$M (+0,77%) stock surges nearly 20% after Q2 delivers strongest same-store sales growth in 3 years (+1.9%) and beats expectations. CEO Tony Spring’s turnaround plan, including store revamps & closures, drives optimism despite tariff challenges.

Discussão sobre M

Postos

15

1Mês·

Macy’s Q2’25 Earnings Highlights

🔹 Revenue: $4.8B (Est. $4.69B) 🟢; -2.5% YoY

🔹 Adj. EPS: $0.41 (Est. $0.19) 🟢; -23% YoY

🔹 Macy’s SSS: +0.8% owned; +1.9% O+L+M

Guidance (FY25):

🔹 Revenue: $21.15B–$21.45B (Est. $21.2B) 🟢

🔹 Adj. EPS: $1.70–$2.05 (Est. $1.78) 🟢

🔹 Comparable O+L+M Sales: down ~1.5% to -0.5% YoY

🔹 Go-Forward O+L+M Sales: down ~1.5% to flat YoY

🔹 Adj. EBITDA Margin: 7.4%–7.9%

Q2 Comparable Sales:

🔹 Macy’s Inc.: +0.8% owned; +1.9% O+L+M

🔹 Macy’s (nameplate): +0.4% owned; +1.2% O+L+M

🔹 Reimagine 125: +1.1% owned; +1.4% O+L

🔹 Bloomingdale’s: +3.6% owned; +5.7% O+L+M

🔹 Bluemercury: +1.2% owned (18th straight quarter of gains)

Other Revenue:

🔹 Other Revenue: $187M; UP +18% YoY

🔹 Credit Card Rev: $153M; UP +22% YoY

🔹 Macy’s Media Network: $34M (Flat YoY)

Other Metrics:

🔹 Adj. Net Income: $113M; DOWN -24% YoY

🔹 Adj. EBITDA: $393M; DOWN -10% YoY

🔹 Gross Margin: 39.7%; DOWN -80bps YoY

🔹 SG&A: $1.9B; DOWN -$29M YoY (38.9% of sales, +20bps)

Balance Sheet / Liquidity:

🔹 Cash & Equivalents: $829M

🔹 Total Debt: $2.6B (reduced ~$340M via refinancing; no major maturities until 2030)

🔹 Inventories: DOWN -0.8% YoY

Shareholder Returns:

🔹 Dividend: $0.1824/share; $50M paid in Q2

🔹 Buybacks: $50M (4M shares in Q2; 12.6M shares YTD, $151M)

🔹 $1.2B remaining under $2.0B authorization

CEO Commentary (Tony Spring):

🔸 “Our teams achieved better than expected top- and bottom-line results, driven by our strongest comparable sales growth in 12 quarters.”

🔸 “Performance highlights the advantages of being a multi-brand, multi-category, omni-channel retailer.”

🔸 “Enterprise-wide improvements, with a strong focus on customer experience, give us further confidence our Bold New Chapter initiatives can drive long-term profitable growth.”

44

1 Comentar

G_Lappas10@G_Lappas10

1Mês

••

5Mês·

Today’s Screen

Today, I’m looking for stocks with > 10% Shareholder yield, FCF yield, and Earnings yield (my personal magic formula) but I’ve also included > 10% Tangible BVPS (5 year) CAGR and a minimum market cap of $500 million for this screen. This combines lots of data into one simple screen covering quality, valuation, and shareholder orientation, while eliminating the smallest companies with skewed numbers.

I like to screen until I’m down to 10-30 stocks, to generate a list of quality companies, trading at fair or below fair prices, to dig deeper into. Here are today’s results:

I currently own Chord and Crocs in different portfolios. Have owned Tri-Point Homes, United Airlines, and Macy’s in the past.

22

7Mês·

Macy’s Q4 Earnings Highlights:

🔹 Adj. EPS: $1.80 (Est. $1.54) 🟢

🔹 Revenue: $7.77B (Est. $7.76B) 🟢; -4.3% YoY

🔹 Inventory: $4.47B (Est. $4.38B) 🟢; +2.5% YoY

🔹 S.S.S (Owned): -1.1% (Est. -0.09%) 🔴

FY Guide:

🔹 Revenue: $21.0B-$21.4B (Est. $21.66B) 🔴

🔹 Adj. EPS: $2.05-$2.25 (Est. $2.31) 🔴

🔹 Comp Sales: Down ~2.0% to -0.5% vs. 2024

🔹 Go-Forward Comp Sales: Down ~2.0% to flat vs. 2024

🔹 Adj. EBITDA Margin: 8.4%-8.6% of revenue

11

10Mês·

From 18-year-old wannabe investment banker to successful private asset manager: my (bumpy) path to €300,000 in a custody account

In Part 1 I described my start as an investor from 2010 to 2016. Despite loss-making investments and bad decisions (buying AT&T instead of Amazon), I was able to achieve a portfolio value of €35,000. These experiences were to lay the first foundation stone for my future successful investment strategy (https://app.getquin.com/de/activity/PElWrODsmV)

In part 2 I talk about further setbacks in 2017 and 2018 and how the purchase of MasterCard shares marked the turning point in my investment career. Despite initial losses and professional dissatisfaction, I realized that my original strategy wasn't working and discovered the "dividend growth" for me. With a new professional position and a solid salary, I was finally able to really hit the ground running in 2019 (https://app.getquin.com/de/activity/LUkWiLtZKX)

In part 3 it will now be about the years 2019 to 2021 will be discussed. In these 3 years, my portfolio has increased fivefold. From €40,000, it went up to €199,000 in the meantime. But not everything was positive here either. During this time, I also made the two worst trades of my investment career. In addition to Wirecard, there were two other equity investments that resulted in losses of over 80%.

The year 2019 & the first share savings plans:

The year 2019 started with a portfolio balance of ~€40,000 and after my MasterCard purchase in December 2018, my major portfolio reorganization was to continue directly at the beginning of 2019. So in the first four months with Tencent $700 (+0,67%)

Intel $INTC (-6,85%)

Salesforce $CRM (-0,27%)

Alphabet $GOOG (+2,09%) and Meta $META (+0,55%) (then still Facebook), five more tech stocks were added to my portfolio. In return I have BHP Billiton $BHP (-0,59%)

Macy's $M (+0,77%)

and Hugo Boss $BOSS (-0,02%) sold.

Later in the year, the shares of Mercedes $MBG (+0,6%)

and AT&T $T (+1,78%) were also removed from the portfolio.

In addition to further acquisitions such as Pepsi $PEP (-0,05%)

Nextera Energy $NEE (+0,93%)

or Xylem $XYL (+0,1%) I also recognized the benefits of share savings plans in 2019 and started to set up a pure "savings plan custody account". At that time, this was still done via comdirect or Consorsbank and each savings plan execution cost a fee of 0.75%.

Another sale in 2019 was the Gamestop-share $GME (-1,01%) . Bought in 2016 to have something to do with gaming in the portfolio, but not taking into account that stationary sales are becoming less and less relevant. In the end, the share price fell by 85% - unfortunately, this was long before the memestock hype emerged.

My portfolio rose to ~€67,000 in 2019 and achieved a return of 23%. However, this was still well below the MSCI World and the S&P 500.

The year 2020 - Corona, Wirecard bankruptcy & 100k before 30 in the portfolio

2020 - a year that few of us will probably forget. While everything was still going reasonably smoothly in January and February 2020, chaos was set to break out from mid-February/March.

The first few weeks of 2020 had given rise to hopes of a very positive development in my portfolio. From the beginning of January to mid-February, my portfolio rose by almost €10,000 to €77,000.

Panic then slowly set in from mid-February. I still remember exactly how trading on the US stock markets was repeatedly suspended for short periods and daily losses of 10% were normal. At 0 o'clock sharp, I looked at the US futures and in seconds the futures went down by -5%. A cap for the futures, the futures loss must not be higher and you knew the next morning it would end badly for the DAX.

But when there is blood in the streets, you can make very good deals! So in March 2020 I bought the Allianz

$ALV (+0,36%) for €118. This gives me a personal dividend yield of almost 12% based on the current dividend of €13.80. Unfortunately, I only bought for €1,000 in total.

Also Starbucks

$SBUX (+1,05%) I was able to buy for less than €50.

The stock market crash continued until the Fed made short work of it and ended the crash single-handedly. The crash was ended with interest rate cuts and massive money printing and once again the saying "Never bet against the FED" proved to be true.

The stock markets then went through the roof and within a very short space of time were already back to a positive level compared to the end of 2019. Every share that somehow falls under the term "stay at home" was suddenly the hot tip on the stock market. Whether the Peloton $PTON (+3,46%)

or Teladoc $TDOC (+7,63%) everything went through the roof.

I let myself get carried away and did about 10 "Stay at Home" hype stocks into a growth savings plan portfolio. Of these, at the end of 2024 with Sea $SE (-0,93%) and MercadoLibre $MELI (+0,9%) only two shares remained. It goes without saying that most of them left the portfolio at a loss.

But 2020 was also the Wirecard year $WDI BaFin's ban on short selling, a year-long audit by EY, political backing and massive investments by German fund managers from DWS, UnionInvest and Deka vs. a journalist from the Financial Times.

Wirecard's claims that the journalist was in cahoots with short sellers and the backing from various institutions were unfortunately too credible for me.

When Wirecard faced the press and announced that EUR 2 billion could no longer be found, things went downhill and it became clear to everyone that the company was heading for insolvency. Before trading was suspended, I was able to sell my shares at a 50% loss and got off lightly.

Later in the year, I was able to conclude an extremely favorable leasing offer and sell my private car. The proceeds went straight into my securities account and I broke the €100,000 barrier in November 2020.

My portfolio then ended the year with a value of ~€120,000. At +5%, my performance was pretty much in line with the MSCI World.

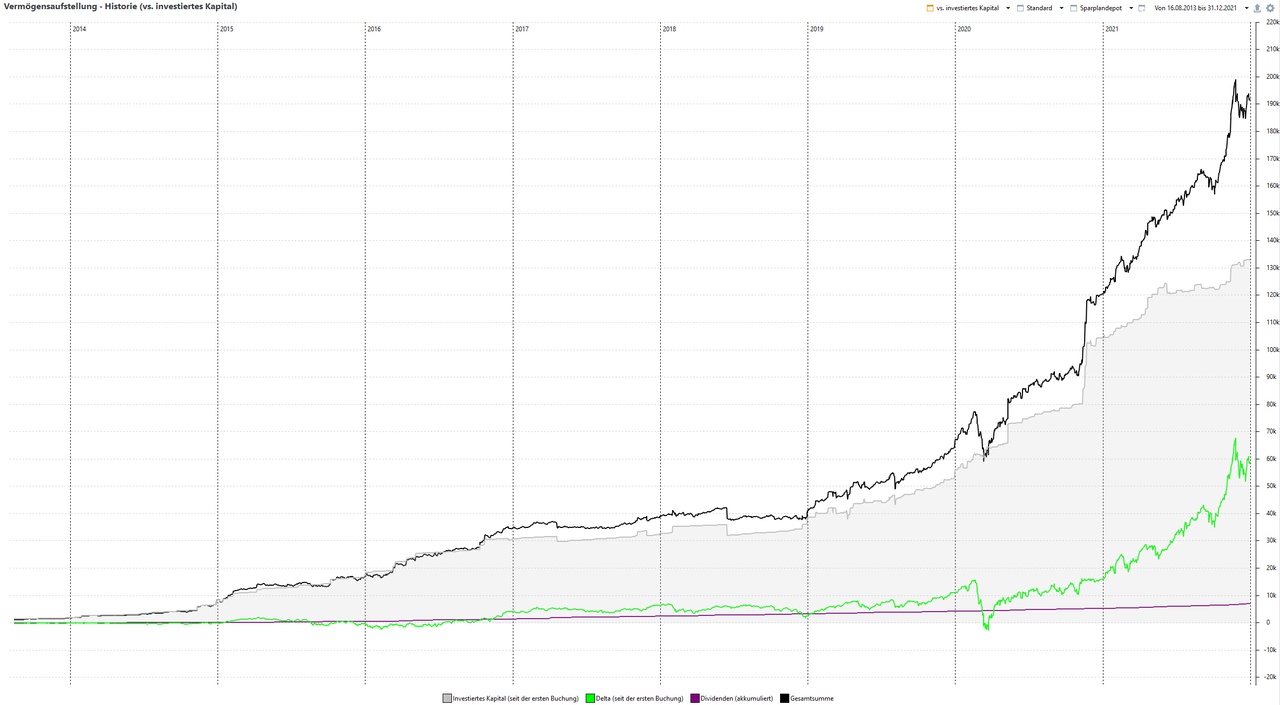

The year 2021 - HYPE! Wall Street bets, crypto and almost 200k in the portfolio

The year 2021 was characterized above all by hypes. Cryptocurrencies, memestocks and memecoins were in the headlines everywhere. Gamestop, Dogecoin, SPACs and NFTs everyone had to have.

Traditional shares became almost boring.

One of the reasons was certainly the checks that the US government issued to its citizens. It was still Corona, many were locked down and suddenly people started gambling on the stock market.

The hype can be illustrated very well using the example of NFTs. In 2021, NFTs worth $17 billion were traded, in 2023 it was only 80 million - a decline of 97%. According to one study, ~95% of all NFTs are now completely worthless.

The madness in one example: Procter & Gamble launched a Charmin toilet paper NFT. This was sold for over $4,000. All proceeds were donated, but a symbol of the madness of 2021.

From a portfolio perspective, 2021 was great! In the end, there was a +32% return and a portfolio value of over €190,000, which at times in November 2021 was €199,000.

My top performers were NVIDIA

$NVDA (+2,27%) with over 100% price gains and Pfizer $PFE (+0,18%)

, which was driven by the vaccine hype and at €50 was twice as high as in 2024.

My worst performer was another 80% loss with TAL Education $TAL (+0%) . An education company from China. Unfortunately, this was the first time I was able to experience the political arbitrariness in countries like China. Overnight, it was decided that education/tutoring could only be run as a non-profit. Of course, this was almost a death sentence for the company and the share price plummeted by 80%.

Asset development & return:

After the years 2013 to 2018 were forgettable in terms of returns, the years 2019 to 2021 finally delivered:

Year

Deposit value

Yield

2019 67.000€ +19%

2020 121.000€ +5%

2021 193.000€ +34%

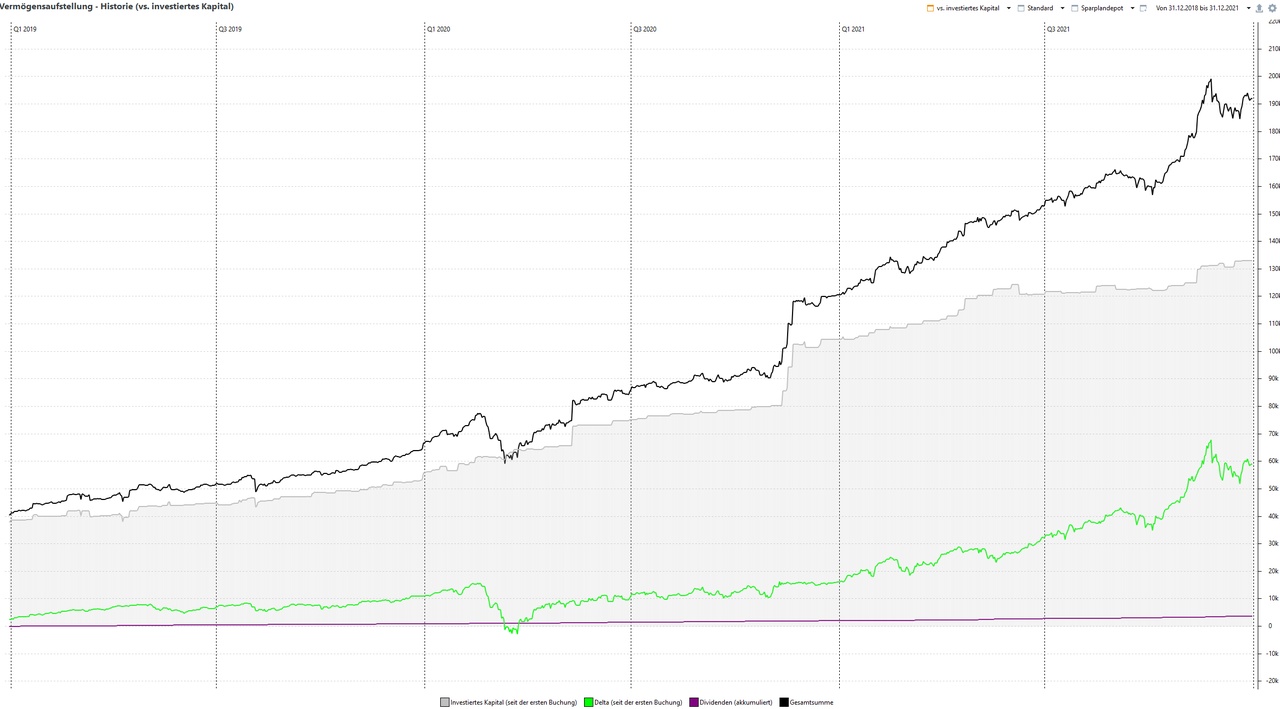

Vermögensentwicklung 2019-2021:

Vermögensentwicklung 2013-2021:

Outlook:

Looking back on the hype year 2021, it is almost obvious that 2022 had to be clearly negative.

After the party, however, came the hangover in the form of inflation and the war in Ukraine. Sharply rising interest rates and global economic concerns did the rest.

In the next part, I would therefore like to look at the years 2022 & 2023. I will then combine 2024 with my review of the year in the last part.

53Posições

€ 292.803,30

70,11%

10Mês·

From 18-year-old wannabe investment banker to successful private asset manager: my (bumpy) path to €300,000 in my custody account

Part 2 of X:

After a long road through the valley of tears: how buying MasterCard shares ended up

changed everything - This is probably the best way to describe the next stage of my investing life. After discussing my first steps on the stock market in the first part and realizing that I'm not the next Warren Buffett and that I've made just about every rookie mistake, after three years everything should finally be getting better, right? Unfortunately, that wasn't the case in 2017 and 2018. In fact, everything only got worse.

(Part 1: https://app.getquin.com/de/activity/PElWrODsmV) - Thank you for all the positive feedback!

Baseline & Spoilers:

From 2013 to 2016, I did a dual study program and earned a small salary every month. As I was still living at home, I was able to save and invest around €30,000 during these three years. I also added around € 5,000 in capital gains and dividends. My portfolio balance at the end of 2016 was therefore around €35,000. Despite my poor stock selection, this was a sum I could be happy with as a 23-year-old.

Now let's jump forward 24 months: at the end of 2018, I had a portfolio balance of around €40,000, just a measly €6,000 more than two years earlier. In these two years, there were additional price losses of €3,500. In other words, I had managed to lose €600 on the stock market in 5.5 years, while the S&P 500 gained over 50% in the same period - a remarkable (negative) achievement! Only dividends of over € 3,000 in these 5.5 years led to a positive return on the bottom line.

But now let's take a look at what went so massively wrong in 2017 and 2018.

Personal income situation:

After I completed my Bachelor's degree at the end of 2016, I knew that I didn't want to stay with my training company. There was a strong focus on sales, which I personally never wanted to do. I therefore left the company and decided to make a new career start in my early or almost mid-20s.

Before my studies, I really wanted to go into investment banking in New York, but after my studies I suddenly didn't know what I actually wanted to do: "self-employed would be cool", "do I do another Master's", "do I study something completely different again?" - these were my thoughts at the end of 2016 and beginning of 2017. As I was registered as unemployed during this time, I had to keep going to job interviews, which were more or less forced on me by the job center. These were mandatory, as otherwise the money could have been cut (times before the citizen's allowance 😉). My highlight was a job interview at Vorwerk, and I'm not kidding: for an open position as a vacuum cleaner salesmanwho is allowed to move from door to door.

In mid-2017, I was then offered a job in a completely different area that had absolutely nothing to do with my bachelor's degree in business administration and started all over again. I received around €600-700 in unemployment benefit for 9 months and then only a trainee salary of €800-900. Fortunately, I was able to continue living with my parents and invest around €200-300 in ETF savings plans every month. However, I was only able to save around €2,000 in total in 2017.

A few weeks went by and I quickly realized that I was once again not happy with my new professional situation. So I knew I had to leave again. This time, however, I didn't want to just quit and turn up at the job center again. So I forced myself to keep going until I had something in hand. The subject of a Master's degree came up again. But it was also by chance that I got in touch with my former employer.

Long story short: At the beginning of 2018, after 1.5 years, I signed a new contract with my former employer (DAX company), albeit not in a sales role, but in head office/administration. Even though the salary increased significantly, this involved moving to another city. In addition to the rental costs, I also had to furnish an apartment. As a result, there was not much room for investment in the stock market in 2018 either. In total, "only" €5,000 was invested in 2018.

Portfolio performance:

As already mentioned, 2017 and 2018 were an absolute flop in the portfolio. No significant investments and a lousy performance.

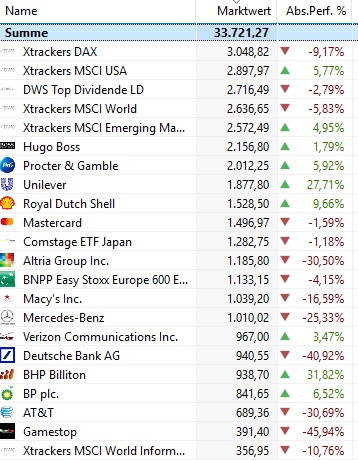

In hindsight, it's no wonder: at the time, my portfolio consisted of price rockets such as Hugo Boss $BOSS (-0,02%)

Deutsche Bank $DBK (+0,66%)

Macy's $M (+0,77%)

AT&T $T (+1,78%)

Verizon $VZ (+0,48%)

or Daimler $MBG (+0,6%) .

I was still convinced that tech and co. were far too expensive - I only bought what had a low P/E ratio and a (high) dividend yield. From a dividend perspective, that was great: in 2017, I received over €1,000 in dividends for the first time. I won't reach this mark again until 2020.

However, it also became clear to me that dividends are of little use if there are share price losses on the other side. On average over the two years, my return was a meagre ~2.5%. That was still more than was available on the call money account at the time - today such a return would hurt even more. But you don't have to sugarcoat it either: The performance was forgettable.

Bright spots:

But it wasn't all bad either: I took my first steps into crypto in the fall of 2017. Back then, there was a lot of Bitcoin hype for the first time. I had no idea about it yet, so I bought a participation certificate via the stock exchange as normal. I made a profit of almost €500 in just under three weeks. After that, the hype quickly died down again and I didn't get involved with Bitcoin and co. until the next hype in mid or late 2020.

If I had continued at the end of 2017 and bought Bitcoin regularly, my wealth would probably be a lot bigger today.

All in all, I can look back on the year

2017 but I can also defend myself a little bit: The performance in 2017 was around +7%, which was roughly in line with the performance of the MSCI World (+8%). Only the S&P 500 was significantly stronger at +20% (Trump and his "America First" policy have already had an impact here).

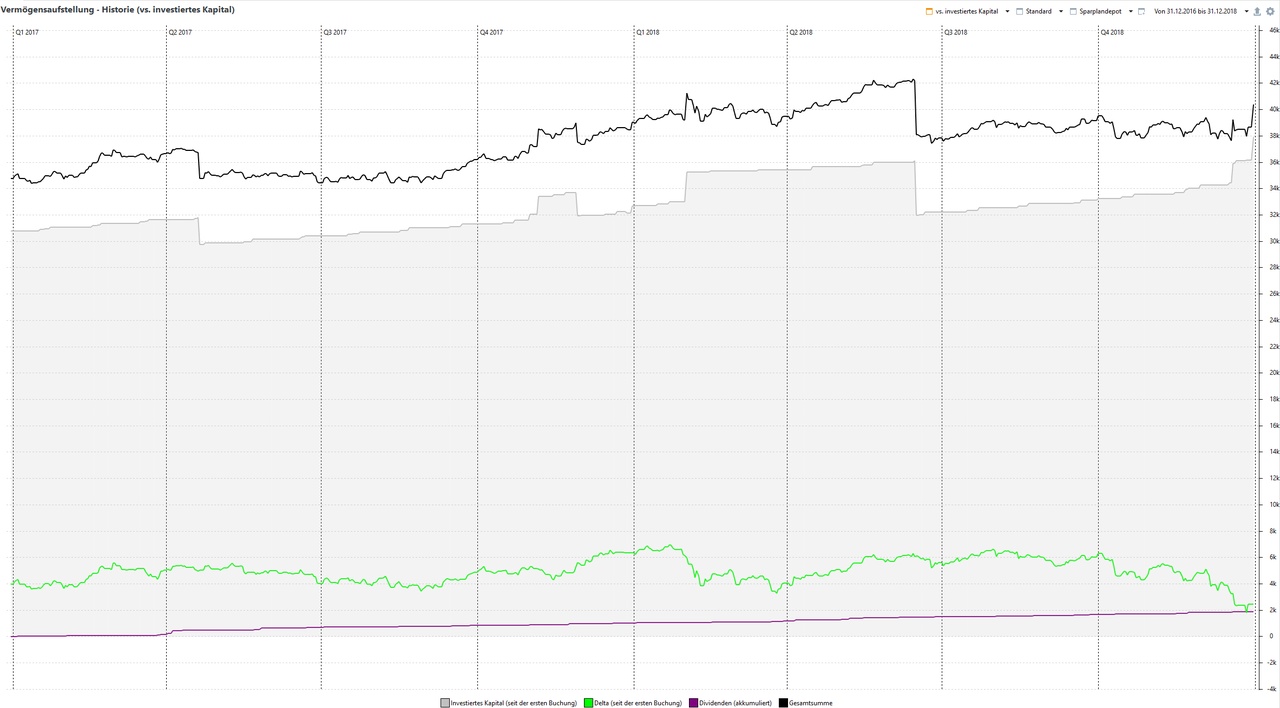

The year 2018 was not a good year on the stock markets overall, and most indices closed in the red. Nevertheless, my decline was greater than that of the S&P 500 and the MSCI World.

There were a number of negative factors in 2018, such as risks from the trade war between China and the USA, Brexit and global economic concerns. All of this was reflected in share prices, particularly in the final trading days of 2018. Once again, a shutdown was on the cards in the US because no agreement could or would be reached on raising the debt ceiling. Within a few days from mid-December, prices fell by 5-6%. This was the main factor behind the extremely poor performance over the two years.

The turning point:

Even though December 2018 was a bad month for the stock markets, in hindsight it was extremely good for me and my portfolio. In December 2018, I bought MasterCard $MA (-0,09%) and that was the turning point in my investing career.

I realized that my strategy (low P/E ratio, high dividend) would lead to nothing and discovered more and more the topic of "dividend growth" for me. MasterCard was the first stock to enter my portfolio that was in line with my new strategy.

Instead of a low P/E ratio of less than 10, the P/E ratio was suddenly over 30 and the dividend well below 1%, but growing strongly - just like sales and profits. A clear difference to companies like Macy's, Daimler and Hugo Boss in my portfolio.

My financial situation also improved significantly over the course of 2018. My net salary was around €2,500, and even though I had to pay rent and other costs, it became clear that I would be able to invest more again from 2019.

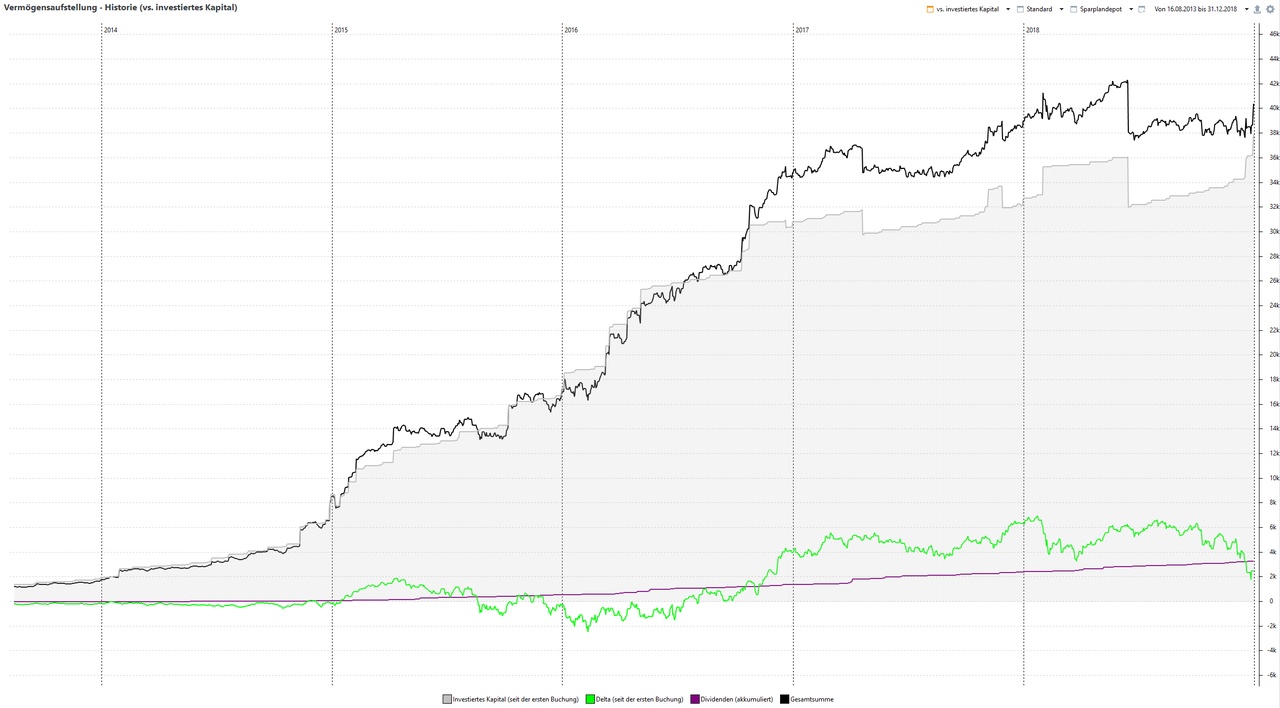

Asset development & return:

As described, the two years were too forgettable - but the learnings and my strategy change in hindsight extremely important for my future investing life.

Year

Deposit value

Return

2017 39.000€ +7%

2018 41.000€ -10%

Vermögensentwicklung 2016-2018:

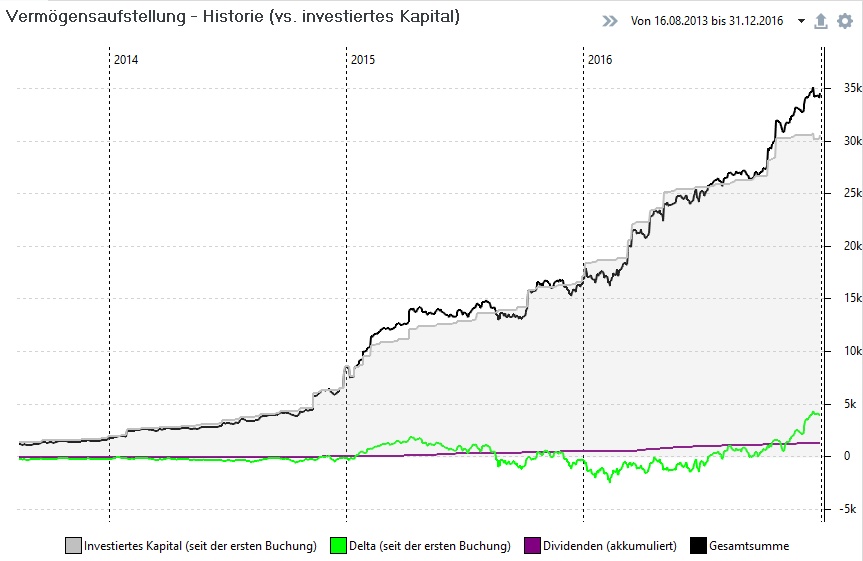

Vermögensentwicklung 2013-2018:

Outlook:

I had arrived professionally and was ready to build up a completely new strategy in my portfolio. Everything was ready for 2019! And everything should finally get better in 2019. But there will be more big mistakes in the next part (Wirecard, corona hype, China), but above all there will finally be successes!

In part 3, I will discuss the years 2019 to 2021. We will then break the €100,000 mark and even come close to reaching €200,000.

6666

22 Comentários

I'm glad you're sharing your thoughts and your career with us. I'm already looking forward to the next part 🤛

•

22

•10Mês·

From 18-year-old wannabe investment banker to successful private asset manager: my (bumpy) path to €300,000 in a custody account

Part 1 of X (let's see how many there will be): The new Gordon Gekko? Between Chinese small-cap recommendations from stock market letters and "AT&T is better than Amazon" (2010 - 2016)

(Part 2: https://app.getquin.com/de/activity/LUkWiLtZKX)

Previous story:

Inspired by @DonkeyInvestor I would now like to share my story and continue it if there is interest. Thanks for the cool idea!

My investment journey began about 2-3 years before my first securities purchase in 2013. While the financial crisis (2007-2009) only interested me marginally as a ~15-year-old, the emerging euro crisis from 2010 onwards aroused a much greater interest in the economy, sovereign debt and co. As part of some school work, I dealt with the debt crisis in Greece, among other things.

Through films like Wall Street or Margin Call - The Great Crash slowly sparked my interest in the stock market. With my first smartphone in 2012, I was able to secretly check share prices during lessons - which often led to the teacher confiscating it 😂 I primarily followed the prices of "cool" shares such as Daimler, Hugo Boss and Sony.

I grew a desire to become an investment banker myself and emigrate to Wall Street in New York (spoiler: neither happened 😉).

The first purchases:

My first purchases were made under contradictory circumstances. I was firmly convinced that a major crash was imminent (government debt, interest rate policy, ...) and was very convinced by well-known crash prophets such as Dirk Müller.

Nevertheless, I wanted to play along and bought my first shares.

In 2013, I started my dual business studies at a global bank. When I started my studies, I finally made my first securities purchases. On the one hand, my capital-forming benefits went into the DWS Top Dividende, and on the other, I set up an ETF savings plan on the DAX. In 2014, I added further shares such as AT&T $T (+1,78%) Verizon $VZ (+0,48%) Shell $SHEL (+0,1%) and Sony $6758 (-0,82%) were added. While Sony was a great investment, I unfortunately sold the stock far too early. My purchase price was around €12 and I sold at around €18. If I hadn't sold Sony, it would have been a tenbagger at times.

My main investment criteria at the time were

- Low P/E ratio

- High dividend yield

- And/or "cool" company

So in 2014 I had to choose between Amazon $AMZN (+1,75%) ("cool, but no dividend & much too high P/E ratio") and AT&T ("high dividend, low P/E ratio"). And, of course, the decision sucked with today's knowledge.

Another company was Macy's $M (+0,77%) . When I was in New York and visited the largest shopping center in the world, I was sure I had to have this stock.

The only two stocks I still have in my portfolio from my early years are Procter & Gamble $PG (-0,26%) (bought in 2015) and Unilever $ULVR (-0,19%) (bought in 2016).

In 2016, I had a total of 14 individual shares in my portfolio, 12 of which were sold in the following years and will probably never end up in my portfolio again.

The first lesson:

After I realized professionally that the path to investment banking and New York was probably not the right one after all (40 hours of work is really exhausting, I don't need 80 or more in investment banking), I slowly realized that I wasn't the next Gordon Gekko or Warren Buffett either.

It was too boring for me to just invest in shares - after all, I wanted to get rich quick and drive a Porsche! So from 2014, I also started investing in other things (no, unfortunately not crypto).

I tried my hand at various certificates, reverse convertibles and the like, all with little success. The biggest learning I had was with an absolutely hot tip from the internet. It was a classic pump and dump game from a stock market letter. Someone had stocked up on shares in a Chinese small cap (Tianbao Holdings) and then called on everyone to buy: "Share with the chance of a 10,000% return - forget Apple and co." It was advertised like this or something similar at the time.

I took my entire monthly salary (around €800) and thought to myself: get in! It didn't matter what the company was doing or why the opportunity should be so great! At first things went up and I was quickly up 20%. Then it went downhill - the initial investor had probably made his return and withdrawn the money. The stock exchanges quickly realized this and stopped trading. I tried to sell the shares on various stock exchanges and was able to get rid of them in Berlin, Bremen or somewhere else - with a loss of 50%. Two weeks of work for nothing. Although it was "only" a loss of €400, it really annoyed me. Not just the loss, but that I fell for something like that.

In hindsight, the €400 was extremely well invested and helped me a lot in my future investment career.

Asset development & return:

How did the first 3-4 years on the stock market go and how did my assets develop?

Year Deposit value Return

2013 2.000€ -12%

2014 8.600€ -1%

2015 17.000€ +4%

2016 35.000€ +14%

All in all, these were lost years for me in terms of returns. You can also see this from the green line, which was mostly in negative territory.

The stock markets did very well, and yet I mostly only saw losses or very low returns.

Conclusion & outlook:

So in 2016 it was clear to me: no investment banking, no New York, I'm not the new Warren Buffett and I'm not going to get rich overnight.

In the following 3 years from 2016 to 2019, I built on my initial experiences and slowly developed into a better investor. Nevertheless, more big mistakes followed (Bitcoin, Wirecard, ...).

201201

30 Comentários

10Mês

When is part 2 coming? 👍🏼

•

3636

•

10Mês·

You have to give it a try:

Macy's $M (+0,77%) has launched an investigation after it became known that a former employee allegedly concealed financial information, which led to accounting errors. In total, he has reported expenses of more than 132 million dollars were concealed (!). This incident caused additional operational costs and contributed to the delay in full quarterly reporting. The company emphasizes that it is taking measures to improve internal control mechanisms and ensure transparency for investors.

Personal opinion:

Wtf!

You can find more information in the article on the Financial Times.

The news is based on what I personally consider to be reputable sources. No investment advice. Follow me for more updates!

www.ft.comMacy’s says employee hid more than $132mn in delivery expenses

22

Títulos em alta

Principais criadores desta semana

Dados tempo real da LSX · Dados financeiros e EOD da FactSet