Good morning, my dears,

and today we continue with the new series.

" My intern Juan on a tenbagger search " 🎥

🔍 Juan is also allowed to let off steam on my watchlist this weekend. And guys, what can I tell you. He's learning more and more from me by:

- Looking in the growth sectors

- He proceeds according to the strategy "Putting the cart before the horse"

- He looks for niche champions and scoops

Juan is increasingly becoming a stock picker.

So I'm not at all surprised that he found a SpaceX scoop straight away. Because he sees potential here, spurred on by the SpaceX IPO. He is also operating in an absolute growth sector here. Juan hasn't missed the fact that the Americans are the target either

" The journey to Mars "

My dears, so as not to inflame your excitement to the extreme. Let's quickly move on to the company presentation which I developed together with Juan.

As always, I look forward to many comments. And Juan also needs some confirmation from you. This motivates him to continue searching for you.

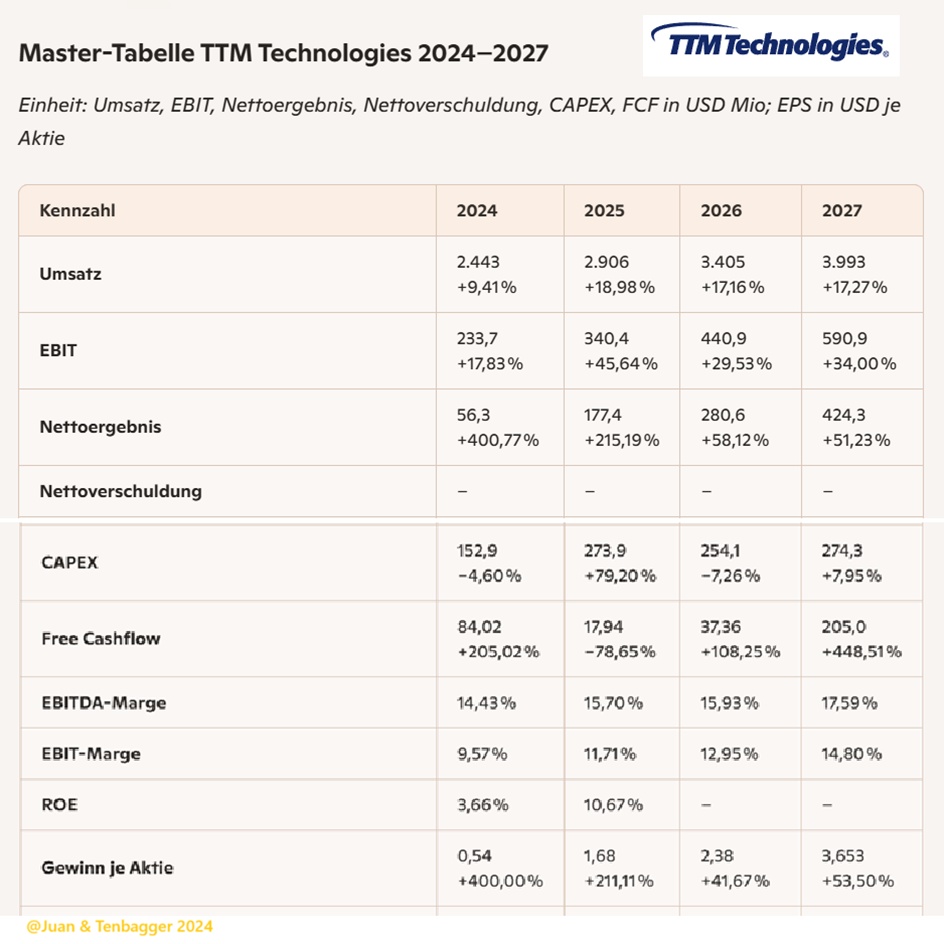

$FTC (-0,71%)

🛰️ Why Filtronic is considered a SpaceX scoop

1) Filtronic provides mmWave and RF technology for space and satellite communications

This clearly shows that Filtronic is actively involved in the space industry industry:

- "Space" is a core sector in its own right

- Products such as E-Band SSPA, Hercules II, Morpheus II are built for satellite backhaul and ground stations

These are exactly the components that LEO constellations like Starlink need.

Filtronic builds components that are indispensable for LEO constellations

SpaceX (Starlink), Amazon Kuiper, OneWeb, Telesat - they all need:

- High-performance mmWave amplifiers

- E-band transceivers

- Ka-band modules

- High-frequency filters

- TRMs (Transmit-Receive Modules)

Filtronic offers exactly these modules.

"Filtronic introduces an advanced high-bandwidth DIFI solution to enable fully virtualized satellite earth stations."

This is exactly the kind of infrastructure that Starlink & Co. need to scale.

🎯 Juan's conclusion for you

Filtronic is a classic "scoop manufacturer" in the space boom. Not the rocket, not the satellite - but the high-frequency technology, without which neither would work.

That's exactly the sweet spot for tenbagger smallcaps.

Filtronic plc develops and manufactures radio frequency (RF), microwave and millimeter wave (mmWave) technologies. The company's products transmit, receive and condition radio signals, particularly at microwave and mmWave frequencies. It develops and manufactures RF-to-mmWave components and subsystems for mission-critical communication networks. The company's products include Morpheus X2, Morpheus II, Hades, Cerus, tower top amplifiers, switched filter banks, GaN amplifiers, custom filters, custom combiners, interference mitigation filters, transmit and receive modules, transceivers, front-end modules, ceramic filters, combline filters, merged element filters, metal cavity filters, suspended substrate filters, thin film filters, small cell filters, waveguide diplexers, cross-band combiners and in-band combiners. The company's technologies are used in high-performance markets including aerospace and defense, telecommunications infrastructure, critical communications, space and other markets.

Number of employees: 186

Markets

Your products are at the forefront of radar and electronic warfare technology.

- Telecommunications infrastructure

They enable reliable, accurate voice and data communications for emergency services.

- Critical Communications

- Space

They offer high-performance transceiver modules that enable ground-to-space and inter-space data transmission.

Low latency private networks,

quantum computing,

Test & Measurement

From the track to the train

115190-FILTRONIC-ANNUAL-REPORT-2025_v6_LR-00E.pdf

History of innovation:

Company founded by Professor David Rhodes at the University of Leeds.

First employees recruited.

Filtronic components receive a Queens Award for technology. Wireless infrastructure business established.

Filtronic Comtek established to focus on 2G - global systems for (GSM)

Filtronic Comtek plc listed on the UK stock exchange.

Acquisition of the Fujitsu silicon plant in Newton Aycliffe for the manufacture of GaAs (gallium arsenide) wafers.

Triton chipset, transmit and receive multi-purpose MMICs, developed for mobile backhaul

The company reorganizes into three divisions: Wireless Infrastructure, Handset Products and Integrated Products

Development of mmWave capabilities, including Theseus, Orpheus and Morpheus II

Headquarters relocated to NETPark Science Park in Sedgefield, County Durham.

Company listing moves to the AIM stock market.

Company listing moves to the AIM stock market.

Launch of contract manufacturing services, primarily for aerospace and defense

Launched Morpheus II, market leading transceiver product and tower top amplifier range.

Awarded the Queen's Award for Enterprise: International Trade.

Launched Hades E-band active diplexer and extended range of Cerus high power amplifiers.

Morpheus X2, Taurus and Hades X2 launched

Awarded the King's Award for Enterprise: Innovation

ESA-funded project

DTEP funding

Leonardo - Supplier Innovation Award

Strategic partnership Partnership with Space X

Part of the ESA/Viasat D2D project

New contract wins in the year include

- LEONARDO

- VIASAT

- AIRBUS

- SpaceX

Operational highlights

Strong execution of growth strategy

- The move to a new, bespoke facility in Sedgefield is underway and due to be completed in the first half of FY2026, doubling the Group's UK manufacturing capacity to meet the growing demand for the Group's products

Expanding exposure to the space and aerospace and defense markets

- Record orders in the space sector, including a landmark agreement with SpaceXas well as new contract awards to Viasatthe European Space Agency and Airbus.

- Strengthening the position in the defense sector, demonstrated by the recently concluded contract for the airborne radar application with Leonardo and the progress made in the programs of QinetiQ and BAE Maritime Systems.

Continuous innovation to support scaling

- Extended development to higher frequency RF bands, in particular V-band, opened up new market opportunities and reached a major milestone with the successful launch of Prometheus, the highest power solid state power amplifier on the market.

- Accelerated transition from gallium arsenide (GaAs) to gallium nitride (GaN) technology, enabling higher performance for satellite and defense systems, with the launch of the GaN-based product line in 2026.

NEWS

Filtronic stellt eine fortschrittliche Hochbandbreiten-DIFI-Lösung vor, um vollständig virtualisierte Satellitenbodenstationen zu ermöglichen – Filtronic

Filtronic eröffnet neue Haupt- und Produktionsstätte – Filtronic

Filtronic sichert sich eine Schlüsselrolle im europäischen Verteidigungssektorprogramm – Filtronic

Filtronic vergab NSIP Mittel zur Entwicklung der nächsten Generation des 550W Ka-Band SSPA - Filtronic

Filtronic, a leading Entwickler und Hersteller fortschrittlicher RF- und Mikrowellenlösungenwas funded by the National Space Innovation Program (NSIP) of the britischen Weltraumagentur (NSIP) to develop a high-performance 550W Ka-band solid-state power amplifier (SSPA). The project will advance Filtronic's proprietary gallium nitride (GaN) technology and integrated system design, setting new standards in efficiency, linearity and reliability for satellite communications.

Filtronic schließt mehrjähriges GaN-Verpackungsprojekt ab – Filtronic

Filtronic sichert den Auftrag für Satellitennutzlast-Baugruppen – Filtronic

Filtronic sichert sich rekordverdächtige SpaceX-Bestellung – Filtronic

Filtronic verdoppelt innerhalb eines Jahres seine Ingenieurbelegschaft, da die Expansion im Vereinigten Königreich sich beschleunigt – Filtronic

Geographical distribution of sales

(GBP 2025)

Americas 51.16 million

United Kingdom 3.95 million

Europe 1.2 million

Rest of the world 4.0 million

📌 Brief analysis of the key financial figures (2025-2028)

from the perspective of an investor who pays attention to growth, margin quality and cash flow

1) Growth: extremely strong, but volatile

Filtronic shows an explosive sales growth:

- 2025: +121 %

- 2026: slight decline (-1.6 %)

- 2027: +13 %

- 2028: +20 %

The pattern is typical for a deep-tech supplier: large project cycles → strong leaps → short breaks → next growth wave.

Investor takeaway: → Filtronic is growing structurally, but not linearly. Attractive for long-term investors.

2) Margins: Peak in 2025, normalization thereafter

The margins show a clear picture:

- EBITDA margin 2025: 30% (extremely strong)

- 2026: 18,9 % (normalization)

- 2027-2028: 20-21 % (stable profitability)

Investor takeaway: → 2025 is an exceptional year. → From 2027 onwards, Filtronic stabilizes at solid 20% EBITDA margins - very good for an RF/mmWave specialist.

3) Profitability: fluctuating, but structurally positive

Net result:

- 2025: GBP 14.05 million (peak)

- 2026: GBP 3.1 million (slump)

- 2027: GBP 6.85 million (recovery)

- 2028: no estimate

Investor takeaway: → Profits fluctuate strongly, but remain positive. → The business model is profitable, but project-driven.

4) Cash flow: Surprisingly strong

Free cash flow:

- 2025: GBP 8.22 million

- 2026: GBP -0.65 million

- 2027: GBP 5.87 million

- 2028: GBP 8 million

Investor takeaway: → Filtronic generates regularly positive FCFexcept during investment peaks. → This is a quality feature for small caps.

5) Balance sheet: very strong - net cash position

Net debt:

- 2025: GBP -10.8 million

- 2026: GBP -10.1 million

- 2027: GBP -12 million

- 2028: GBP -25 million

Investor takeaway: → Filtronic is debt-free and further expands its cash buffer. → This massively reduces risk.

6) Capital intensity: fluctuating but controlled

CAPEX:

- 2025: GBP 5.62 million

- 2026: GBP 9.67 million

- 2027: GBP 4.93 million

- 2028: GBP 5 million

Investor takeaway: → CAPEX peaks are project-related. → No structurally capital-intensive business model.

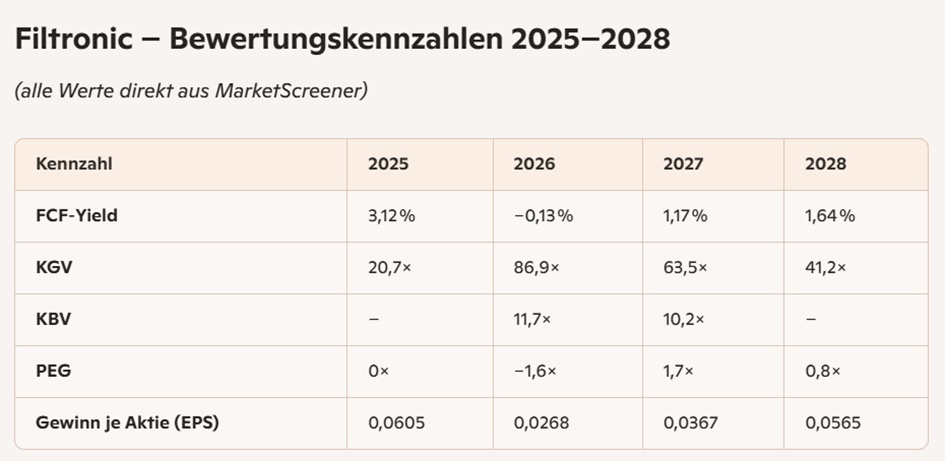

7) EPS: Strong growth over the cycle

Earnings per share:

- 2025: 0.0605 GBP

- 2026: 0.0268 GBP

- 2027: 0.0367 GBP

- 2028: 0.0565 GBP

Investor takeaway: → EPS grows over the entire cycle significantly. → 2026 is a downward outlier, but 2027-2028 show clear recovery.

🎯 Overall conclusion for you as an investor

Filtronic is a classic deep-tech small cap with:

- very strong structural growth

- High but fluctuating profitability

- excellent cash flow profile

- debt-free balance sheet

- clear technological competitive advantages (mmWave, defense, satellites)

investment character:

- Non-linearbut high quality

- High upsidewhen large orders come in

- Low insolvency risk due to net cash

- 2025-2028 show: Filtronic can scale

Market value 512.5

Number of shares (in thousands) 219,943

Date of publication 29.07.2025

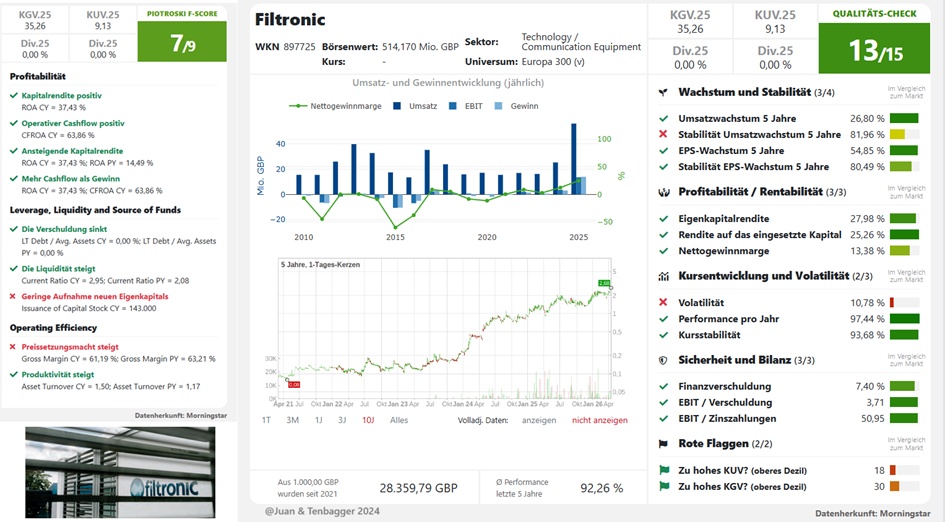

📌 Valuation analysis Filtronic (based on MarketScreener)

(P/E ratio, P/B ratio, PEG, FCF yield, EPS -

1) P/E ratio - expensive in the cycle, but falling sharply towards 2028

MarketScreener shows an extreme volatility:

- 2025: 20,7×

- 2026: 86,9×

- 2027: 63,5×

- 2028: 41,2×

Interpretation: → 2026 is an outlier year with low earnings → P/E ratio shoots up. → From 2027/2028, the valuation normalizes again significantly → 2028 P/E ratio 41× is not atypical for a deep-tech small cap.

Investor takeaway: → Filtronic is not a value playbut a growth tech play with cyclical profits.

Investor takeaway: → The 2028 PEG is the strongest bullish signal in the valuation.

🎯 Overall valuation (MarketScreener-based)

Value:

❌ No value case → High P/E ratios, high P/B ratios, cyclical earnings.

Growth:

🟩 Strong → Sales + margins + EPS structurally rising again from 2027.

Quality:

🟨 Medium to high → Net cash, positive FCF, technological momentum, but volatile profits.

💡 Juan's investor conclusion

Filtronic is a deep tech small capthat:

- looks expensive in terms of valuation,

- but 2028 clearly more attractive (PEG < 1),

- cash flow positive remains positive,

- and a real technology moat (mmWave, defense, satellites).

For investors: → Not a classic value stock, → but an asymmetrical growth tech case with high upside if the order situation continues in 2027/2028.

🔍 Why Filtronic has tenbagger potential in the first place

1) Market position

Filtronic is one of the few suppliers worldwide for high-frequency mmWave modules in the defense/satellite sector.

2) Scalable technology

When a large customer scales (e.g. LEO constellation, defense program), Filtronic scales scales disproportionately.

3) Valuation provides leverage

PEG 2028 = 0,8 → Market is pricing in growth not fully priced in.

4) Net cash balance sheet

→ Very low insolvency risk → High flexibility for capex & R&D

🧠 Juan's clear conclusion

Filtronic is not a safe tenbaggerbut an asymmetric high upside small cap:

- Moat extremely strong

- Structural growth

- Valuation attractive from 2028

- High risk, but controlled

➡️ 20-30% tenbagger probability is exceptionally good.

Performance

1 week +16.50 %

1 month + 24.60 %

6 months + 79.23 %

1 year +137.76 %

3 years +1,841.67 %

5 years +2,812.50 %

7 years +2,906.45 %

SHARE PRICE € 2.68 19.04.2026

$FTC (-0,71%)