🇮🇷🇺🇸 Iran threatens to target world's largest oil company Saudi Aramco and key pipelines if President Trump attacks Iranian power plants.

Saudi Aramco

Stock

Stock

ISIN: SA14TG012N13

Ticker: 2222

SA14TG012N13

2222

Price

Debate sobre 2222

Puestos

12

4Lun·

Commodities | Nat gas continues to burn

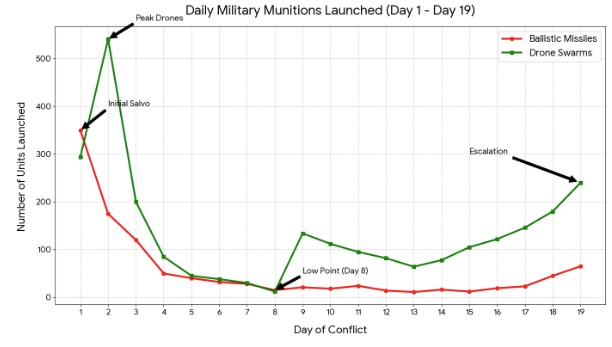

Israel and the USA have attacked the South Pars Gasfeldera joint project between Iran and Qatar. In response, the Iranians have declared that all energy infrastructure in the region is now considered a legitimate target. So far, they have attacked Qatari facilities, including the Ras Laffan Industrial City, a $NGAS (-3,73 %) hub, and report heavy damage. In addition, a $2222-refinery in Riyadh was also attacked.

The hit rate of Iranian attacks now also appears to be increasing, while the local air defense systems in some Gulf states also appear significantly weakened. The number of hits is also increasing.

The winners will continue to be fertilizer, drone manufacturers and defense tech.

1414

12 Comentarios

Drone manufacturers, you write together.

And speculating on food is anti-social. Has no one ever explained that to you?

And speculating on food is anti-social. Has no one ever explained that to you?

•

44

•4Lun·

Oil | Oil market under pressure

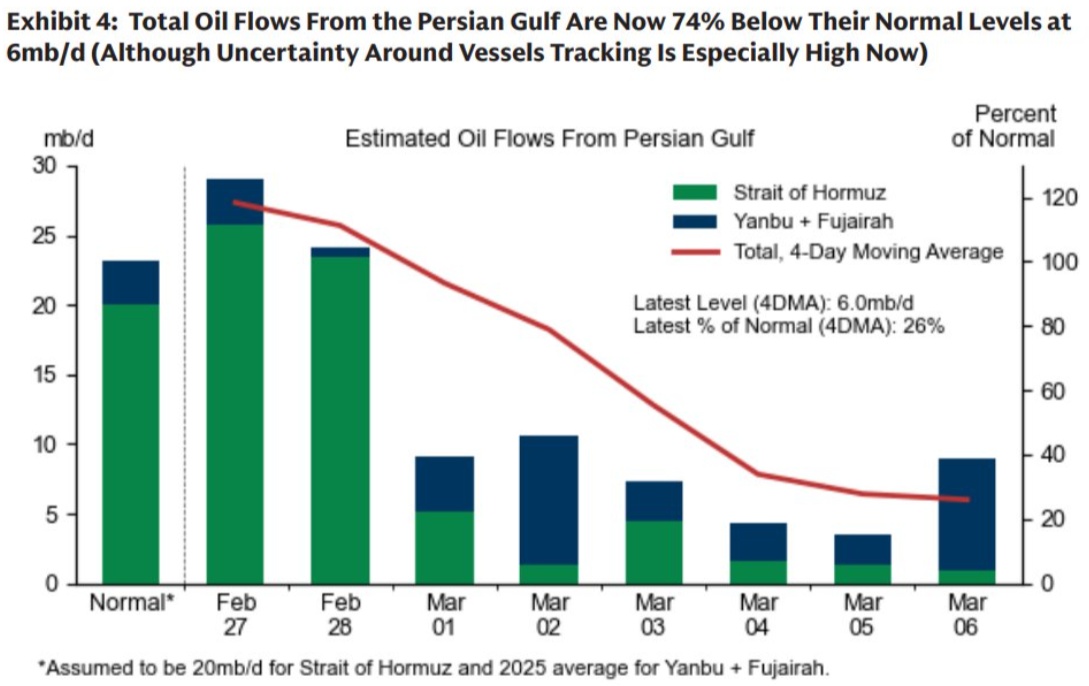

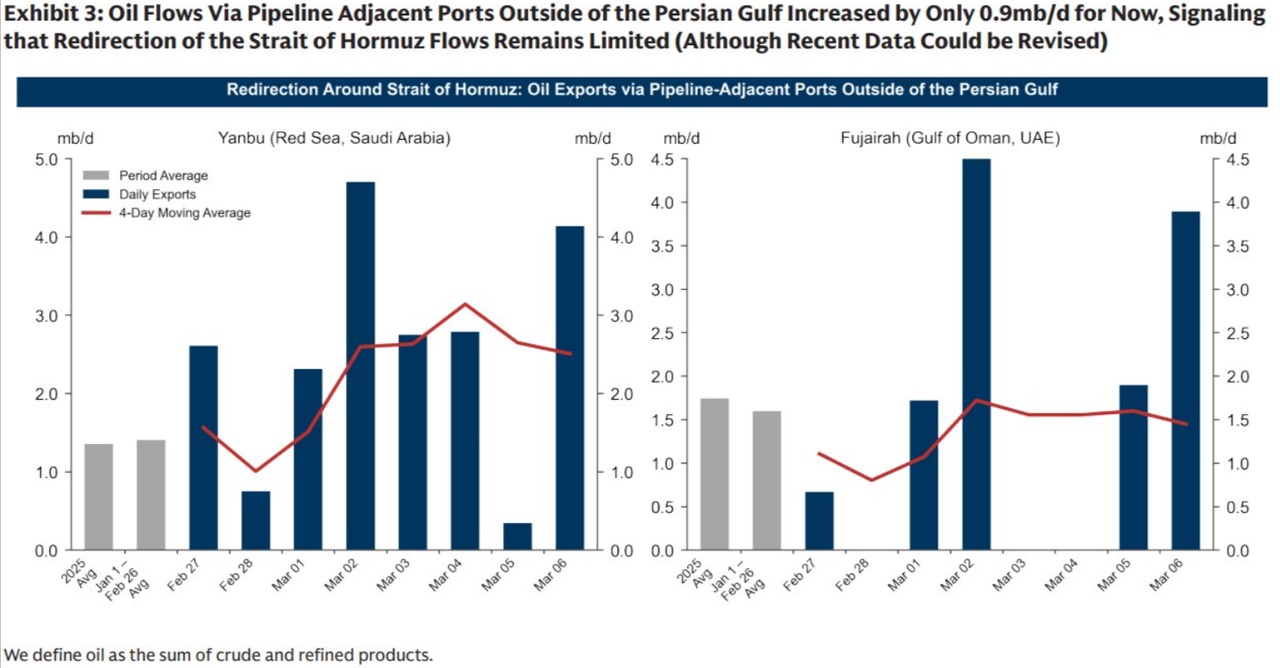

The geopolitical situation in the Middle East continues to deteriorate. According to General Cane of the US Department of War, the second phase of the war has now begun. Oil has (of course) reacted particularly to the second Iran war. In recent days, attempts have been made to transport the oil, which primarily flows through the Strait of Hormuz, via pipelines to ports such as Yanbu in Saudi Arabia or Fujairah in the UAE. The King Fahad Industrial Port in Yanbu is the largest exporter of crude oil, refined products and petrochemicals on the Red Sea with 34 berths and 10 terminals. It is used for $2222 as detour. Fujairah is a very good location for bunker oil and storage outside the Strait of Hormuz. The Fujairah Oil Terminal has 36 tanks with 1.2 million cubic meters of storage (approx. 18 million barrels) and 14 berths.

Currently, it can be stated that 4 mb/d was loaded onto VLCCs on Friday, giving a total of 8 mb/d. However, this is not in proportion to what is flowing through the Strait of Hormuz, 20 mb/d. They are currently trying to shift as much oil to ships to balance this out, but they are not succeeding. This is also due to the fact that oil storage facilities have now also become a target of the IRGC. On March 3rd, several drones hit the oil storage facility in Fujairah, which can be seen in the graphic, as no exports could take place and were still restricted on March 4th.

To see the extent of the current oil problem, an overview of total oil exports from the Persian Gulf is essential. This chart shows that flows have been reduced by 74%. Normally, around 20 mb/d flows through the Strait of Hormuz and 2.5 mb/d through the Yanbu and Fujaihra pipelines as a replacement/balancing valve. Due to the outbreak of war, the flow through Hormuz collapsed, partly due to fear of attacks by the IRGC and the closure by them on March 2nd (radio message).

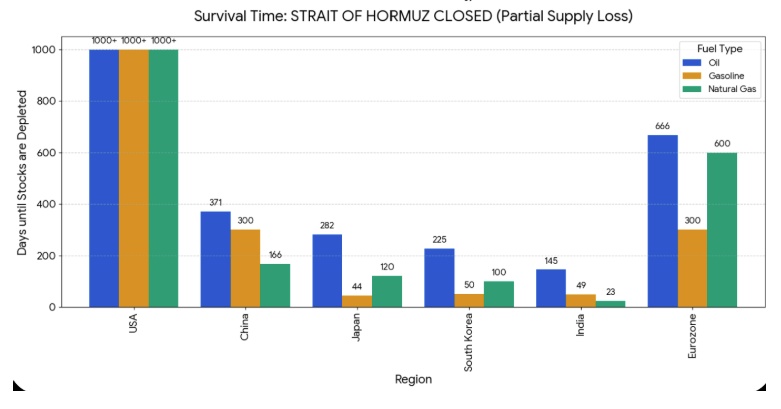

If you look at the strategic impact of a closure of the Strait of Hormuz, it hardly affects the USA, which can withstand +1000 days based on stocks. Countries in Asia, such as South Korea, Japan and to some extent China, are particularly affected, especially for gas. Europe is strategically moderately to well "prepared". The only problem is with gasoline. Those countries run the risk of having to buy expensive oil in order to maintain their normal operations.

1919

40 Comentarios

Now it's getting dangerous because a spiral has started! Oil price up => inflation => interest rates go up => recession => stock market crash 💣 I think we're in for a very uncomfortable time folks!

Last week was the most extreme rise in oil prices since 1982! Back then there was also a stock market crash and if it turns out stupidly, we will see the same thing again, only MUCH WORSE, because this time the AI fears are added and a madman is sitting in the White House!

If this scenario happens, then expect a crash of more than 70%!

Last week was the most extreme rise in oil prices since 1982! Back then there was also a stock market crash and if it turns out stupidly, we will see the same thing again, only MUCH WORSE, because this time the AI fears are added and a madman is sitting in the White House!

If this scenario happens, then expect a crash of more than 70%!

•

1313

•

1Año·

Oil price analysis

Price decline

OPEC+ countries

Brent futures curve

Oil supply

Kazakhstan

Trade war

Price target

Link: https://shorturl.at/asfT7

$SHEL (-1,39 %)

$TTE (-3,6 %)

$CVX (-1,6 %)

$XOM (-0,87 %)

$BP. (-3,82 %)

$OXY (-1,2 %)

$SLB (+2,73 %)

$2222

$ENI (-1,33 %)

shorturl.atAttention Required! | Cloudflare

55

3 Comentarios

The link is about derivatives on the oil price. But I see another good trading opportunity. Because contrary to the assumption in the article that they want to hit countries like Kazakhstan and Iran, I see a completely different target. That is the US fracking industry. The USA is now the largest single producer in the world due to the immense investments in this sector. 13.5 million barrels per day. This is a thorn in OPEC's side, as it jeopardizes OPEC's supremacy. So they are trying to use the oversupply to push prices so low that the business is not worthwhile for the fracking companies. Donald Trump is satisfied with expensive Arab investments in other areas and has long since deviated from his drill baby drill actions. He knows full well that US citizens are more enthusiastic about falling energy prices, regardless of what causes them. It could therefore be interesting to bet on falling prices for US fracking companies.

Yesterday, OPEC announced a further increase in production quotas of over 400,000 barrels/day from July 1.

Yesterday, OPEC announced a further increase in production quotas of over 400,000 barrels/day from July 1.

•

55

•

1Año·

Europe's defense stocks rise after Selensky-Trump dispute | Aramco expects results - forecast

European defense stocks rise after Selensky-Trump dispute

Shares in the defense industry experienced a strong upswing on Monday, and there are good reasons for this. The trigger was the scandal between Ukrainian President Volodymyr Selenskyj and US President Donald Trump, which brought talks on a raw materials agreement and security guarantees to a standstill. This uncertainty has prompted investors to bet on defense stocks in the expectation that defense spending in Europe will increase.

Rheinmetall $RHM (+1,28 %) reached a new record high in the DAX and closed with an impressive gain of 13.71% at EUR 1,144.50. This means that the share has already gained 80 percent since the beginning of the year. HENSOLDT $HAG also benefited from the general euphoria and closed up 22.25 percent at 64.00 euros. Shares in thyssenkrupp $TKA (+2,84 %) rose by 10.57 percent to 8.41 euros, while RENK $ABBV (-0,77 %) rose by 18.90 percent to 35.52 euros.

Analysts agree that geopolitical tensions and uncertainty over US policy will boost defense spending in Europe. Jürgen Molnar from RoboMarkets emphasizes that the world has changed after the scandal and that Europe can no longer count on the USA as a reliable partner. JPMorgan analyst David Perry points out that many NATO countries will increase their defense spending in the near future, which could further boost demand for defense stocks.

Forecast: Aramco expects results

Saudi Aramco $2222 is about to announce results for the quarter ending December 31, 2024. Analysts estimate that earnings per share will come in at 9.3 cents, down from 11 cents in the same quarter last year.

For sales, analysts expect a decline to an average of EUR 103 billion, which corresponds to a decrease of 11.69 percent compared to the previous year. Last year, Aramco recorded sales of EUR 117 billion. For the past fiscal year, analysts expect earnings of EUR 0.42 per share, compared with EUR 0.48 per share in the previous year. Total sales are estimated at EUR 450 billion, which also represents a decline compared to last year.

Sources:

33

1 ComentarioIf it wasn't so sad what is happening on this planet at the moment, then as a Thyssen investor you would actually have to be happy about the development of the share. But I never really wanted to profit from armaments.

•

44

•

1Año·

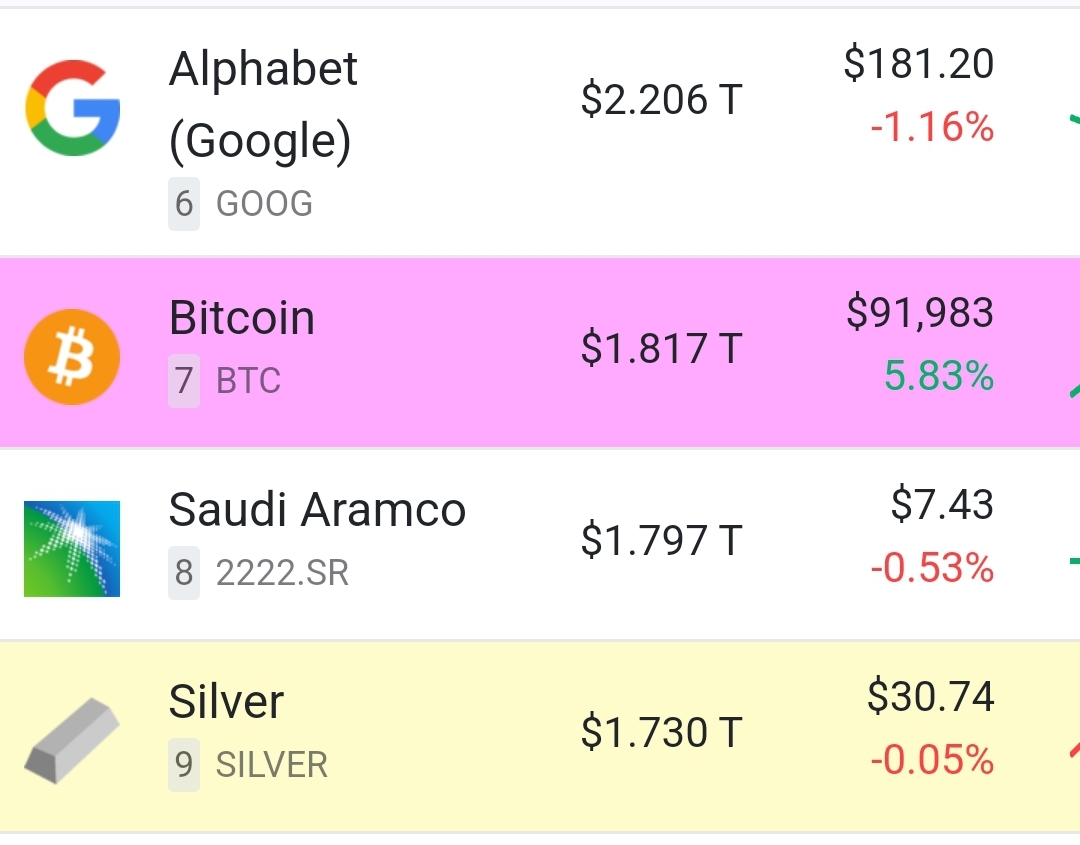

Let's move on!

$BTC (+0,01 %)

has now also $2222

flipped🚀

Next comes $GOOGL (+2,02 %) 😁

BTW: have I ever mentioned that I love the push messages from Strike?😂

2121

7 Comentarios

Would be another quarter of market cap on top phew😅🫣

•

33

•

1Año·

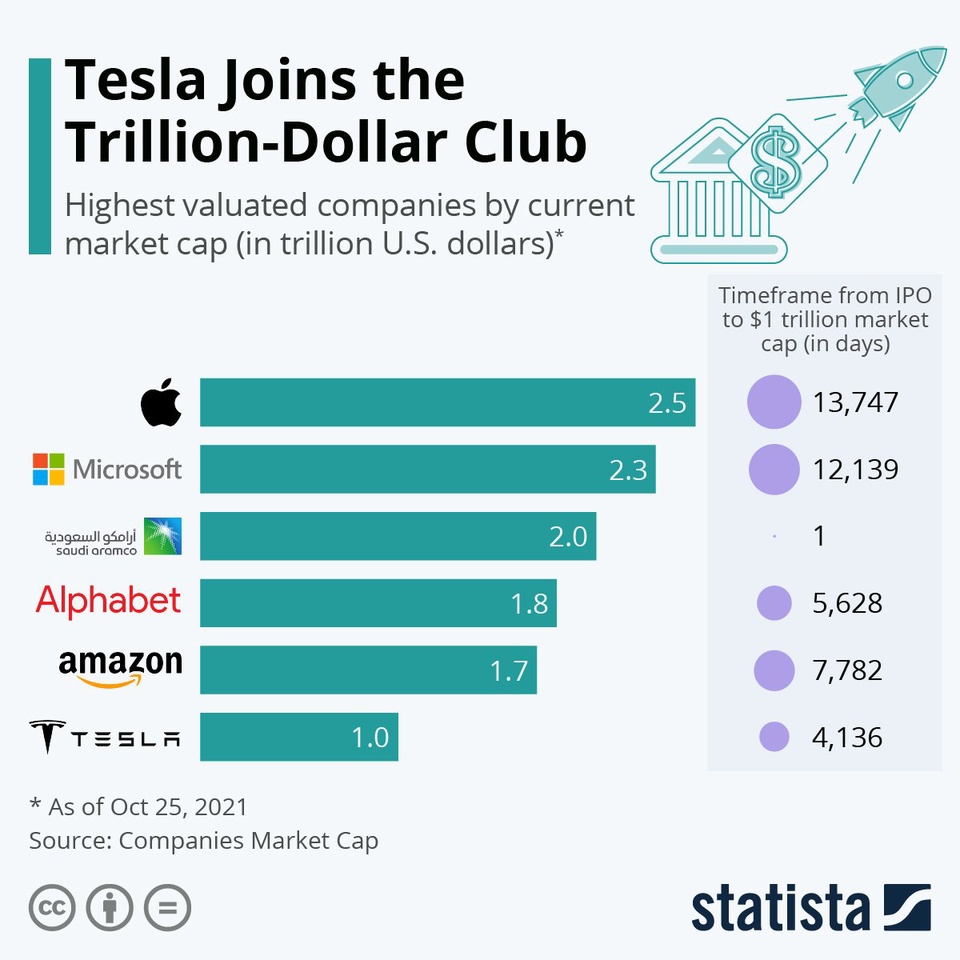

On this day in 2021 $TSLA (+0,92 %)

joined the 1 trillion market capitalization club for the first time

99

1Año·

Companies with trillion dollar valuations:

Apple: $3.5 trillion - $AAPL (+2,28 %)

Nvidia: $3.1 trillion - $NVDA (+3,53 %)

Microsoft: $3 trillion - $MSFT (+1,18 %)

Alphabet: $2 trillion - $GOOGL (+2,02 %)

Amazon: $1.8 trillion - $AMZN (-1,42 %)

Saudi Aramco: $1.7 trillion - $2222

Meta: $1.3 trillion - $META (-0,36 %)

Berkshire Hathaway: $1 trillion $BRK.B (+0,46 %)

Source: Jon Erlichman

66

3 Comentarios

1Año

If you're interested, you can find up-to-date numbers and some additional assets here: https://8marketcap.com/

•

55

•

3Año·

The bear is dancing! 🐻 - 5 Bearish Scenarios for Western Oil Stocks.

The oil industry has been battling massive media headwinds in the public eye since as early as the 1980s. Nevertheless, the saying proves true: "Those who are believed dead live longer!" proves true again and again.

In the following, I have listed some points that could indeed trigger bearish scenarios in the Western oil and gas sector. The probabilities for it are quite given, although these are now realistic, I am not able to judge with the contribution.

1. decoupling of the world markets

Many of you must have heard about it in the news. China is currently mediating in the dispute between the oil powers Saudi Arabia and Iran. It is said to amount to reconciliation and a new alliance is to be forged.

Oil trade, explicitly between Saudi Arabia and China, is then to be traded via the yuan (the Chinese currency).

What does this mean? Currencies have no material value. They are printed numbers with a sometimes fancy design intended to facilitate trade in a country or currency union. Behind this piece of paper, however, is always the respective person's imagination of the economic power of the respective nation. Almost all international trade is in U.S. dollars.

Saudi Arabia owns about 13% of the world's oil reserves (according to OPEC statistics). Not for nothing is Saudi Aramco $2222 has at times been the most valuable company in the world. China, on the other hand, is one of the largest buyers of oil. If one now transacts this trade in yuan, one suffers a relatively high loss of value in the dollar. The prices of WTI or Brent, which are tradable for us, would inevitably lose value as well, as demand collapses accordingly. (Long-term view)

In addition, we should continue to monitor China's activities with regard to Iran. After all, Iran also has huge oil reserves that cannot participate in the market at the moment due to the nuclear dispute and the resulting embargo.

2. persistently high prices

Persistently high prices could also spell doom for our oil industry. At present, it is true that money is being made strongly and shareholders can enjoy dizzying records. Nevertheless, the search for alternatives is becoming more attractive. The high demand from the industry may topple as soon as the high prices cannot be passed on to the end consumer, as this would again lead to demand deficits and increased supply. This leads to production cuts and ultimately to demand problems for oil.

The search for alternatives becomes more attractive, as high oil prices make one attractive to the overall market. This does not necessarily spur renewable energy sources. Relatively low coal and gas prices also lead to a reorientation on the energy markets. This can be read particularly clearly from the prices of the respective commodities from 2022. With the difference that the scenario was true for gas.

3. political environment

The following scenario is itself very unlikely, since the lobby in the EU can enjoy quite a lot of influence. Nevertheless, one is quite capable of surprises.

Suppose political environment in a large economic area changes rapidly. This can mean various legalities.

As an example, I take the decoupling of alternatives from oil and gas products. Biofuels could be fully more competitive, or a tax break, as in the 2000s could be a consequence. As a result, demand for oil fell just as sharply, and the federal government consequently rescinded the tax break and passed the Fuel Quota Act to compensate.

4. speculative bubbles in emissions trading

Many may not be familiar with it. In the EU, emitters are obliged to compensate for their emissions. In this case, the responsible companies have to buy certificates for this purpose. However, every emitter participates in this market. Accordingly, it can lead to speculation bubbles forming here as well. The corporations pass these costs on to the consumer. Accordingly, the respective economic good naturally becomes more expensive.

However, this emissions trading system is not limited to the EU. China and other countries also have such trading systems, although the prices there are rather symbolic in comparison.

In addition, there are of course national emissions trading systems, such as the one we have in Germany with the so-called CO2 pricing.

5. overthrow in own rebuilding

The petroleum companies on the European continent in particular are almost outdoing each other with their sustainability goals.

While Total $TTE (-3,6 %) has nevertheless been able to solidly claim the gas market in the LNG sector for itself, Shell hardly plays a significant role in it. $SHEL (-1,39 %) hardly plays a significant role in it. Overall, in the liquefied natural gas market, US brands such as. $LNG (-0,51 %) , $CVX (-1,6 %) and $COP (-1,39 %) have established themselves.

Please note that this is the fossil market. In the renewables sector, Shell, in turn, already plays a quite considerable role.

BP $BP. (-3,82 %) on the other hand, is rather cautious and timid in this respect. Rightly so?

Of course, this cannot be said across the board, since no one can reliably predict the future, especially the general conditions for the future. Nevertheless, the restructuring of the petroleum companies costs an enormous amount of capital and destroys their original business model. It is therefore necessary to venture into new and uncertain sectors, into markets that are already dominated by other well-known companies. The risk of losing market share both in the oil industry and in the so-called "future industries" is therefore very high.

77

9 Comentarios

3Año

Thanks for your work ! I must admit that it is not really my field of interest 😅, nevertheless once again worth reading, like all your other contributions too 🤝

•

22

•

3Año·

getquin Daily Summary 10.10.2022

Hello getquin,

have a nice monday to all of you.

Europe🌍:

1. alliance expects inflation to rise further

Ahead of the release of the latest consumer price index this week, Mohamed El-Erian, Allianz's chief inflation advisor, said he expects headline inflation "probably to come down to around 8%" but core inflation "still rising."

Read more: https://cnb.cx/3Cm1tcb

🟩 $ALV (+0,44 %) 165,32€ (🔼🔽 +0,62%)

America🌏:

2nd Rivian Automotive recalls almost all vehicles

The vehicles of Tesla, competitor Rivian, probably have a steering problem, which the automaker now wants to fix. To do so, Rivian is recalling about 13,000 cars built from 2021 through this September. Rivian is one of Tesla's larger competitors, with Amazon and Jeff Bezos also among its owners.

Read more: https://on.wsj.com/3rGHXCr

🟥 $RIVN (+1,49 %) 31,10$ (🔽 -8,38%)

Asia🌏:

3. Saudi Aramco delivers fully to North Asia despite OPEC restriction

Saudi Aramco has told at least five customers in North Asia that they will receive the full contracted amount of crude oil in November, several sources familiar with the matter said Monday. The full supply allocation comes despite the decision by OPEC+, including Russia, to cut its production target by 2 million barrels per day. By lowering output, OPEC+ countries intend to further fuel oil prices. U.S. Treasury Secretary Yellen sees this as a major threat and thinks this development could trigger a global recession.

Read more: https://cnb.cx/3CLARTl

🟥 $2222 9,80€ (🔽 -0,69%)

Stocks of the day:

🟩 TOP $1COV (+0 %) 33,50€ (🔼 +8,98%)

👍 postitive estimates of quarterly results boost share price

🟥 FLOP $F (-1,78 %) 12,06€ (🔽 -5,00%)

👎 Analysts expect Ford and all other U.S. automakers to see profits slump by approx. 50%

🟥 Most searched $MSFT (+1,18 %) 236,40€ (🔽 -1,59%)

🟩 Most traded $TSLA (+0,92 %) , 228,45€ (🔼 +0,10%)

🟥 S&P500, 3,615.50 (🔽 -0.66%)

🟩 DAX, 12,317.20 (🔼 +0.36%)

🟥 bitcoin ₿, 19,889.25€ (🔽 -0.41%)

Time: 17:10 CEST

88

1 Comentario

Also nice $MPW announces share buyback program of $500M by oct 2023 https://www.businesswire.com/news/home/20221009005054/en/Medical-Properties-Trust-Announces-Authorization-of-Stock-Repurchase-Program

•

88

•Valores en tendencia

Principales creadores de la semana

Datos financieros de FactSet