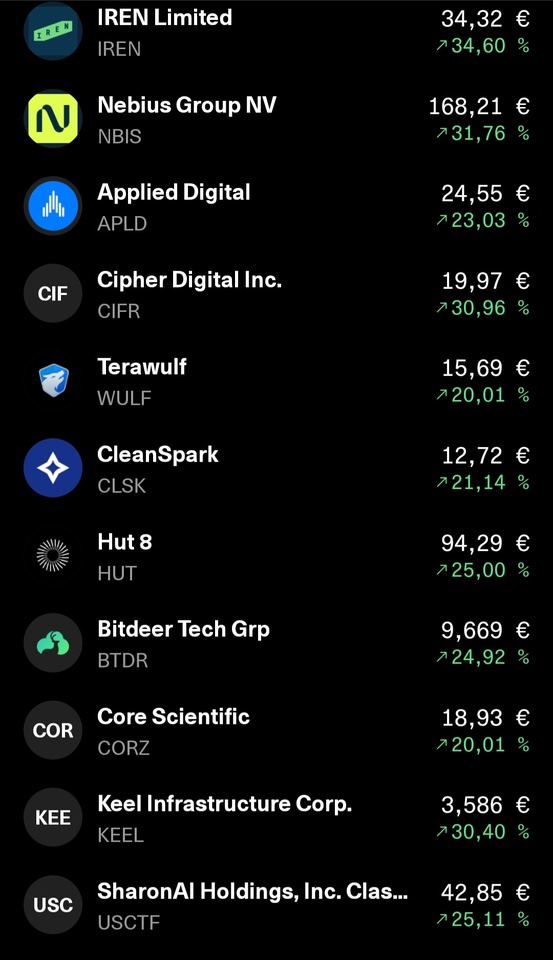

Leopold Aschenbrenner, an AI investor who is just 24 years old, finds himself facing the ruins of his radical investment strategy with his once-extremely-successful hedge fund, Situational Awareness LP, as massive leverage proved to be his undoing during the recent tech sell-off. To meet urgent margin calls from his banks, the fund was forced to liquidate its entire public equity portfolio—which was heavily concentrated in AI infrastructure and software short positions—in a last-ditch effort and sell it off to a competitor. While the massive paper gains from the first half of the year have thus been wiped out, the former wunderkind is now fighting for the very survival of his remaining fund through the hasty sale of lucrative private-equity stakes, such as in the AI startup Anthropic. With his fund, Aschenbrenner was primarily invested in AI infrastructure and energy stocks such as Nebius, SK Hynix, Micron, CoreWeave, and Bloom Energy, while simultaneously maintaining short positions in software stocks like Adobe.

Leopold Aschenbrenner’s hedge fund, “Situational Awareness LP,” was in fact largely forced into liquidation on July 30, 2026, as he had bet heavily on AI infrastructure stocks and Bitcoin miners using a risky 4x leverage. When these sectors plummeted in July and his short positions in software stocks simultaneously backfired, uncovered margin calls forced the fund to dump its entire public equity portfolio in one fell swoop to the market maker Citadel. As a result of this crash, the fund’s assets under management—which had previously grown rapidly to over $20 billion—were halved to approximately $10 billion. What remains now consists almost exclusively of unlisted private-market investments that were spared from the short-term margin calls, including, most notably, a massive stake in the AI company Anthropic valued at around $5 billion.

Leopold Aschenbrenner (born in 2001 or 2002) is a German researcher and investor in the field of artificial intelligence who graduated from Columbia University at the age of 19 as valedictorian. After working for the Global Priorities Initiative in Oxford and the FTX Future Fund, he joined OpenAI’s “Superalignment” team at OpenAI, but was dismissed in April 2024 following internal conflicts over what he considered inadequate security measures and an alleged information leak. He gained international recognition shortly thereafter with his highly acclaimed essay “Situational Awareness,” in which he predicts the development of artificial general intelligence (AGI) by 2027 and the massive global security challenges that would accompany it. In the wake of this success, he founded the AI-focused hedge fund Situational Awareness LP, which is backed by prominent tech investors.

$NBIS (-2,65%)

$ADBE (+1,12%)

$000660

$SKHY (-4,49%)

$SKHY (-4,49%)

$CRWV (-5,11%)

$MU (-7,98%)

$BE (-3,13%)