Hello my dears,

As announced yesterday, the series continues today.

After the last company presentation of Filtronic $FTC (-0,71%) the dear Prompt Jack ( @Aktienhauptmeister ) took another look at the company.

I realized that Juan still has some weaknesses, which Jack fortunately pointed out to us without embellishment.

Juan recognized the potential in the sector and also had SpaceX's IPO in mind. But in his euphoria, he neglected important criteria.

- He overlooked the fact that a great deal of SpaceX fantasy is already priced into the share price

That's why I explained to Juan once again in a personal one-on-one meeting. Despite the euphoria and Tenbagger fantasy, the valuation should not be neglected. After all, in the end this contributes to a large extent to achieving a Tenbagger at all.

Guys, and what can I tell you, motivated by the conversation, Juan set off on another search.

And he found a competitor of Filtronic in the USA.

Again, I look forward to a ruthless review from Jack ( @Aktienhauptmeister ), and from the community.

TTM Technologies $TTMI (-2,2%)

66% plus in the data center segment makes PCB specialist an indispensable AI profiteer!

13.04.2026

AI growth driver: massive demand for specialized PCBs for data centers ensures forecast segment growth of 66 Strong guidance for 2026: The company forecasts double-digit revenue growth driven by massive demand for AI infrastructure and modernization in the defense sector. Strong order backlog: A record backlog of USD 1.61 billion in the aerospace and defense sector offers long-term planning security.

The double lever: How TTM Technologies is benefiting from the defense boom and AI craze.

15.04.2026

There's still room after the rally.

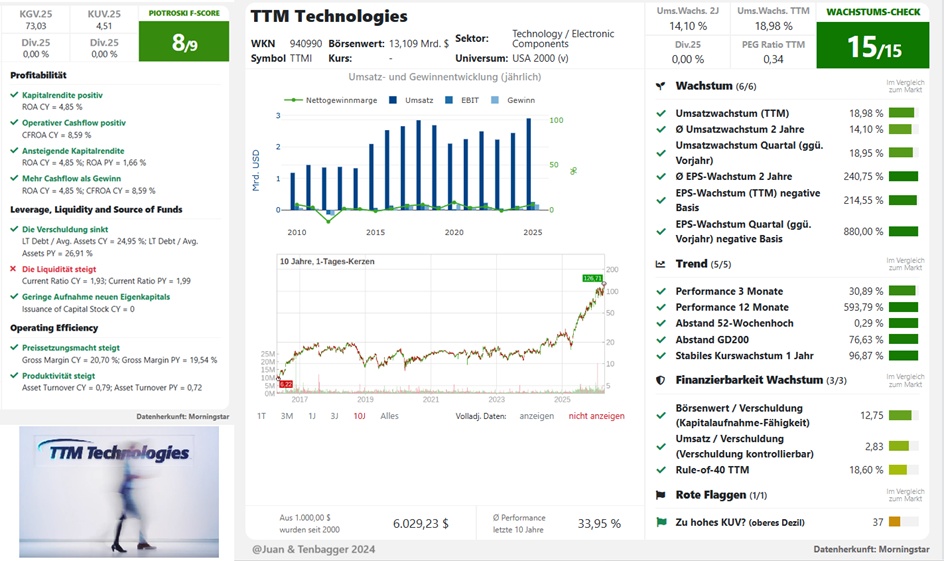

The market capitalization of TTM Technologies (TTMI) has now climbed to over USD 10 billion. The price-earnings-to-growth ratio (PEG) is 1.1, despite the 400% performance rally in the last twelve months.

Important components for radars, missile control systems and satellite communication

The company acts as the nervous system of modern defense and space systems. The company is not a manufacturer of tanks or missile hulls, but produces the highly complex printed circuit boards (PCBs), radio frequency (RF) assemblies and microwave subsystems that are essential for radars, missile guidance systems (e.g. Javelin) and satellite communications. The strategic role is also evolving: TTM is moving up the value chain by no longer just supplying the bare circuit board, but building complete, integrated sub and mission systems. This is lucrative, as complex assemblies achieve significantly higher margins than basic PCBs. In the space sector, TTM is benefiting from the development of radiation-hardened components that are needed for thousands of new LEO (Low Earth Orbit) satellites.

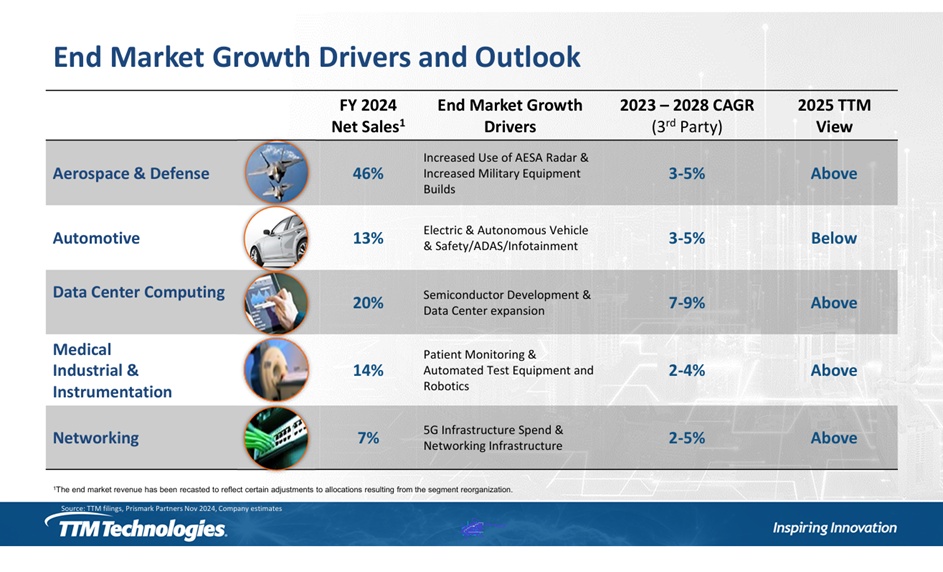

Aerospace & Defense accounts for around 40% of sales - Data Center business is also booming

41% of sales come from the Aerospace & Defense sector. At the same time, the data center business (AI) is booming. Together, these two drivers account for 80% of business. TTM is benefiting from the fact that military systems increasingly require AI capabilities ("Edge AI"), which is driving demand for extremely powerful PCBs in the defense sector. The new plant in Syracuse (New York), which is expected to generate revenue in the second half of 2026, and the huge plant acquired from TDK in Eau Claire (Wisconsin), will massively increase US production capacity for strategic customers.

Almost 20% sales growth

TTM delivered a strong 4th quarter and beat its own forecasts. Sales increased by 19%. The new plant in Penang (Malaysia) is not yet operating within the target corridor. It weighed on the gross margin in Q4 with 180 basis points, which was worse than the previously forecast 160 basis points. Management vows improvement, but this remains an operational construction site. The operating margin is improving and management issued very bullish medium-term growth targets (doubling profit by 2027). Bookings for surveillance radars, air defense systems (LTAMDS) and missile systems (MRAM, Javelin) were particularly highlighted. Management emphasized the growth in so-called "restricted programs" (secret military projects).

Conclusion

The ambitious targets (doubling profits by 2027) are attractive, but operational implementation is not a sure-fire success. The valuation with a P/E ratio26e of 33 is still ok, as EPS is expected to increase by another 40% in the coming year. The share could break out again and be picked up.

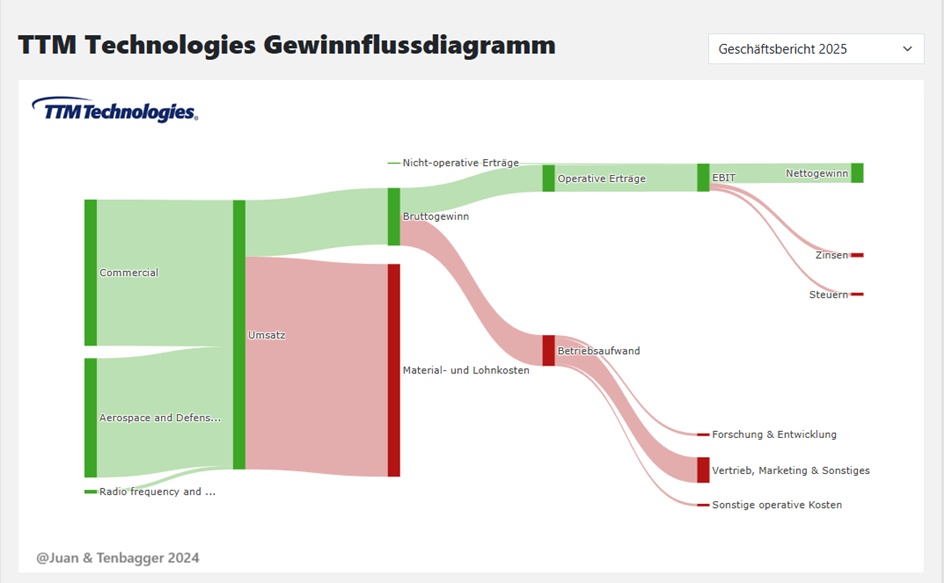

TTM Technologies, Inc. is a global manufacturer of technology solutions, including mission systems, radio frequency (RF) components and RF microwave/microelectronics assemblies, as well as quick-turn and technologically advanced printed circuit boards (PCBs). The company's segments include PCB and RF and Specialty Components (RF&S Components). The PCB segment consists of approximately 16 domestic system, subsystem and PCB factories, four PCB factories in China, one in Malaysia and one in Canada. The RF&S Components segment consists of one domestic plant for RF components and one plant for RF components in China. Both segments operate predominantly in the same industries, producing customized products for their customers and using similar distribution channels. The company offers a range of engineered systems, RF and microwave assemblies, HDI (High Density Interconnect) PCBs, rigid-flex PCBs, customized assemblies and system integration, IC substrates and others.

Number of employees: 18,200

TTM Technologies offers advanced technology products for a variety of innovative applications

- Aerospace & Defense

- Automotive

- Commercial Space

- Data Center Computing

- 5G / 6G

- Industry and instrumentation

- Medical Medicine

- Networks & Communication

INDUSTRY LEADER

- Top 10 of the world's leading PCB manufacturers

- 22 production sites worldwide

In the future

- Continued focus on markets with growth characteristics and favorable megatrends - Ongoing investment in differentiation:

- Advanced PCB technology for Generative AI

- Developed RF products for aerospace

- Manufacturing sites

- Sound financial management

- Plan in place to improve operating margins

- Strong focus on cash flow generation

- Capital allocation balances investment in the business with return of capital to shareholders

TTM Technologies, Inc. Investor Presentation - October 2025

Geographical distribution of sales

(USD 2025)

USA 1.55 billion

Other 1.1 bn

Taiwan 257 million

🔎 Brief analysis of the key financial figures (2024-2027)

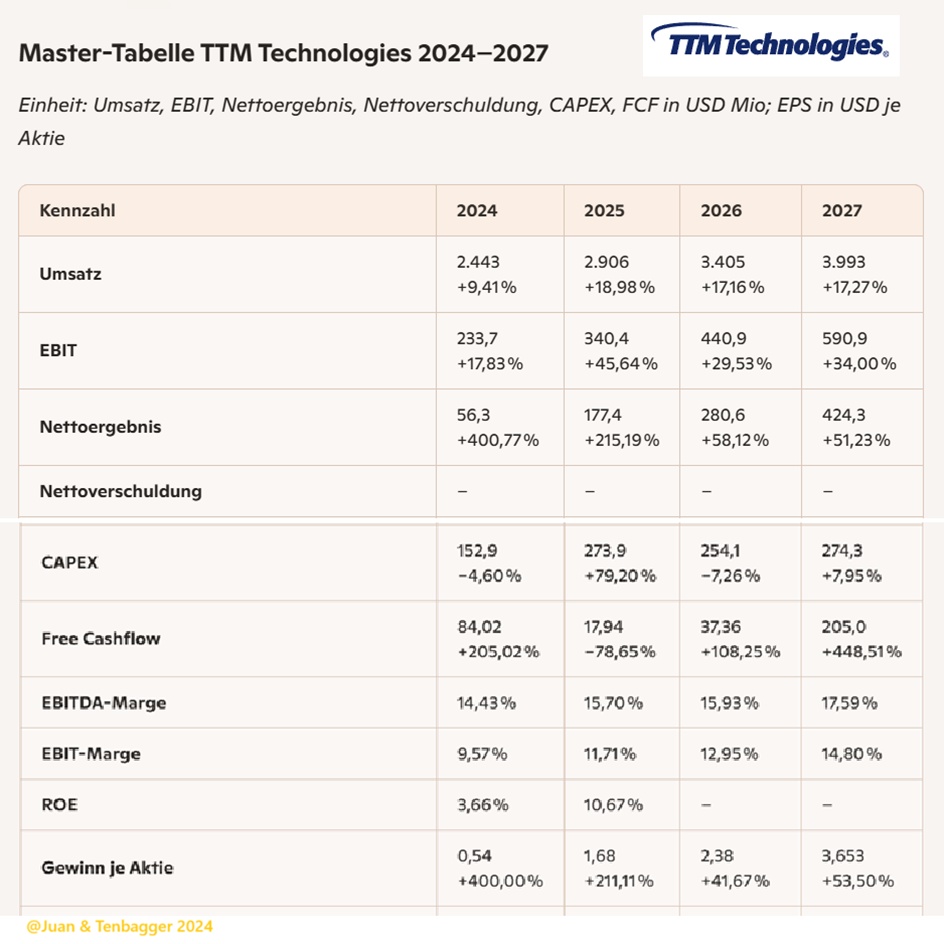

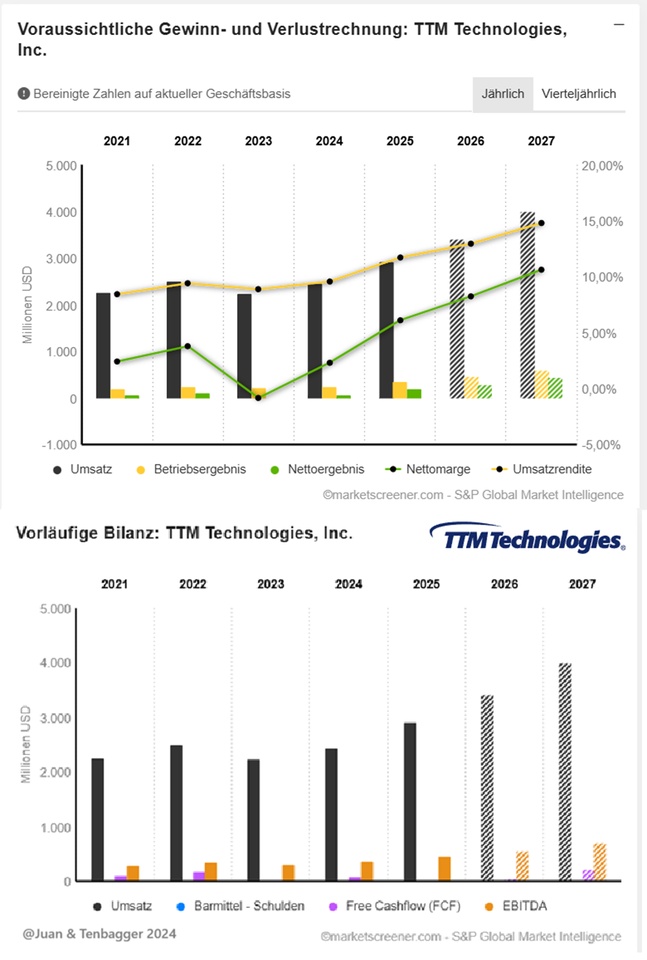

1) Strong, accelerated growth Turnover grows from 2.44 billion → USD 3.99 billion (+17-19% p.a.). This is exceptionally dynamic for a PCB/RF manufacturer and reflects structural demand (aerospace, defense, high-speed computing).

2) Margins are rising continuously EBIT margin improves from 9,6 % → 14,8 %. EBITDA margin increases from 14,4 % → 17,6 %. → This speaks for economies of scale, pricing power and mix improvement.

3) Earnings explode Net profit grows from 56 million → USD 424 million. EPS increases from 0.54 → 3.653 USD. → Massive operating leverage.

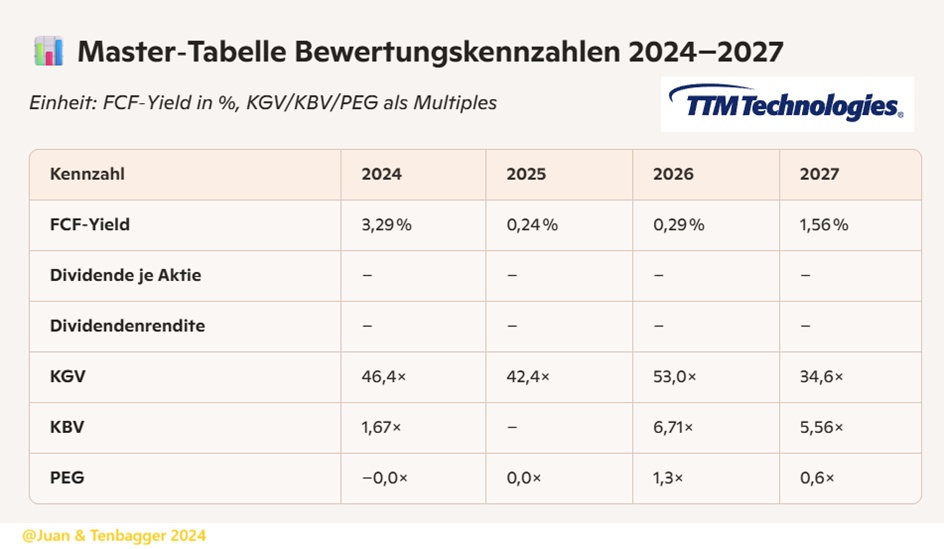

4) Free cash flow volatile, but very strong in 2027 2025 weak (high CAPEX), but 2027 with 205m USD an FCF breakout. → CAPEX cycles determine short-term FCF fluctuations.

5) ROE jumps up From 3,66 % (2024) to 10,67 % (2025). → Return on investment increases significantly, no estimates from 2026.

🧭 Summary for you as an investor

TTM shows a classic structural growth profile: rising sales, rising margins, rising profits - and an FCF peak in 2027. The company is scaling cleanly, which in combination with defense exposure and high-speed electronics creates a robust, cycle-resistant growth picture results.

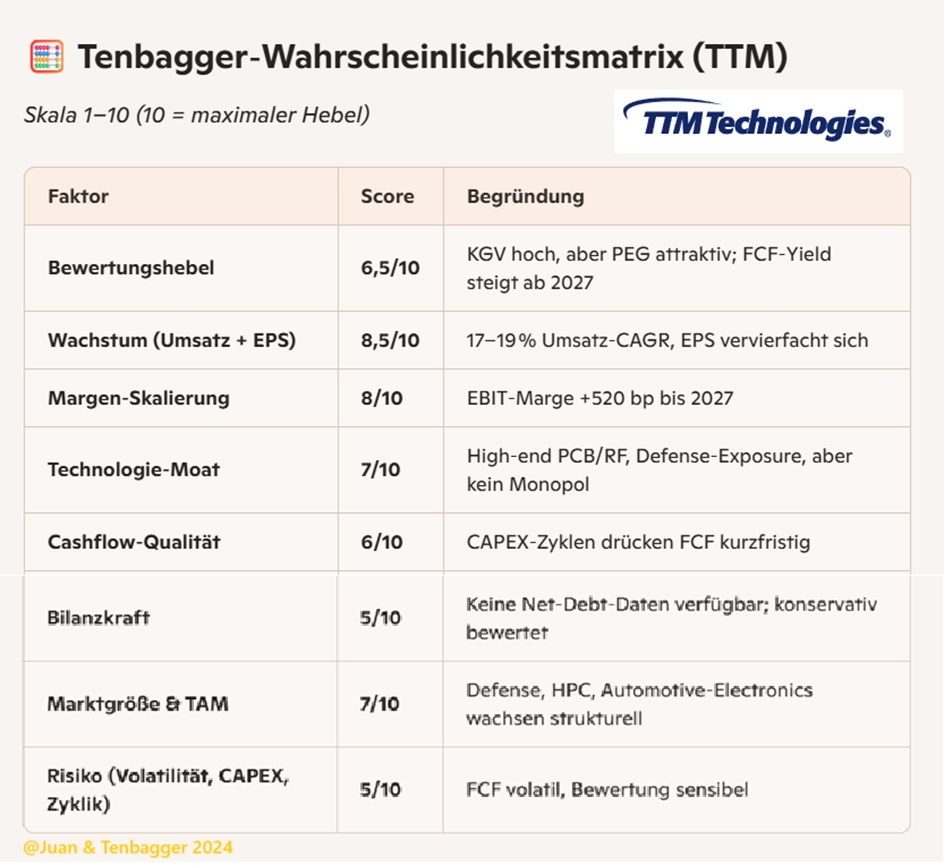

🧭 Ultra-short valuation conclusion

TTM is clearly a growth case, not a value case:

- P/E ratio highbut falling towards 2027 → Valuation eases.

- P/E 2027 = 0.6× → Strong ratio of growth to price.

- FCF yield 2027 = 1.56 % → still low, but trend rising strongly.

- No dividend → Complete focus on reinvestment & growth.

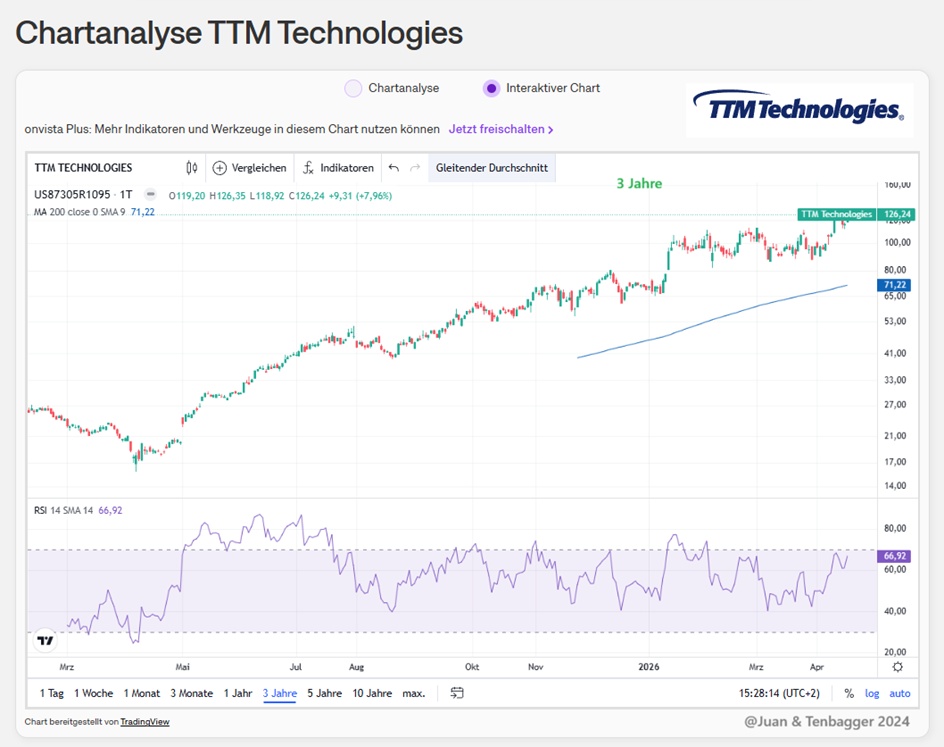

🚀 Tenbagger probability matrix - TTM Technologies (TTMI)

Based on the MarketScreener data from your active tab

📊 1st valuation basis (2024-2027)

- P/E RATIO: high, but falling → 46× → 34×

- PEG: 2027 at 0,6× → strong growth-to-price ratio

- FCF yield: 2025 weak, 2027 strongly increasing (1.56%)

- P/B RATIO: moderate (5-6×) → Valuation speaks for growth, not value.

📈 2. fundamental leverage (2024-2027)

- Turnover: 2.44 → USD 3.99 bn (+17-19% p.a.)

- EBIT margin: 9,6 % → 14,8 %

- EPS: 0.54 → 3.653 USD

- FCF: 2027 Breakout (USD 205 million) → Scaling + margin expansion + earnings leverage.

🛰️ 3. Strategic positioning

- Exposure to Aerospace, defense, high-speed computing

- PCB/RF high-end segment → structurally growing

- Strong order intake according to investor presentations → Cyclically robust + structurally growing.

🎯 Overall score: 6.9 / 10

→ Realistic tenbagger probability until 2032: 15-25 %

Why not higher?

- FCF yield still too low

- CAPEX cycles slow down in the short term

- Valuation already ambitious (growth premium)

Why still interesting?

- EPS leverage is extremely strong

- Margins increase every year

- Defense exposure provides stability

- PEG 2027 = 0.6× → Rare for a structural growth stock

Short conclusion for you

TTM is not a classic tenbagger moonshotbut a quality growth compounder with realistic 2-4× potential and a small but real chance to 10×, if:

- margins continue to rise

- FCF remains permanently high from 2027

- Defense/HPC cycles continue

Valuation does not expand too much

Performance

1 week +3.91 %

1 month +29.42 %

1 year +120.85 %

3 years +896.37 %

10 years +1,742.92 %

PRICE 108.23€ (21.04.2026 at 11:39)