$KSPI (-2,22 %)

$NCLH (-3,58 %)

$STNE (-3,21 %)

$BEI (-1,51 %)

$SE (-4,33 %)

$ONON (-3,62 %)

$TGT (-2,32 %)

$GTLB (-3,67 %)

$CRWD (-2,83 %)

$BAYN (-1,05 %)

$WIX (+1,17 %)

$ADS (-4,76 %)

$AVGO (-1,41 %)

$DHL (-1,37 %)

$R3NK (+0,83 %)

$JD (+0 %)

$BILI (-1,29 %)

$1913 (-1,53 %)

$MRK (+1,4 %)

$MRVL (-1,72 %)

$GPS (-3,42 %)

$COST (-0,24 %)

$IOT (-4,71 %)

$LHA (-3,69 %)

Discussion sur WIX

Postes

104Mo·

Quarterly figures 02.03-06.03.26

1515

6Mo·

3-point checklist for the turnaround - does Wix have what it takes?

The stock market year is coming to an end and the cards are being reshuffled. Because stock market history shows: Today's losers are often tomorrow's stars.

On the winners' podium

The year is slowly drawing to a close. The big winners and losers have been announced.

The top 5 in the S&P 500 this year consists almost entirely of hardware manufacturers. With share price gains of between 216 % and 560 %, Sandisk, Western DigitalSeagate, Robinhood and Micron occupy the top spots.

Anyone who was there can rejoice. For example, I commented positively on Seagate and Micron several times during the year.

At the other end of the range are Trade Desk, Fiserv, Deckers OutdoorAlexandria Real Estate and Gartner. The share price losses are between 48 and 68 %.

The astonishing thing is that some of these shares were previously long-term performers.

As in every year, the question arises as to which shares offer the potential for a turnaround. Experience shows that the losers from one year always rise sharply in the following year. There are several examples of this.

Micron, for example, crashed significantly in the course of 2024 and was trading at around USD 61 just a few months ago - today the price is around USD 265.

But caution is advised: Most shares have crashed with good reason. A successful turnaround therefore requires a healthy core business that has only been impacted by temporary factors or economic headwinds.

The 3-point checklist for a turnaround

Before investing in a stock that has crashed, you should ask yourself three questions:

Has the stock crashed because there are general economic problems or the industry has fallen out of favor? Or are there structural problems?

Is there a reason why 2026 could be better? For example, through cost-cutting programs, an improving economy, falling key interest rates, new management, etc.?

Is the company on a solid footing or could it be in trouble?

A company should meet all of these criteria. Ideally, business should be going well and the share price should have fallen for other reasons. An astonishing number of shares currently fall into this category.

Just as some supposed or real AI winners have virtually gone through the roof, many supposed AI losers have also crashed.

Stock market losers with potential

In my view, Wix is a particularly extreme example. The share has lost more than half of its value, even though the company has consistently delivered.

There are fears on the stock market that the website builder business will be displaced by AI. This thesis cannot simply be dismissed out of hand. However, it seems to overlook the fact that Wix does not earn its money with the website builders themselves, but with the associated services such as hosting, marketing packages, payment processing, etc.

If companies and private customers create their websites with an AI instead of a website builder in the future, they will still need all of these services.

On top of that, they could use Wix's AI, because the company is of course not idle in this area - quite the opposite. With Base44, Wix is one of the stronger companies in this area and appears to be gaining market share.

This is an AI-supported platform that can create fully functional individual apps based on simple text commands - completely without programming.

When the narrative changes ...

Wix could therefore just as easily be classified as an AI winner. If the narrative on the stock market changes, the valuation is also likely to change drastically.

According to recent press reports, OpenAI has just secured fresh capital. In the financing round, the company was apparently valued in the high three-digit billion range, although OpenAI does not yet have an established business model.

Wix, on the other hand, is highly profitable and Base44 is growing at an enormous pace. One can and may ask oneself what stock market value Base44 would currently achieve on its own.

At the end of the year, the annualized turnover should be USD 40 - 50 million.

Base44 now has more than 2 million users and is gaining more than 1,000 new paying customers every day.

The growth momentum is increasing and has far exceeded expectations. I would not be surprised if Base44's turnover increases to USD 100 - 200 million in the coming year.

Bottom formation or next setback?

All this is underpinned by an equally growing core business. In the course of the quarterly figures, the forecast for sales in the current financial year was raised from USD 1.97 - 2.00 billion to USD 1.98 - 2.00 billion and for free cash flow from USD 590 - 610 million to USD 595 - 610 million.

This gives Wix a P/FCF of slightly less than 10.

A few days after the quarterly figures, further share buybacks were therefore decided and the budget for this was increased by USD 200 million to USD 500 million, which corresponds to more than 8% of the market capitalization.

There are therefore several possibilities that could cause share prices to rise. On the one hand, Wix has a profitable core business, which enables share buybacks on a large scale and has a low valuation. In addition, there is the growth in the core business and Base44 and the possibility that the market could appreciate the value of Base44 more in the future.

Wix share: Chart from 22.12.2025, price: USD 104.43 - symbol: WIX | source: TWS

The share is currently trying to form a bottom near the support zone at USD 92 - 100. Starting from this base, there could now be a recovery towards USD 115 or 118.

The chart picture would brighten above USD 120.

However, if the share falls below USD 92, the bulls will have lost their chance for the time being.

Source

88

4 Commentaires

Chris@Multibagger

6Mo

•

22

•

11Mo·

Hidden Gem?

The analysis of Wix.com Ltd.'s latest business figures and strategic developments following the publication of Q2 2025 results on August 6, 2025 shows a company in a phase of significant transformation and strong operational performance.

The remarkable earnings per share of $2.28, which significantly exceeded expectations, as well as the acceleration of revenue growth and bookings for new cohorts reaching pre-COVID peak levels, are clear indicators of improved operational efficiency and successful strategic execution.

Wix is pursuing a sophisticated, multi-pronged growth strategy. The aggressive investments in AI-powered website builders, the acquisition of Base44 to tap into the application development market and the launch of financial services for merchants position Wix as a more comprehensive digital business platform that goes beyond just website building. This diversification into higher value segments and new revenue streams strengthens the resilience of the business model and offers significant potential for sustainable growth in average revenue per user.

The strong growth forecasts for the AI market in web development and the overall website builder market also provide a favorable macroeconomic tailwind.

Nevertheless, Wix is not without risks. The market is highly competitive and saturated, especially with dominant players such as WordPress and Shopify.

Despite these challenges, the opportunities outweigh the risks. The current valuation of the stock, which is close to its 52-week low, combined with the recent positive financial results and analysts' optimistic price targets, indicates an attractive risk/reward ratio.

Wix's ability to drive innovation and adapt to changing market demands, particularly through the increased use of AI, makes the company a promising candidate for investors interested in long-term growth in the digital ecosystem.

In view of the strong Q2 performance, the strategic expansion into high-growth areas and the attractive risk/reward ratio, a Strong Buy recommendation is issued for Wix.com Ltd.

Source: Deepsearch Gemini

11Mo·

The investment bank sees these stocks as the big beneficiaries of AI adaptation

$AAPL (-1,22 %) Apple, Inc. (ISIN: US0378331005)

$ADBE (-2,88 %) Adobe Inc (ISIN: US00724F1012)

$AES (+0,44 %) AES Corp (ISIN: US00130H1059)

$AMZN (-3,95 %) Amazon.com Inc (ISIN: US0231)

$APP (-3,3 %) AppLovin Corp (ISIN: US03831W1080)

$AXON (+0,67 %) Axon Enterprise, Inc. (ISIN: US05464C1018)

$BE (+2,18 %) Bloom Energy Corp. (ISIN: US09

$CRM (-4,35 %) Salesforce.com, Inc. (ISIN: US79466L3024)

$GOOGL (-3,5 %) Alphabet Inc (Class A) (ISIN: US02079K3059)

$GTLS (+0 %) Chart Industries, Inc. (ISIN: US16115Q3083)

$HUBS (-5,81 %) HubSpot Inc (ISIN: US4435731009)

$JCI (+1,18 %) Johnson Controls International plc (ISIN: IE00BY7QL619)

$NEE (+0,62 %) NextEra Energy, Inc (ISIN: US65339F1012)

$NVDA (-1,19 %) NVIDIA Corp (ISIN: US67066G1040)

$SLB (+0,29 %) Schlumberger N.V. (ISIN: AN8068571086)

$SPGI (-1,95 %) S&P Global Inc (ISIN: US78409V1044)

$TSLA (-11,28 %) Tesla Inc (ISIN: US88160R1

$TT (+0,92 %) Trane Technologies PLC (ISIN: IE00BK9ZQ967)

$$VRTX (+0,71 %) Vertex Pharmaceuticals Inc (ISIN: US92532F1003)

$VERTEX (+0,26 %) Vertex, Inc (ISIN: US92538J1060)

$VST (+1,18 %) Vistra Corp (ISIN: US92840M1027)

$WIX (+1,17 %) Wix.com Ltd (ISIN: IL0011301780)

Morgan Stanley expects these companies to benefit greatly from the global trend towards AI integration, whether through leading chips such as NVIDIA, cloud and software solutions such as Amazon, Alphabet or Salesforce, or specialized applications in energy, industry and biotechnology. With tech giants expected to invest almost 400 billion US dollars by 2026, demand in many of these segments could explode. But while the list reads impressively, there is still the intriguing question of who will ultimately benefit not only from the hype, but also from the sustainable use of this technology.

Source: Boerse-Online (Morgan Stanley report on AI-related stocks)

Image material: Techa Tungateja/iStockphoto

1Année·

WIX Q4'24 Earnings Highlights

🔹 Adj. EPS: $1.93 (Est. $1.59) 🟢

🔹 Revenue: $460.5M (Est. $461.75M) 🟡; UP +14% YoY

🔹 Bookings: $464.6M (Est. $461.75M) 🟢; UP +18% YoY

🔹 Free Cash Flow: $131.8M (Est. $130.12M) 🟢

Q1'25 Guidance:

🔹 Revenue: $469M-$473M (Est. $481.47M) 🔴; UP +12-13% YoY

FY'25 Guidance:

🔹 Revenue: $1.97B-$2.0B (Est. $2.018B) 🔴; UP +12-14% YoY

🔹 Bookings: $2.03B-$2.06B (Est. $2.08B) 🔴; UP +11-13% YoY

🔹 Free Cash Flow Margin: 30-31% (Est. 29%) 🟢

Q4'24 Segment Revenue:

🔹 Creative Subscriptions: $329.7M (Est. $330.46M) 🟡; UP +11% YoY

🔹 Business Solutions: $130.7M (Est. $131.31M) 🟡; UP +21% YoY

🔹 Partners: $168.1M; UP +29% YoY

🔹 Transaction: $57.1M; UP +23% YoY

Q4'24 Geographical Insights:

🔸 ~40% of revenue from non-USD currencies; FX headwinds expected in 2025

Other Q4'24 Key Metrics:

🔹 Creative Subscriptions ARR: $1.343B; UP +13% YoY

🔹 Non-GAAP Gross Margin: 70%; Flat YoY

🔹 Creative Subscriptions Gross Margin (Non-GAAP): 85%; UP +1% YoY

🔹 Business Solutions Gross Margin (Non-GAAP): 32%; UP +2% YoY

🔹 FCF Margin: 29%; UP from 22% YoY

Announcements & Strategic Updates:

🔸 Completed $200M share repurchase in Jan 2025; $725M total since Aug 2023

🔸 Achieved first year of positive GAAP operating income in 2024

🔸 On track for Rule of 45 in 2025 at high end of outlook

Management Commentary:

🔸 "Wix sets a high standard for innovation and creativity, and we’re constantly exceeding expectations," said Avishai Abrahami, Co-founder and CEO. "2025 is poised to reimagine and expand the Self Creator experience with two transformative products planned for the spring and early fall, delivering immense value to users and accelerating growth."

🔸 "We wrapped 2024 with accelerated growth and profitability, driven by successful execution of our product roadmap and pricing strategy," added Lior Shemesh, CFO. "Solid growth coupled with efficiencies puts us on track to achieve Rule of 45 in 2025."

33

1Année·

Wix Q3 FY24 #EarningsReport Summary | $WIX (+1,17 %)

In Q3 FY24, http://Wix.com sustained strong momentum through strategic AI integrations, robust partner activity, and innovative product launches. These efforts culminated in accelerated bookings growth and increased profitability metrics.

📊 Income Statement Highlights (vs Q3 FY23):

▫️ Net Income: $26.78M vs $6.98M (+283.70%)

▫️ Revenue: $444.67M vs $393.84M (+12.91%)

▫️ Adjusted EPS: $1.50 vs $1.10 (+36.36%)

▫️ Total Bookings: $449.80M vs $389.10M (+15.62%)

▫️ Free Cash Flow (FCF): $127.76M vs $44.77M (+185.46%)

📊 Segment Revenue Highlights:

▫️ Creative Subscriptions: $318.83M (+9.71%)

▫️ Business Solutions: $125.85M (+21.98%)

💼 Balance Sheet Highlights:

▫️ Total Assets: $1.71B

▫️ Cash and Cash Equivalents: $439.43M

▫️ Deferred Revenues: $656.67M

🔮 Future Outlook:

Wix has raised its FY24 revenue outlook to $1.76B, projecting 13% YoY growth. It anticipates continued AI-driven momentum, robust cohort retention, and FCF margin expansion into FY25.

22

2Année·

Satisfied with the use of AI?

Have a wonderful Monday morning!

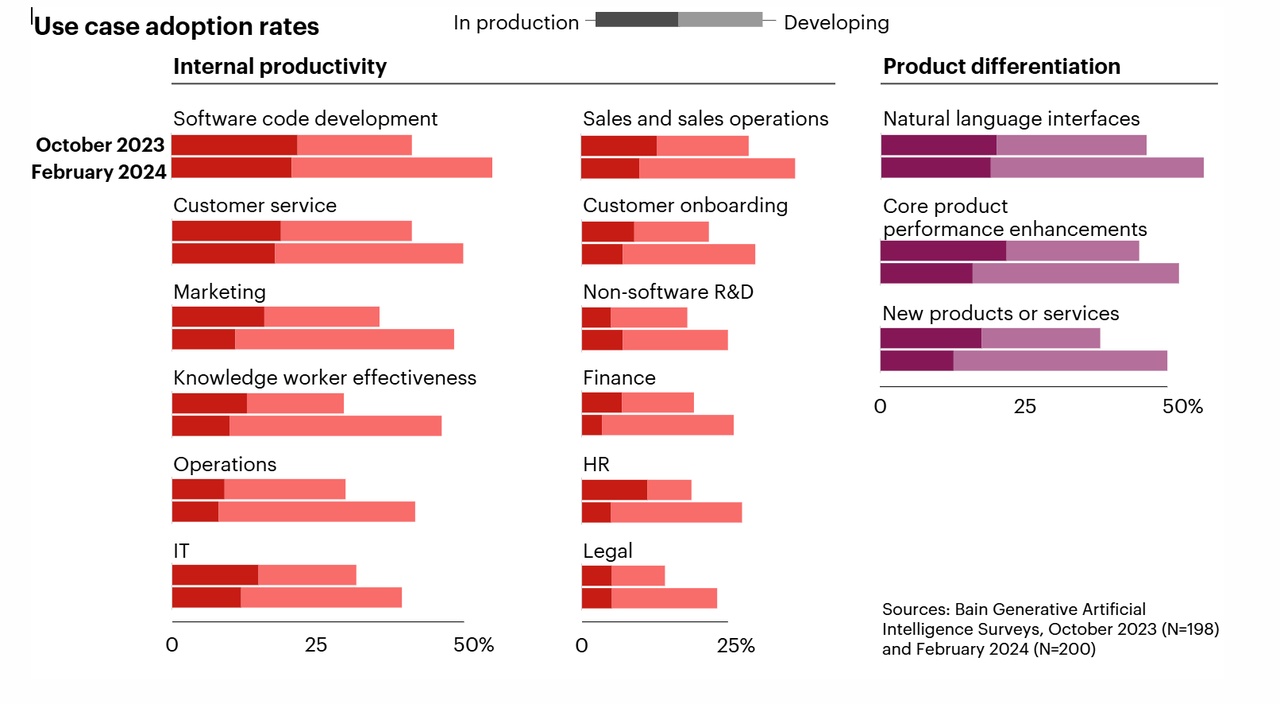

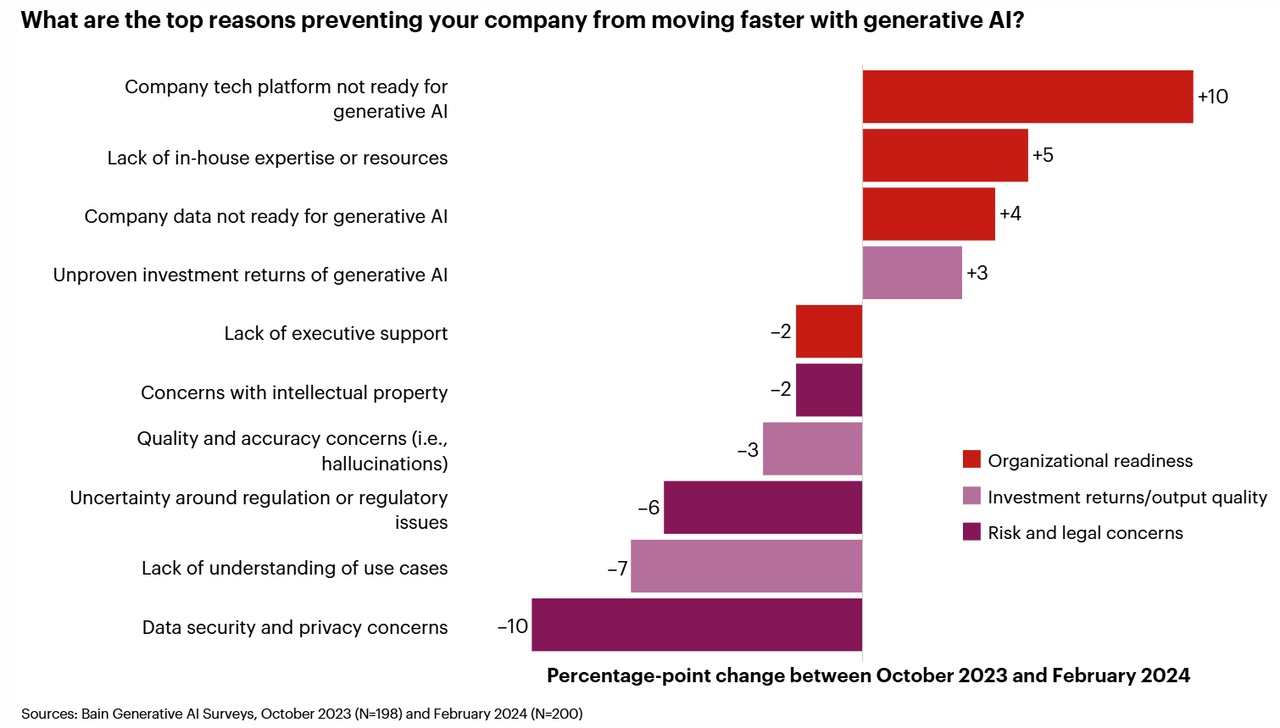

I just read an exciting survey from Bain & Company that shows that companies around the world are investing heavily in artificial intelligence (AI). Bain has identified four main themes that emerge from their survey:

Widespread adoption of Generative AI87% of the companies surveyed are developing, testing or already using generative AI. These technologies are mainly used in areas such as software development, customer service, marketing and sales.

High investmentsSmaller companies invest around USD 5 million per year in generative AI, while larger companies spend up to USD 50 million per year. These investments show the high confidence in the potential benefits of AI.

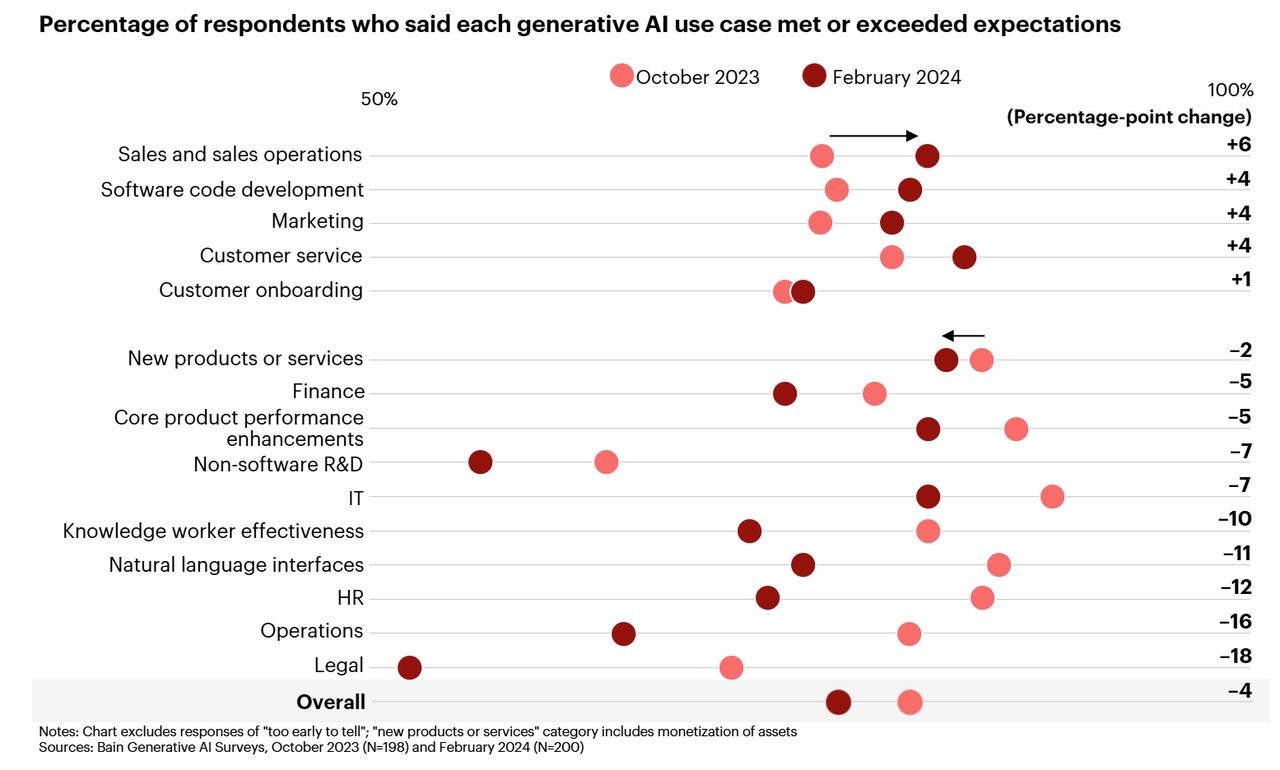

Expectations are being exceededMore than 80% of companies report that generative AI has met or exceeded their expectations. This underlines the immediate added value that AI can create in various business areas. - But not everyone is happy! (see picture)

Future priority60% of the companies surveyed see generative AI as a top 3 priority for the next two years. This indicates that the trend towards AI integration in companies will continue.

What do you think of these developments in the AI sector? Do you think that investments in AI will pay off in the long term?

I am convinced that investments in AI will pay off in the long term. The widespread use and significant investments show that the benefits are real. Of course there are risks, but the opportunities seem to outweigh the risks. I find the developments in software development and customer service particularly exciting, as immediate added value is created here. UGs (regardless of size) need to adapt to avoid being left behind.

I look forward to your opinions and an exciting discussion!

Source:

AI Survey: Four Themes Emerging | Bain & Company

Interesting stocks on the topic (don't hold any of the stocks mentioned):

$WIX (+1,17 %)

$GTLB (-3,67 %)

$GDDY (-1,63 %)

$APP (-3,3 %)

$ZENV

22

Titres populaires

Meilleurs créateurs cette semaine

Données en temps réel par LSX · Données financières de FactSet