Second recap this year, performance even worse. I know that headline doesn’t sound great, but you have to look a bit deeper and understand my investment philosophy before judging the result.

The portfolio was down almost 9% in February, which mainly comes down to a few factors. First, some of my previous winners erased their gains entirely or even drifted into the red. Nvidia, Visa and MercadoLibre are good examples. I don’t use stop-losses because I assess companies holistically and don’t base sell decisions purely on price movements.

I generally sell for two reasons. The first is when the investment case I originally signed up for is no longer intact. That’s why I sold Fiserv a few months ago after they slashed guidance and effectively reset the company by pushing out management. It’s also why I sold Novo Nordisk when the story shifted from a slower-growing but still dominant player to something far less attractive: declining revenue, margins and free cash flow.

The second reason is when I believe there are simply better opportunities elsewhere in the market. That happened this month when I sold my T-Mobile US position to double down on some of my higher conviction and higher upside names like Microsoft, Zeta and ServiceNow.

Another reason my portfolio didn’t perform well last month is that I don’t use technical analysis. I don’t mind buying into a falling knife because I evaluate companies based on their fundamentals. Nobody knows whether a stock rebounds the day after a 30% drawdown or moves sideways for two years. But if I believe a company is a strong long-term compounder with clear upside, I’m not going to avoid it just because it could drop another 10%. In some cases I’ll even add more.

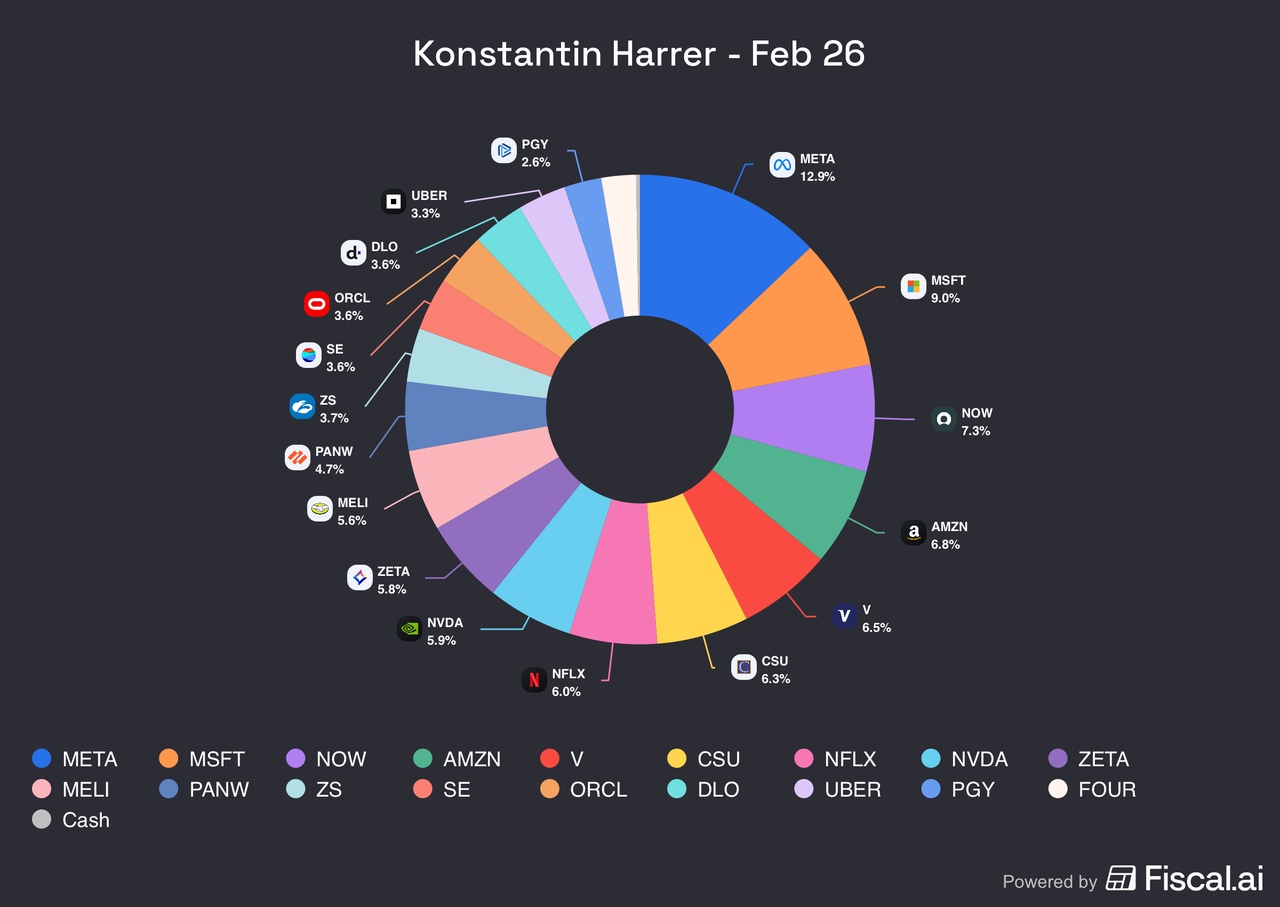

And that’s exactly what I did last month. I bought quite a few stocks, particularly in software and cybersecurity, because I think the market is mispricing some, though certainly not all, of those businesses. I added to Microsoft, ServiceNow, Palo Alto, Zscaler, Oracle and Amazon when they reached levels I considered attractive. And no, I didn’t always buy the exact bottom. That was a conscious decision.

A good example is Amazon. I bought the first half of my position before earnings at around $210 because I thought it was already an attractive entry. Then the stock sold off towards $200 and I added again. If I had waited for $190, I might never own the stock and would be kicking myself two years from now if it’s up 50%.

So yes, February doesn’t look great if you only look at the performance number. But what I actually did during the month was add to some exceptional long-term compounders. Some of them are so obvious that you almost want to call them no-brainers, even though you’re technically not supposed to say that.

But let’s be honest. Google was a no-brainer last year. Meta was, and arguably still is, a no-brainer at around 20x forward earnings while growing revenue at 20%. Microsoft might be the highest quality business in the world and trades at roughly 23x forward earnings.

My cash position is practically zero right now. While I do think the broader market has run fairly hot over the past year, there are still some extraordinary opportunities out there.

February Performance: -9%

Performance since inception: -2.8%

$META (+2,62%)

$AMZN (+6,74%)

$MSFT (+3,6%)

$NOW (+1,39%)

$V (+0,06%)

$CSU (+0,83%)

$NFLX (-1,74%)

$NVDA (+2,15%)

$ZETA (+0,86%)

$MELI (-0,65%)

$PANW (+1,58%)

$ZS (+1,76%)

$SE (+0,33%)

$ORCL (+0,38%)

$DLO (+0,96%)

$UBER (+0,59%)

$PGY

$FOUR

$TMUS (-0,53%)