are 20-25 %.

This is not a contradiction -

but shows that there is constant regrouping, buying back and reinvesting.

👉 The return is not generated because nobody defaults -

but because the system expects defaults.

The mistake many beginners make

Many people hear:

"Buy-back guarantee, auto-invest, 12% - sounds relaxed."

And that's exactly that is the dangerous moment.

P2P only works well if you:

- diversified

- critically scrutinize lenders

- and come to terms internally with defaults

If you are looking for absolute security lost nothing here.

But if you are looking for returns and consciously manage riskwill find an interesting niche here.

Conclusion

My conclusion in one sentence

P2P loans are not a substitute for overnight money -

but a deliberately risky addition to returns for people who know why they are getting 12 or 13 %.

And when we think about it, it's not with the question

"Is that safe?"

but with the much more important one:

"What risk am I consciously taking - and am I getting a fair price for it?"

If you would like to open an account with Income, please use my affiliate link: https://link.finanzenanders.de/income

Not enough?

If you Income Marketplace or P2P investments interest you, then let's get down to business.

Income Marketplace In figures (so we're not just talking about feelings)

- Foundation: 2020

- Registered office: Tallinn, Estonia

- Regulation: ❌ None

- Investor assets under management: ~EUR 26-27 million

- Financed loan volume: >EUR 220 million

- Average yield: approx. 11-14 % p. a. (13,78 % lt. Income)

- Deposit protection: ❌ None

- My current investment: € 3,579

- My current return: 12.95 %

In short: Not a savings account. Not even close, but a very high return.

At times I've invested over €10,000 on Income I withdrew a lot from all my P2P loans when we bought our house. That was the plan. And now the great thing is that with Income the transfer to my reference account is free of charge and super fast!

I like the UI / structure of Income:

Everything at a glance.

I also really like the cash flow forecast.

Why Income not simply "Mintos with a different logo" is

Income is trying to solve a problem that P2P investors have known well since corona:

The buyback guarantee is only worth as much as the lender who promises it.

Therefore Income on two additional security mechanisms:

Security concept 1: Junior Share

("Skin in the Game - but the right way, please")

With almost all loans, the lender holds a subordinated subordinated equity share - usually 20-35 %.

This means that

- Investors are are given priority

- the lender receives money only when we are fully repaid

- if the portfolio turns out worse → the lender loses first

👉 This is structurally better than classic "skin in the game", but:

- It protects not from poor collection rates

- It does not protect not from systemic crises

- It has never been proven in a major stress test

Security concept 2: Cash flow buffer

(Or: "Plan B in case the lender disappears")

If a lender defaults:

- Income takes over the loan portfolios via SPVs

- Repayments continue

- Collections are made via local partners

- Losses are to be cushioned by surpluses & junior shares

Sounds good - and is conceptually clean.

But to be fair, it has to be said:

The real thing hasn't really been played out yet.

The well-known problem case ClickCash (Brazil) was simply too small to seriously test the system.

Failure rates: Apparently low - potentially brutally different

This is where it gets exciting:

- Official platform statistics (March 2026):

- → only 1,7 % of the portfolio in debt collection

- Lender-specific:

- → partial 20-25 % defaults with high-risk originators

- (e.g. Indonesia, Brazil with ClickCash)

This is not a contradiction:

- Short-dated + buyback + regrouping conceal short-term defaults

- In the long term, everything depends on Lender quality & collection efficiency

👉 Diversification is not a "nice to have" here, but essential for survival.

Auto-Invest: Passive income - or passive looking away?

Income lives from Auto-Invest.

Once configured, the capital (usually) continues to work diligently.

Advantages:

- Compound interest

- hardly any cash drag

- Very granularly controllable

But:

- You must not not blindly filter for yield

- if you take all lenders & countries, you also buy problems

💡 My personal lesson:

Better fewer lenders - but understood risks.

This is how my auto-invest is set up

However, I also have the option of investing manually, such as in this short-term business loan:

Sorted by shortest term

I have chosen the top loan and will invest €25.41.

Done.

The inconvenient truth: Income is not (yet) profitable

Income earned:

- approx. 2-4 % p. a. fees on loan portfolios

- no fees from investors

Problem:

- Losses in the annual reports

- No audited financial statements

- Dependent on investor and financing rounds

Plain language:

You also invest to a certain extent in the hope that Income survives as a platform.

For whom is Income suitable - and for whom not?

Suitable for: ✅ Yield-oriented investors

✅ People with previous P2P experience

✅ Investors who can mentally & financially cope with total losses

✅ Addition of up to ~5-10% of total assets

Not suitable for: ❌ Security lovers

❌ "This is my nest egg" faction

❌ Investors without time to monitor risk

❌ People who believe that 12% is "virtually safe"

Conclusion: Exciting, lucrative - but not a free ride

Income Marketplace is not a miracle investmentbut:

- structurally more sophisticated than many P2P platforms

- transparent

- high-yielding

- so far without losses for investors

👉 Whether it stays that way is decided not the marketingbut:

- a real lender crash

- a recession in emerging markets

- or your own discipline when investing

In other words:

Income is not a savings account.

But perhaps that's precisely why it's interesting. Definitely for me :)

Disclaimer

Of course, investing in shares, ETFs, crypto, ... is always associated with risks. My thoughts are therefore not to be understood as concrete recommendations for action (neither buy nor sell recommendations), but are intended to stimulate your way of thinking. So that you can also develop your own opportunities. Past performance is no guarantee of future returns. Capital is at risk. Furthermore, the data and figures are not accurate. For links with * I receive a commission if you order through them. There are no additional costs for you. Thank you for your support!

Even I can make mistakes, so please always double-check.

This article reflects my opinion and my experience, although it is financially supported by Income is financially supported.

steady.pageJust a moment...

1111

10 Comments

Stefan@Da_Fischi

3Mon

•

11

•View all 7 further answers

5Mon·

Current recommendations on dividend stocks (DZ Bank)

The DZ Bank analysts have drawn up two lists of shares that they consider to be particularly attractive. For more defensive investors and for investors who rely on continuous cash flows, they recommend the so-called "dividend aristocrats": In other words, companies that have regularly paid and raised dividends.

Top dividend aristocrats:

Pfizer $PFE (+1.25%), Verizon $VZ (-1.7%), BNP Paribas $BNP (-0.4%)Zurich Insurance $ZURN (-0.05%), Enel $ENEL (-0.45%), Sanofi $SAN (+0.06%), Hannover Re $HNR1 (+0.28%) , Man and Machine $MUM (+0.55%), Generali $G (-0.07%) and Allianz $ALV (+0.36%)

Another list has been compiled for investors with a somewhat higher risk appetite: Stocks with attractive dividend yields and additional share price potential. These not only pay a good dividend of at least three percent, but could also increase significantly in price in the future. However, the continuity of dividends in the past plays a lesser role - and this strategy is correspondingly riskier.

Top dividend rockets:

Man and machine $MUM (+0.55%) , Cancom $COK (-1.31%), Bastei Lübbe $BST (+1.26%), Sixt $SIX2 (-1.67%), Kontron $KTN (-0.05%), Fresenius Medical Care $FME (-1.02%), Vonovia $VNA (-2.24%), Hawesko $HAW (-1.64%), ElringKlinger $ZIL2 (+7.86%) and Hannover Re $HNR1 (+0.28%)

Source text (excerpt) & graphic: World | AAA, 19.02.2026

1414

5Mon·

Takeover rumors

$OCUL (-1.34%) jump up considerably today. Most recently, there were takeover rumors in January by $SAN (+0.06%) .

The reason for the jump could be similar news that has not yet been made public here. I am currently assuming a short-term jump and am considering going short. Analysts see a clearly positive trend until 2027, but in the short term I don't think this will be reflected in the share price.

Source: https://www.sharedeals.de/bietet-sanofi-mehr-als-16-us/

Edit: unfortunately my broker (ING) does not have any bills

www.sharedeals.deOcular Therapeutix: Bietet Sanofi mehr als 16 US$?

44

2 Comments

There is MM2Z8L factor 4 bill

And 2 more from MS with factor 3 and 2

And 2 more from MS with factor 3 and 2

•

22

•7Mon·

Takeover worth billions in the pharmaceutical industry

Last month I was still looking into Dynavax. But unfortunately only put it on the watch at first.

The French pharmaceutical group Sanofi is acquiring the US vaccine company Dynavax Technologies Corporation for a value of 2.2 billion US dollars. According to Sanofi, it is offering USD 15.50 per share in cash and the deal is expected to be completed in the first quarter of 2026. With the takeover, Sanofi is securing the HEPLISAV-B drug, a vaccine already marketed in the USA for the prevention of hepatitis B in adults, among other things. The vaccine differs from existing offerings with a two-dose schedule within one month, whereas conventional vaccines require three doses over six months. Dynavax currently has the shingles vaccine candidate Z-1018 in development, which is currently in clinical phase 1/2.

www.n-tv.deMilliardenübernahme in der Pharmabranche

9Mon·

Collapse of the French government

The party in neighboring France was short-lived, Lecornu resigned and with him the Paris stock market sank, too bad being that France turns out to be a solid country in fundamentals, the latest data showed good growth in the country despite unstable politics, let's see how long this will last and by how much French stocks will fall, some opportunities may appear on the horizon, in France personally I am following $SAN (+0.06%) e $ENGI (-0.97%) , solid companies with good distribution, the former still undervalued according to fundamentals. I will have a chance to invest more cash in 10 days, in the meantime I am watching the developments in the transalpine market.

44

11Mon·

Buying opportunity?

Time to buy $SAN (+0.06%) now?

11

2 Comments

It has good fundamentals and it is certainly cheap

•

33

•

1Yr·

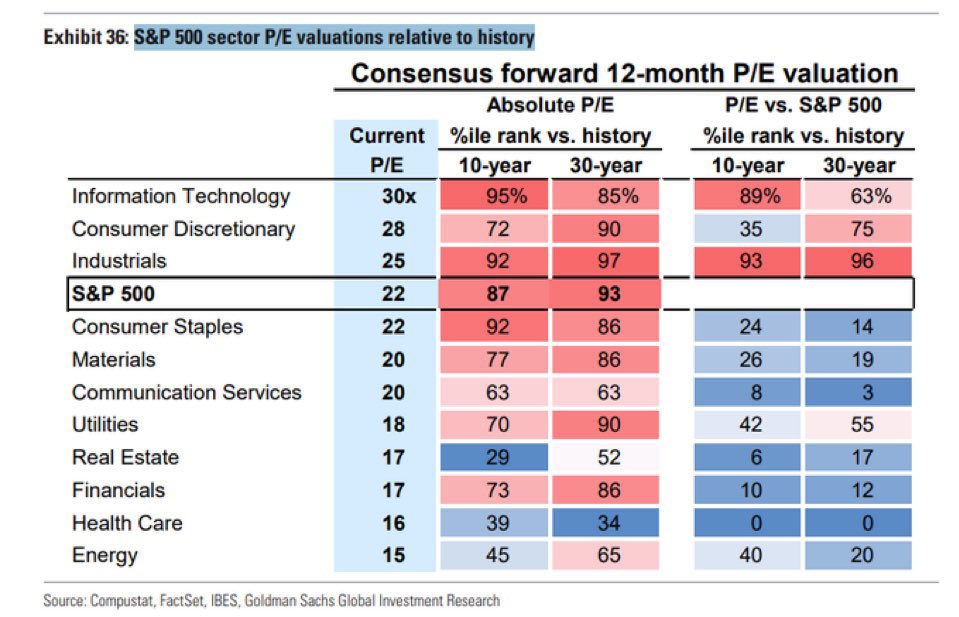

Valuation Healthcare sector - Goldman Sachs

$XDWH (+1.19%)

$XLV (+1.15%)

$CSPX (-0.32%)

$VUSA (-0.38%)

$UNH (+0.65%)

$OSCR (-1.1%)

According to Goldman Sachs, healthcare is the only sector in the S& P 500 that is cheaper than the 10- and 30-year averages.

This is an extremely attractive risk/reward ratio and the coming months will be exciting.

$ELV (+3.46%)

$CNC (+4.94%)

$DHR (+1.93%)

$SRT (-1.81%)

$LLY (+3.09%)

$NOVO B (+0.57%)

$NVO (+0.36%)

$ISRG (+1.32%)

$JNJ (+0.43%)

$ABBV (+0.31%)

$PFE (+1.25%)

$SAN (+0.06%)

$MRK (-0.11%)

$BMY (-3.95%)

$TMO (+1.89%)

1Yr·

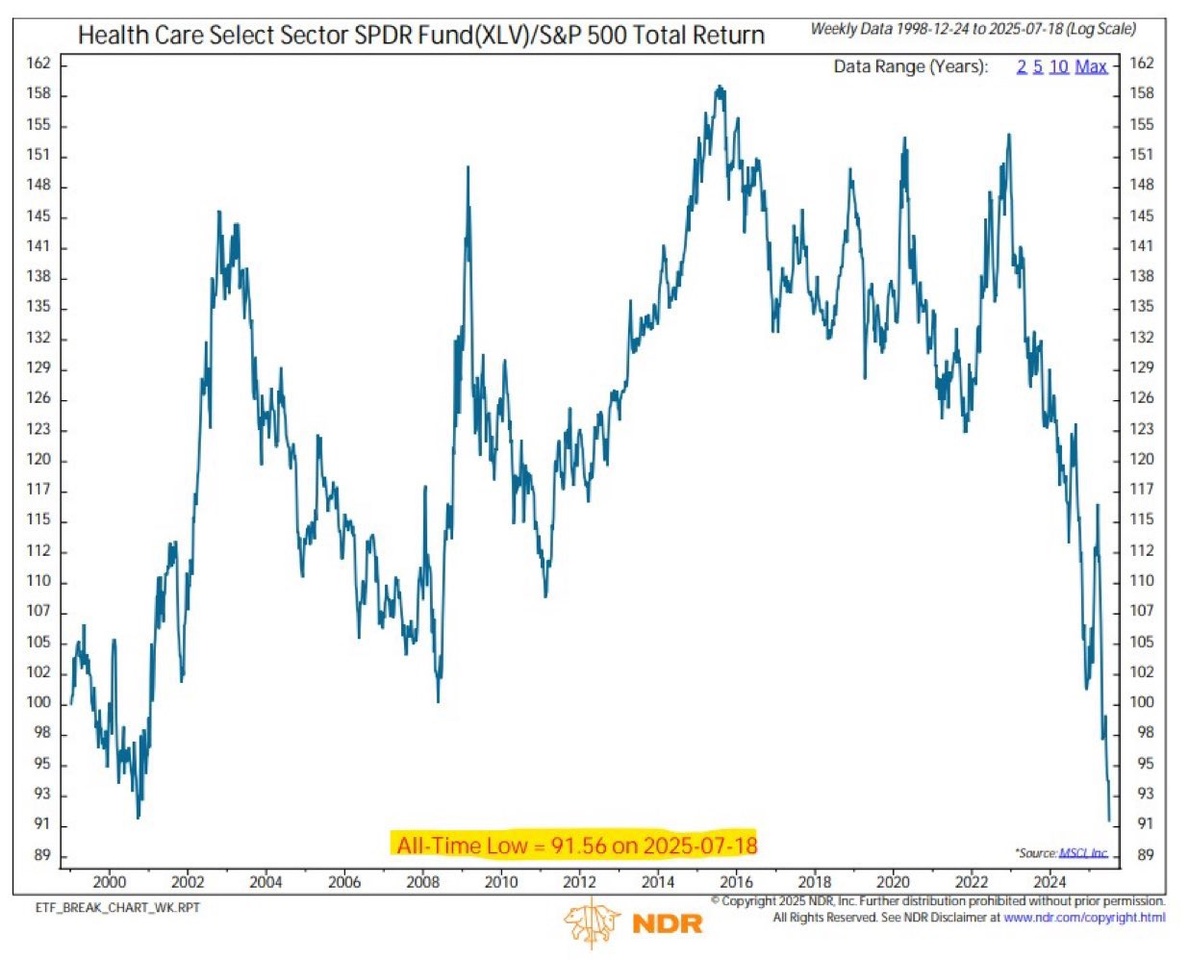

Weak US healthcare sector

$UNH (+0.65%)

$OSCR (-1.1%)

$XDWH (+1.19%)

$ELV (+3.46%)

$LLY (+3.09%)

$XLV (+1.15%)

The US healthcare sector is experiencing its biggest crash in the last 20 years.

If the strong weighting no. 1 $LLY (+3.09%) (over 12%), one would have to go back even further/longer. (probably before the existence of the ETF).

I have positioned myself strongly here as I believe this is a great opportunity.

I also believe that a lot of capital will flow into the sector in the coming months. ✌️

Do you have a similar view? ✌️

99

6 Comments

I still have one US pharma share on my buy list.

But I'm wondering whether I should get in before August.

But I'm wondering whether I should get in before August.

•

22

•

1Yr·

New additions to my portfolio: Sanofi & Unilever

Today I added two European giants to my portfolio:

$SAN (+0.06%) – Healthcare

$ULVR (-0.04%) – Consumer staples

Why?

My portfolio was heavily concentrated in the US and tech stocks. Over the past months, I've been working to build something more balanced — with solid dividends, strong fundamentals, and global exposure.

My current strategy:

I'm gradually shifting towards defensive sectors and passive income.

These two picks bring:

✅ Diversification into the Eurozone and UK

✅ Exposure to resilient industries

✅ Reliable dividends in EUR

• Sanofi ~4% (annual)

• Unilever ~3.5% (quarterly)

I'm 26, started investing with a strong crypto tilt (still hold some), but my focus now is long-term income, stability, and financial freedom — one step at a time.

Trending Securities

Top creators this week

Real-time data from LSX · Fundamentals & EOD data from FactSet