MuM

Price

Debate sobre MUM

Puestos

30

Man and machine: the best quarter in the company's history to date

Man and machine has had 10 record years in a row. Business seems to be booming, but the share is not.

A European hidden champion with a global presence

Mensch und Maschine (MUM) is one of the leading developers of Computer Aided Design, Manufacturing and Engineering (CAD/CAM/CAE), Product Data Management (PDM) and Building Information Modeling/Management (BIM) with around 75 locations throughout Europe, Asia and America.

The business model is divided into the two segments M+M Software (standard software for CAM, BIM and CAE) and Digitalization (customer-specific digitalization solutions, training and consulting for customers from industry, construction and infrastructure).

The two segments each account for around half of Group sales, while M+M Software generates almost three quarters of the profit (EBIT).

The company's applications are used in a wide range of industries, including mechanical engineering, architecture/construction, infrastructure, electrical engineering, plant engineering, data management and so on.

Mensch und Maschine is broadly positioned and well diversified, with even its largest customer accounting for less than 1% of sales.

The biggest criticism of the company has always been its dependence on AutodeskMensch und Maschine has therefore consistently worked to reduce it.

Today, less than 20% of the Group's value added is attributable to Autodesk reselling. The former core business has long since been replaced by the company's own products.

Ten years in series production

For more than a decade, there has not been a year without growth at Mensch und Maschine, and for just as long, a new record profit has been achieved every year.

Ten record years in a row does not appear to be a coincidence, but a successful system.

During this time, profits have increased massively from EUR 0.40 to EUR 1.91 per share and the share has been a massive outperformer for long periods.

In the recent past, however, the share price has completely decoupled from the fundamental development. While earnings have continued to rise, the share price has been trending sideways for years and has really come under pressure in recent months.

We can only speculate as to the reasons for this, as the operating trend is clearly pointing upwards.

The fear of disruption from KI has exerted pressure on the share price in recent months. Another reason is probably chart technology. Falling share prices provoke falling share prices and exert mental pressure on shareholders, who at some point pull the ripcord out of frustration and impatience.

When fundamentals and share price diverge

There is also a change in the business model. The company used to buy software such as that from Autodesk itself and then sell it on to customers, thereby generating traditional trading margins.

In plain language: a lot of turnover, little profit.

This model is now gradually being replaced by a commission model. In this new model, Mensch und Maschine no longer sells Autodesk products in its own name. Instead, the customer concludes the contract directly with Autodesk, while Mensch und Maschine continues to handle sales and consulting. In return, the company receives a commission.

As a result of this change, the reported turnover is significantly lower because the throughput software revenues are eliminated. At the same time, however, the associated expenses are also reduced, so that the margin on the remaining revenue shares tends to increase.

In plain language, this means: less turnover, but the same or potentially even more profit.

At the Börse does not seem to understand this. There is no other way to explain the fall in the share price.

Sales illusion vs. profit reality

This transitional phase has now come to an end, making the underlying trends visible again. It can be assumed that the penny will also slowly drop on the stock market.

On April 21, the company presented an update on the first quarter of the current financial year.

Turnover increased by 8.4% to 71.6 million euros. At the same time, profitability improved, with EBIT increasing by 13.7% to 18.3 million euros.

Earnings even improved by 16% to EUR 0.73 per share, the highest quarterly figure ever.

Operating cash flow increased by 91% to EUR 19.1 million, which corresponds to EUR 1.17 per share.

Outlook and valuation

M+M founder/Chairman Adi Drotleff and CFO Markus Pech expressed their satisfaction: "Based on the strong start to the year and the reduced cost base, we are maintaining our targets for the current financial year 2026 unchanged, i.e. +11 - 19 % to 211 - 226 cents for EPS and EUR 54.5 - 58.5 million for EBIT, and are planning 220 - 240 cents Dividende after 200 cents for 2025."

As the company already earned EUR 0.73 per share in the first quarter and Q1 is often the weakest and Q4 the strongest quarter of the year, the outlook can be described as cautiously conservative.

In addition, the operating cash flow is likely to be higher than the reported profit.

Even if this point is ignored, Mensch und Maschine has a P/E ratio of 17.5 and a Dividendenrendite of 5.8 %.

The long-term average was KGV 37 and 35.8 in the last five years.

The Annual General Meeting is expected to take place on May 12. The dividend is expected to be paid out immediately afterwards

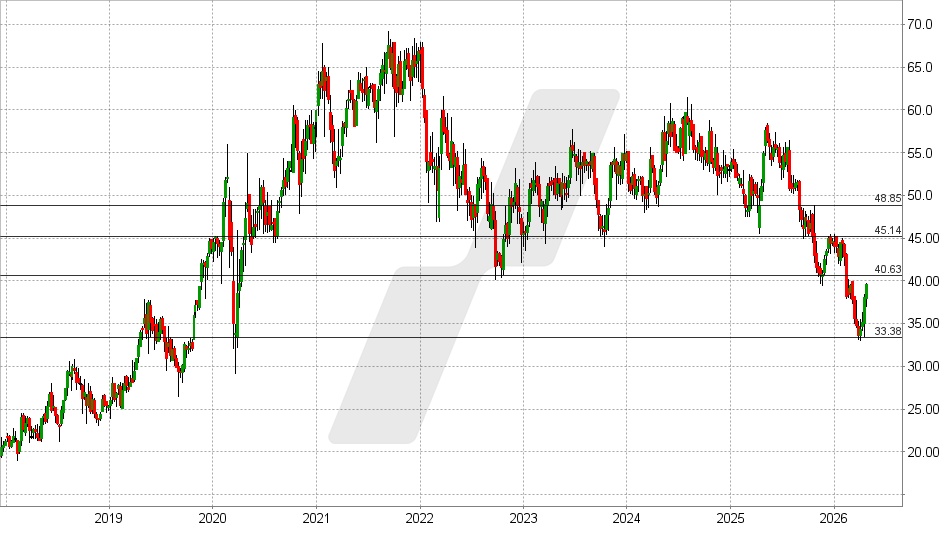

Mensch und Maschine share: chart from 21.04.2026, price: EUR 39.45 - symbol: MUM | source: TWS

The latest Quartalszahlen seem to have gone down well on the stock market. In response, the share price rose by almost 5% to EUR 39.45. The positive trend of the past week has thus continued.

If the share now manages to break out above the resistance band at 40.00 - 40.50 euros, a procyclical uptrend will ensue. Kaufsignal with possible price targets at EUR 45 and EUR 47.50 - 49.00.

However, if the share falls back below EUR 37.50, the bulls will have lost their chance for the time being

Source

Man & Machine

Hello everyone,

$MUM (-0,82 %) doesn't look good at all when you look at the chart. I can hardly or not at all assess this share. In principle, I would like to include this sector in my dividend portfolio. What do you think of the share or can you recommend alternatives?

Regards ✌🏽

Regards

What do you think of the company?

$MUM (-0,82 %) very interesting at first glance. A company with 3.8% dividends and very strong dividend growth in the technology sector...

In the last financial year, the values deteriorated... starting with sales.

Current recommendations on dividend stocks (DZ Bank)

The DZ Bank analysts have drawn up two lists of shares that they consider to be particularly attractive. For more defensive investors and for investors who rely on continuous cash flows, they recommend the so-called "dividend aristocrats": In other words, companies that have regularly paid and raised dividends.

Top dividend aristocrats:

Pfizer $PFE (+0,56 %), Verizon $VZ (+0,63 %), BNP Paribas $BNP (+1,19 %)Zurich Insurance $ZURN (-3,24 %), Enel $ENEL (+0,28 %), Sanofi $SAN (+0,23 %), Hannover Re $HNR1 (+0,56 %) , Man and Machine $MUM (-0,82 %), Generali $G (+1,03 %) and Allianz $ALV (+1,23 %)

Another list has been compiled for investors with a somewhat higher risk appetite: Stocks with attractive dividend yields and additional share price potential. These not only pay a good dividend of at least three percent, but could also increase significantly in price in the future. However, the continuity of dividends in the past plays a lesser role - and this strategy is correspondingly riskier.

Top dividend rockets:

Man and machine $MUM (-0,82 %) , Cancom $COK (-0,51 %), Bastei Lübbe $BST (-0,47 %), Sixt $SIX2 (+1,48 %), Kontron $KTN (+5,52 %), Fresenius Medical Care $FME (+1,8 %), Vonovia $VNA (-0,69 %), Hawesko $HAW (-2,23 %), ElringKlinger $ZIL2 (-4,55 %) and Hannover Re $HNR1 (+0,56 %)

Source text (excerpt) & graphic: World | AAA, 19.02.2026

Allocation by Irish sale

The idea of further diversifying my portfolio had solidified somewhat in recent weeks. $IREN (-0,38 %) I left it at my self-imposed partial sell target of EUR 55 and started to build up the first positions on Friday. I am sticking to my target of investing around EUR 5k in each position. $IREN (-0,38 %) remains in the portfolio with 500 shares and will (probably) not be touched in the near future. $DEFI (-1,31 %) Now also full with 5,500 shares.

19k liquidity left and will still be invested in top-ups + new shares.

Individual shares are now:

$DSFIR (-0,3 %) possibly increase

$MUM (-0,82 %) possibly increase

$FSLR (+0,73 %) Increase if necessary

$NICE Increase if necessary

Does anyone else have an idea for a share, possibly also from the German-speaking region? The Asian region would also be very interesting, although I am looking a little at $1810 (-3,18 %) look at.

vg and have a nice WE

Micha

Next step 150k

After September also provided a decent return, I'm hoping for 150k at the end of the year. I have also recently started betting on a boost of $DEFI (-1,31 %) . $KSPI (+0,75 %) is out for me with +20% after a good run.

A bit of "stability" is provided by $DSFIR (-0,3 %) and $MUM (-0,82 %) although I hope to have bought them at a relatively low level. We will see...

Otherwise, onwards:

good investment to all!