- Mutares Holding's net profit for the financial year 2025 increased to EUR 130.4 million (previous year: EUR 108.3 million)

- Group revenue increases to EUR 6.5 billion (previous year: EUR 5.3 billion), EBITDA rises to EUR 675.3 million (previous year: EUR 117.1 million), adjusted EBITDA improves to EUR -31.2 million (previous year: EUR -85.4 million)

- The forecast predicts Group revenue of between EUR 7.9 billion and EUR 9.1 billion for the financial year 2026 and a net profit of EUR 165 million to EUR 200 million for Mutares Holding

- Medium-term targets until 2030: growth of at least 25% per year in Group revenue and net profit at Mutares Holding

- Capital increase successfully completed, especially for further expansion - strong growth expected in the USA and Asia

Munich, April 28, 2026 - Mutares SE & Co. KGaA $MUX (+0,09 %) (ISIN: DE000A2NB650) ("Mutares", "Mutares Holding" or "Company" and together with its subsidiaries "Mutares Group") today presented its annual report for the financial year 2025, including the consolidated financial statements as well as the combined management and group reports, which were published together with an unqualified auditor's opinion. Despite ongoing economic and geopolitical uncertainties, the company is optimistic about the future given its accelerated international expansion.

Mutares Holding's net profit increased to EUR 130.4 million

The revenue of Mutares Holdingwhich comes from advisory services of affiliated companies and management fees, reached EUR 106.2 million in the financial year 2025 (previous year: EUR 109.8 million). Mutares Holding's net profit under commercial law amounted to EUR 130.4 million in the financial year 2025 (previous year: EUR 108.3 million). The increase in profit was significantly influenced by the increased exit activity in the reporting period, with the complete sale of Steyr Motors being the outstanding transaction that had a decisive impact on profits in financial year 2025.

In the financial year 2025, the Mutares Group generated revenue of EUR 6.5 billion (previous year: EUR 5.3 billion). Consolidated EBITDA (earnings before interest, taxes, depreciation and amortization) in accordance with IFRS amounted to EUR 675.3 million (previous year: EUR 117.1 million), influenced among other things by gains from a bargain purchase and the positive contributions from disposals in the financial year. Adjusted EBITDA, which is specifically adjusted for the effects of regular changes in the portfolio composition, improved to EUR -31.2 million (previous year: EUR -85.4 million). Adjusted EBITDA was influenced in particular by the new acquisitions made in the financial year, especially Buderus, as well as by a persistently challenging environment at Lapeyre and Byldis. This was offset by extremely encouraging progress in restructuring and development at Efacec, Donges, SFC Solutions and Guascor Energy.

Significant expansion and internationalization of the portfolio

Mutares rapidly increased its portfolio in the reporting year. The focus was on scalable platform investments, targeted additional acquisitions and consistent internationalization - particularly in China and the USA. With the acquisitions in the 2025 financial year, Mutares acquired companies with combined annual revenues of around EUR 2.5 billion, thereby significantly expanding the Group's base.

An important highlight of the 2025 financial year was the acquisition of Magirus as a new platform in the business-critical specialty vehicles segment in the infrastructure and specialty industry segment. The globally established brand stands for technological excellence, a strong international market position and a robust end market profile. The strategic positioning was further strengthened by the add-on acquisition of Achleitner: the portfolio is being specifically expanded to include defence and security vehicles, which significantly increases the addressable market and creates additional synergies in sales and internationalization.

At the same time, international expansion was continuously accelerated. In China, Mutares strengthened its presence in one of the world's most dynamic automotive markets by acquiring a majority stake in HSR/HST for Amaneos as an add-on acquisition. In North America, expansion continued with the acquisition of TSM for the FerrAl United Group, and industrial expertise in the field of precision components was strategically expanded.

Overall, Mutares has thus significantly expanded its revenue base and further increased the diversification of its portfolio.

Increased exit activities underline value creation

Mutares impressively confirmed the effectiveness of its business model in the 2025 financial year with numerous exit transactions. The focus was on two outstanding capital market transactions: Steyr Motors and Terranor. The complete exit from the former company is a special milestone, as it represents the most successful investment in the company's history. Following the successful IPO of Steyr Motors in the 2024 financial year and a gradual reduction of the stake, Mutares sold its remaining 23% stake in full to institutional investors from Austria and abroad in a highly sought-after private placement in November 2025. During the entire holding period, Mutares generated gross proceeds of over EUR 170 million and a ROIC well above the target range.

Mutares also achieved significant value with Terranor. With the listing on the Nasdaq First North Growth Market in Stockholm in June 2025, Terranor was successfully positioned on the capital market. In a first step, Mutares sold 25% of its shares, followed by a further placement in December 2025, which reduced the stake to 57%. Both transactions met with strong demand from national and international investors and also led to a ROIC well above the target range.

With the sale of Fuentes shortly before the end of the year, Mutares once again demonstrated its ability to identify companies with solid business models and attractive market positions and to achieve a significant increase in value within a very short period of time by implementing important operational improvements.

This strong exit momentum continued in the current financial year 2026. The successful sale of Kalzip, WIJ Special Media (formerly part of Prénatal) and the inTime Group as well as the signed agreements to sell Relobus and Conexus enabled the optimization of the portfolio and the increase in value. In addition, Mutares expects further attractive exits with significant potential for value creation in the further course of the year, particularly for investments in the defense, energy and energy infrastructure sectors in the Engineering & Technology segment.

Portfolio resegmentation implemented in the 2025 financial year

In the course of the 2025 financial year, Mutares carried out a restructuring of the portfolio in response to changing market conditions and, in particular, changes in the portfolio as a result of completed acquisitions and exit transactions. The aim is to align the strategic control and operational management of the portfolio companies even more closely with their operating business models.

At the center of the new structure was the introduction of the Infrastructure and Special Industry segmentsegment, which bundles portfolio companies from the critical infrastructure sector and other highly specialized industries, including the defence sector. The investments from the former retail and food segment were transferred to the expanded Goods and Services segment segment, which now combines thematically cyclical consumer and service companies. Automotive & Mobility remains an early-cycle segment, while Engineering & Technology continues to cover late-cycle sectors.

Partially supportive operating performance in the Mutares portfolio

In a market environment that remained challenging in some areas, particularly in Automotive & Mobility and in parts of the Goods & Services segment, Mutares' portfolio companies introduced and/or continued comprehensive restructuring and transformation programs in the financial year 2025. Portfolio companies such as Efacec, NEM Energy Group, Magirus and Donges SteelTec are benefiting from positive momentum with strong order intake and thus increasing profitability. The market environment remains extremely attractive: increasing electrification as part of the energy transition, rising demand for electricity due to artificial intelligence and a significant increase in defense budgets are ensuring that demand remains high. At the same time, growing competition for high-quality assets is leading to rising valuations and opening up further attractive exit opportunities with considerable potential for value appreciation.

In the reporting period, the portfolio companies in the Automotive & Mobility segment segment continued to face short-term cancellations or postponements of orders from car manufacturers in some cases. Nevertheless, the segment's sales rose to 2,506.6 million euros in the 2025 financial year (previous year: 2,223.2 million euros). The increase was mainly due to the segment's acquisitions, in particular SFC Climate as an additional acquisition for the SFC Group at the beginning of the 2025 financial year and Matikon in the previous year and Matikon Trim in the 2025 financial year as additional acquisitions for Amaneos. The segment's EBITDA amounted to EUR 109.4 million (previous year: EUR 130.1 million) and was influenced by gains from a bargain purchase totalling EUR 208.2 million (previous year: EUR 219.7 million). Adjusted EBITDA improved to EUR -8.9 million (previous year: EUR -45.9 million), mainly due to the improved profitability at LMS and the positive profit contributions from the newly acquired SFC Climate and TSM (FerrAl United Group).

The portfolio companies in the Engineering & Technology & Technology[1] segment generated sales of EUR 1,337.3 million in the 2025 financial year (previous year: EUR 1,181.0 million). In addition to the full-year consolidation of the Sofinter Group, which was acquired in the previous year, the organic sales growth of the Efacec Group and the Donges Group also contributed to this result. In contrast, sales at Byldis fell year-on-year against the backdrop of a continued weak construction sector. The segment's EBITDA reached EUR 270.3 million (previous year: EUR -49.0 million) and was influenced by the successful partial exit of Steyr Motors, among other things. The adjusted EBITDA of EUR 35.3 million (previous year: EUR -9.9 million) reflects the positive development of Efacec, Guascor Energy and the Donges Group, each of which recorded a welcome increase in profits.

The subsidiaries in the Infrastructure and Special Industry segmentsegment, which was newly established in the 2025 financial year, generated sales of 1,235.5 million euros in the reporting year (previous year: 275.3 million euros). This increase is mainly due to new acquisitions, in particular Magirus, Buderus Edelstahl and Nervión. The segment's EBITDA reached EUR 255.9 million (previous year: EUR 16.7 million) and was significantly influenced by the profits from the bargain purchase of the acquisitions, in particular Magirus and Buderus Edelstahl. Adjusted EBITDA for the reporting period amounted to EUR -14.4 million (previous year: EUR 17.1 million) and reflects in particular the negative profit contribution from Buderus, while other newly acquired investments in the segment, in particular Kuljettava, already made positive contributions and the Terranor Group increased its profitability compared to the previous year.

Sales in the Goods and Services segment amounted to 1,404.6 million euros in the 2025 financial year (previous year: 1,581.9 million euros). The decline, which is attributable to disposals in both the current and previous financial year as well as organic sales declines at Lapeyre and Stuart, could not be fully offset by new acquisitions. The segment's EBITDA amounted to EUR 42.5 million (previous year: EUR 17.8 million), with performance in both the current and previous financial year benefiting from the effects of acquisitions and disposals - in the reporting period from the partial disposal of Locapharm and in the previous year from the disposal of Frigoscandia. Adjusted EBITDA for the reporting year amounted to

EUR -50.6 million (previous year: EUR -51.8 million), with the trend being negatively impacted by the decline in profitability at Stuart and Lapeyre due to falling sales and the negative profit contribution from Natura, while other portfolio companies in the segment, led by GoCollective and Alterga, recorded a pleasing increase in adjusted EBITDA compared to the same period of the previous year.

Adjusted EBITDA varies significantly between the three stages of value creation that portfolio companies typically go through during their time with Mutares (Realignment, Optimization and Harvesting). As in the past, the classification of the portfolio into these three phases was adjusted with the publication of the results for the first quarter of the financial year based on the progress made in the transformation as well as the submitted and approved budget.

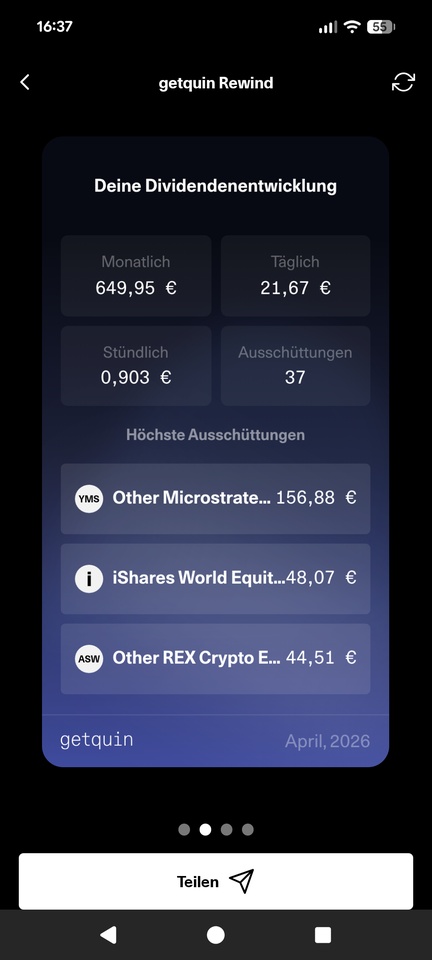

Proposed dividend of EUR 2.00 per share

Mutares pursues a dividend policy that enables shareholders to participate directly and continuously in the company's success while supporting the financing of the Group's further expansion and growth. For the financial year 2025, the Management Board and the Supervisory Board will propose to the Annual General Meeting on July 3, 2026 the distribution of a total dividend of EUR 2.00 per share, which Mutares considers to be a minimum dividend. Should a significant contribution to profits and liquidity exit in the future, Mutares intends to provide shareholders with a windfall profit through a performance dividend.

Non-fulfilment of a financial covenant at the end of the financial year 2025 and waiver of a review before June 30, 2026

In the 2025 financial year, a condition relating to the ratio of consolidated net debt to consolidated equity, as contained in the terms and conditions of the 2023/2027 bond (ISIN NO0012530965) and the 2024/2029 bond (ISIN NO0013325407), was not met. Based on the already signed acquisitions of Wartsila Gas Solutions and the ETP business of SABIC, the Management Board expects the financial ratio to be reached again by the end of June 2026 and to be significantly below the threshold. Mutares has therefore requested the bondholders pursuant to a written procedure ("Written Resolution"), as provided for in the terms and conditions of the Bonds, to waive compliance with the financial ratio regarding consolidated net debt to consolidated equity for the financial year 2025, effective as of June 29, 2025, and has received broad approval. In this context, the review of compliance with this financial ratio will also be waived until June 29, 2026.

Further reduction of the planned Mutares bonds

With regard to Mutares Holding's debt, the plan is to reduce the outstanding nominal amount between the two bonds from the current EUR 385 million to a nominal amount of EUR 250 million to EUR 300 million by the end of the financial year 2026. To this end, the Management Board intends to purchase at least EUR 25 million of the 2023/2027 bond from the second quarter of the 2026 financial year.

Against this background, Mutares intends to offer the creditors of the 2023/2027 Bond a partial repurchase of the Bond in the amount of up to EUR 25 million (subject to an adjustment of the volume) in exchange for cash in a voluntary public offer ("Offer"). The Offer Period is scheduled to commence on May 8, 2026. The repurchase price under the Offer will be announced in the Offer Documents.

The Company will publish further details of the Offer on its website (https://ir.mutares.com/) prior to the commencement of the Offer Period.

Important strategic decisions taken after the balance sheet date - new segment as additional growth driver

Following the balance sheet date, Mutares set a key strategic course for the next phase of the Group's development. The focus is on a transformative acquisition that will sustainably expand the company's industrial footprint.

With the agreement signed in January 2026 to acquire SABIC's Engineering Thermoplastics business in the Americas and Europe, Mutares marks a significant milestone in the company's history. The deal is expected to close in the second quarter of 2026. With revenues of approximately EUR 2.0 billion and equity of around EUR 2.0 billion, this is the largest acquisition in Mutares' history.

The transaction also lays the foundation for the establishment of the new "Chemicals & Materials" segment in the financial year 2026, through which Mutares will enter the specialty chemicals and high-performance materials sector on a significant scale for the first time. The new segment creates an additional, globally oriented growth pillar with a strong presence, particularly in North and South America. The broad customer base in attractive industries and established premium brands offer excellent conditions for operational excellence, innovation and sustainable value creation in the new segment. The development of the segment will be complemented by further transactions, including Venator Ultramarine Blue Pigments.

With the successful completion of the capital increase in April 2026, which generated gross proceeds of EUR 105 million, Mutares has also laid the foundation for further growth and expanded its successful business model as part of its accelerated US expansion. In addition to the existing office in Chicago, Mutares plans to open a second office in the US to fully exploit the potential of the US market. The current transaction pipeline in the USA includes attractive acquisition opportunities with a total sales volume of around EUR 4.8 billion. The first effects of the US expansion can already be seen in the agreements signed in April 2026 to acquire two Magna suppliers as add-on products for Amaneos and FerrAl United - specifically to strengthen the HiLo Group.

Forecast for 2026 and medium-term outlook

Based on the transactions concluded and signed as of the preparation date for the current financial year 2026, the assumptions regarding further planned transactions during the year and the plans for the individual portfolio companies, the Management Board expects the revenues of the Mutares Group to increase to between EUR 7.9 billion and EUR 9.1 billion for the financial year 2026 (financial year 2025: EUR 6.5 billion).

Mutares Holding's net profit will be influenced primarily by income from the advisory business, dividends from portfolio companies and, in particular, exit proceeds from the sale of investments. According to the Management Board's expectations, the latter are also expected to make a disproportionately large contribution to net profit in the 2026 financial year. In this context, the Executive Board expects the gross proceeds (sales prices) from the planned exit transactions received by the company as cash flows to be significantly higher in the 2026 financial year than in the previous year (2025 financial year: approx. EUR 230 million). On this basis, the company's net profit for the 2026 financial year is expected to be between EUR 165 million and EUR 200 million.

The increasing internationalization, combined with the establishment of the new "Chemicals & Materials" segment, opens up additional growth opportunities for Mutares. Accordingly, the Management Board is aiming for annual growth in Group revenue of at least 25% until financial year 2030. At the same time, Mutares Holding's net profit is expected to increase by at least 25% annually. With regard to the previously communicated medium-term targets of EUR 10 billion in consolidated revenues and a net profit of EUR 200 million for Mutares Holding by the financial year 2028, Mutares expects to achieve these significantly earlier.

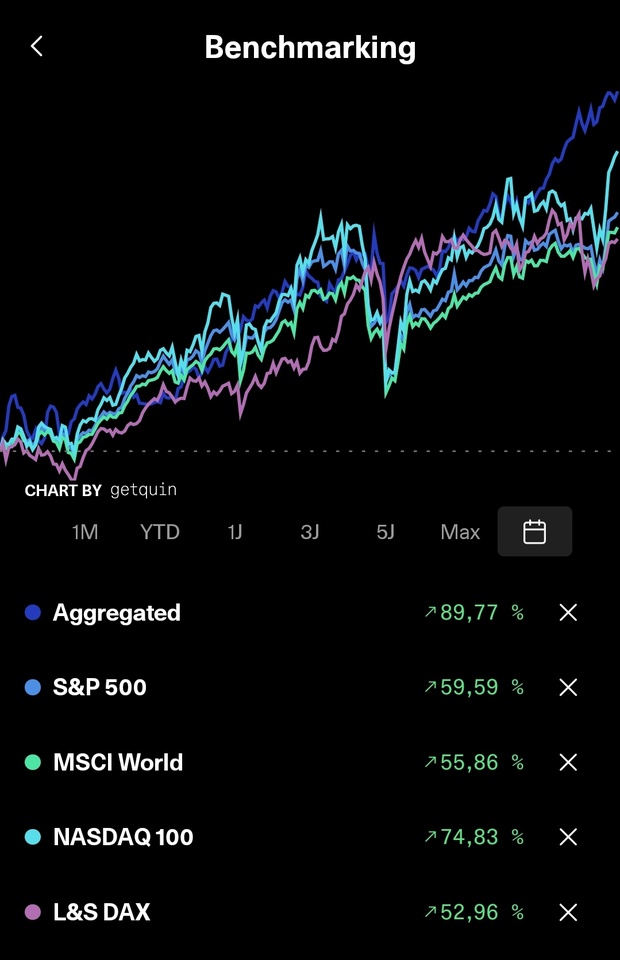

I have been invested with a medium position in the trading portfolio since the announcement of the capital increase, exercised my subscription right and increased the position again today and the share is back in my main dividend portfolio after the sale last summer