After eight weeks of global outflows totaling $8 billion, sentiment toward crypto investment products has recently stabilized. Declining inflation data has $BTC (-0.97%) helped in the short term, as investors are once again betting more heavily on potential interest rate cuts.

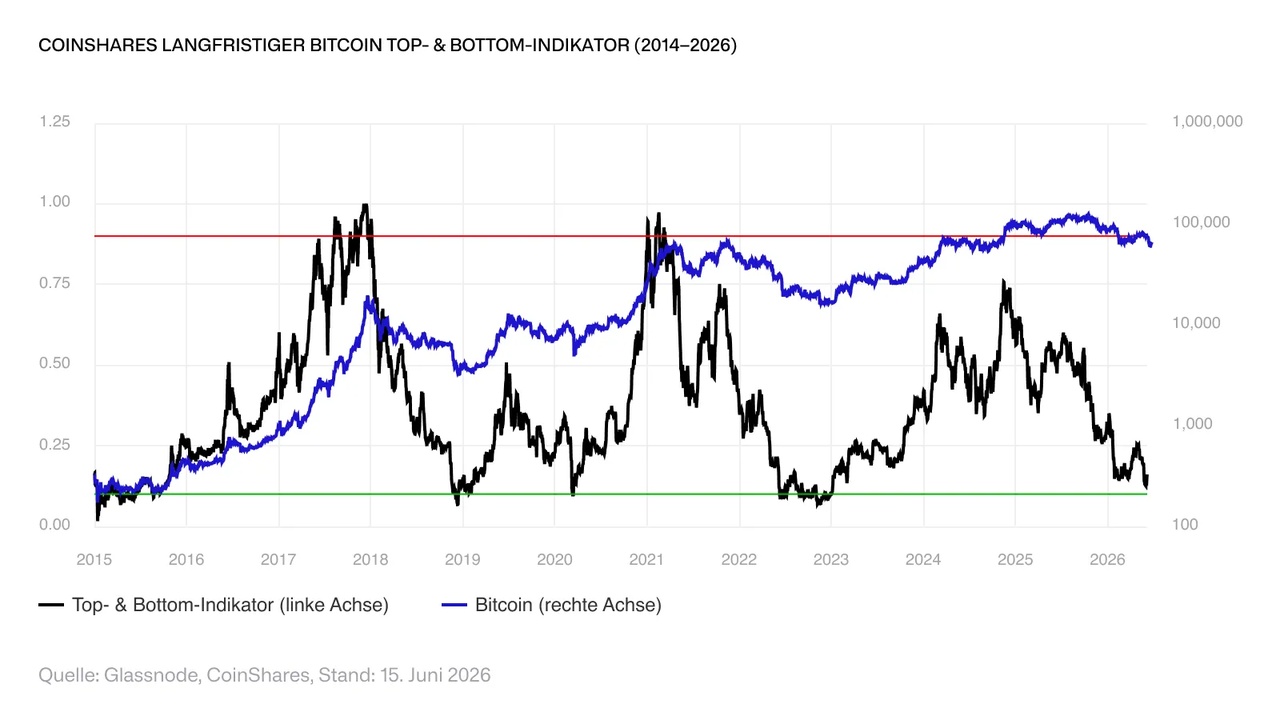

Nevertheless, the picture remains mixed: The bottom #bitcoin is likely close or has already been reached. However, the catalyst for significantly higher prices is still missing. Without a clear shift in interest rate expectations, $BTC (-0.97%) it is likely to trade sideways for the time being. A breakout above $80,000 currently seems unlikely.

(Author: James Butterfill, CoinShares’ Head of Research)

You can invest in Bitcoin through the following vehicle: $BITC (-0.9%)