...chase away your worries and troubles ☝🏻

..wishing you a great start to the weekend 🌞

Postes

52What a wild ride that was, please ?!? Even the poor kangaroo gets sick...

🦘📈🦘📉🦘📈🦘📉🦘📈 🦘

...and personally don't really believe that the current situation is the end of "Pinky and the Brain"...

... "Pinky" still has to live up to the bets of all his boddies, has his back to the wall domestically with regard to the mid-terms and "the Brain" still has no interest in the end, after all, he still wants to permanently occupy at least southern Lebanon (incorporate the country) and therefore continues to escalate...

...my conclusion from this is that "Pinky" will launch a limited ground offensive over Easter or shortly afterwards in order to sell it strategically at home or to be able to announce something successful at all, the outcome of which is still completely open, while "the Brain" is already forging plans on how he can continue to pursue his goals even after a possible US exit - the end is open - regardless of the fact that the energy issue will still not be resolved after the end 🤷🏻♂️

But let's get back to March...

...even though the month was difficult, it ended with a small gain on the bottom line or even just below the last ATH...

...shows me, conversely, that my consistent strategy and steady fingers have been able to survive such market phases relatively well so far 💪🏻

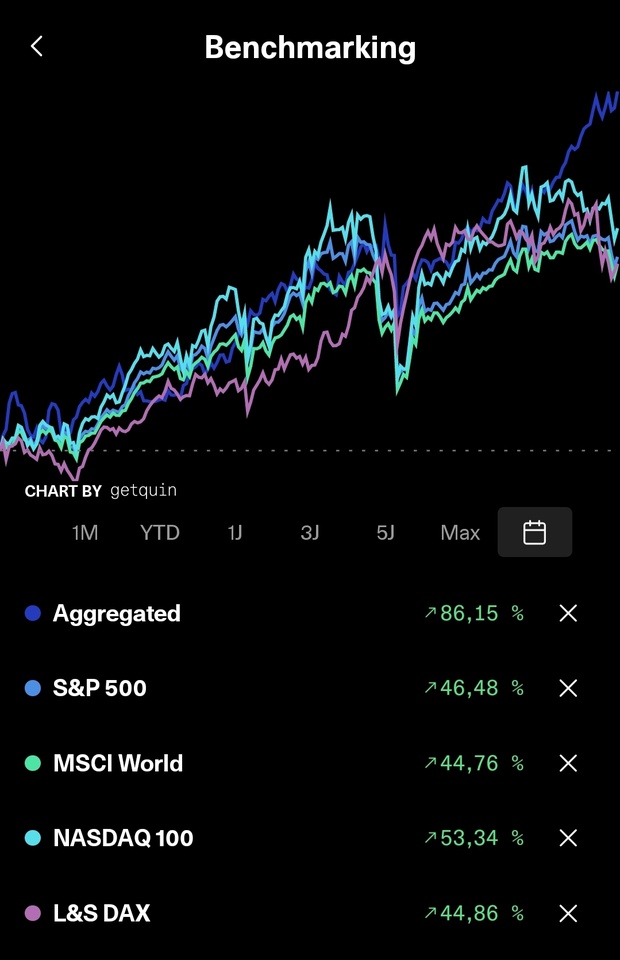

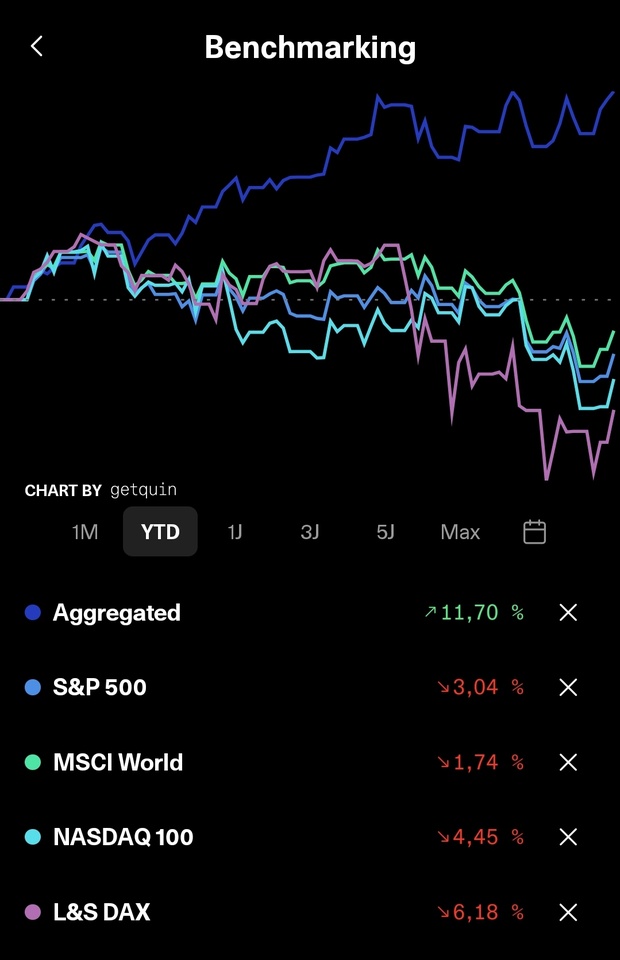

In terms of the year as a whole, the first quarter has also been relatively successful for the circumstances and when I think about the fact that the overall portfolio is just ~1.5-2% below my chosen September milestone, the whole thing reassures me immensely or rather... is going better than forecast 🫠

In the long term, of course, everything is still on target and so not only are the nights still calm and cozy, but I also know that the dividends will continue despite everything, which brings us back to the next topic...

》Dividends《

This month there were €116.68 net dividends, which means an increase of 164.41% YOY 💪🏻

YoC (TTM) is ~6% and thus slightly below the target range, although the good months are yet to come...

》Outflows《

$PDI (+0,37 %) (35x)

$VICI (+0 %) (35x)

》Accesses《

$ALV (+0,38 %) (5x)

$EVD (+0,22 %) (25x)

$FWRG (+0,09 %) (73x)

》TOP 3《

$3750 (+3,28 %) +28,67% (+89,65%)

$VAR (-0,29 %) +23,61% (+55,54%)

$HAUTO (-1,69 %) +11,31% (+79,18%)

》FLOP 3《

$HSBA (+0,42 %) -8,25% (+45,21%)

$ASWM (+0,32 %) -6,51% (-8,38%)

$MUX (-0,28 %) -5,70% (+27,30%)

Furthermore, all contracts for the continuation of my training were signed and sealed this month, which was also pleasing and comes with a small salary increase 😊

That's all from me for now and I wish us all a successful April

+ 1

The Norwegian oil and gas company Vår Energi $VAR (-0,29 %) and its partner Kistos Energy have drilled a dry well in the Balder area in the North Sea.

The well 25/8-C-23 D, named "Prince Updip", was drilled from the Ringhorne platform, just over 200 kilometers west of Stavanger, as part of production license 027.

Vår Energi is the operator of the license with a 90% interest, while partner Kistos Energy (Norway) holds the remaining 10%.

Production license 027 was awarded in 1969 in the second licensing round on the Norwegian Continental Shelf (NCS). This is the 13th exploration well drilled within the license area. The Balder and Ringhorne Øst fields are also located in this license area.

Exploration activities have already taken place within the production license in 2021, when exploration wells 25/8-20 S, B and C proved hydrocarbons in two levels.

Based on the drilling results, the well was classified as dry with hydrocarbon shows and has now been permanently shut-in and abandoned.

ORLEN Upstream Norway $PKN (-0,57 %) has agreed to acquire from Vår Energi $VAR (-0,29 %) to acquire a 25% stake in the PL293 production license in the North Sea, which includes the unconventional Afrodite gas field.

The Afrodite gas field has the potential to supply ORLEN with almost 2 billion cubic meters of natural gas net, the company said.

The project will also serve as a testing ground for new methods of producing unconventional resources on the continental shelf, including Victoria, the largest undeveloped gas deposit in Norway, in which ORLEN also has an interest.

Afrodite was discovered in 2008, but due to the challenging high pressure/high temperature environment, its development was not actively pursued until recently. The license partners have now decided to drill an appraisal well to assess the feasibility of production using stimulation technologies and to better quantify the recoverable reserves.

Current estimates put the recoverable resources at approximately 7.5 billion cubic meters of gas, of which ORLEN accounts for approximately 1.9 billion cubic meters. Afrodite could be developed as a tie-in to the nearby Kvitebjørn field, in which ORLEN Upstream Norway also has an interest, which would create additional synergies.

Vår Energi $VAR (-0,29 %) announces its financial results for the fourth quarter and full year 2025.

The company also holds its Capital Markets Update (CMU) and presents an updated strategy for increased production and value over time, with significant cash flow generation and attractive dividends.

"We are pleased to have achieved transformative growth in 2025, doubling our production in just two years. The company achieved record production, a high reserve replacement ratio, strong financial performance and significant value creation, while further de-risking the future through the completion and commissioning of nine projects, including Jotun FPSO in the Balder field and Johan Castberg."

"Vår Energi has never been in a stronger position for long-term value creation and continues to deliver attractive returns, reflected in distributions to shareholders for 2025 of US$1.2 billion, in line with guidance," said Nick Walker, CEO of Vår Energi.

Vår Energi forecasts production in the range of 390 to 410 thousand barrels of oil equivalent per day (kboepd) for the full year 2026 and increases the long-term production target to more than 400 kboepd.

"This is supported by a portfolio of 13 high quality projects under execution, a flexible pipeline of around 30 early stage projects in the maturing phase and a strengthened asset base with increased reserves and resources," Walker continued.

"Driven by an entrepreneurial, performance-driven organization, we continue to leverage incremental improvements across the Company, including enhanced recovery through infill drilling and targeted exploration, while becoming increasingly efficient and reducing costs."

"This continues to provide resilience in a volatile business environment, strong cash flow generation and attractive long-term returns for shareholders in line with our stated dividend policy of 25-30% of cash flow from operations after tax over the full cycle," Walker concluded.

A transformative 2025:

》Record high production《

● Production of 397 kboepd per quarter and total annual production of 332 kboepd in 2025

● The outlook for the company is less risky following the completion of important projects

● Nine new growth projects were launched as planned during the year, adding around 180 kboepd to peak production

● Strong operational performance in 2025 with an average production efficiency of 92%

Strong financial performance

● Strong after-tax CFFO of USD 1.3 billion in the quarter and USD 4.6 billion for the full year 2025

● Available liquidity of USD 3.5 billion and leverage ratio of 0.8x at year-end 2025

● Production costs per unit at the lower end of the annual forecast at USD 11.1 per boe and USD 10.0 per boe for the quarter

》Development of long-term value creation for the future《

● 10 project approvals in 2025, development of 160 million barrels of oil equivalent (mmboe) net with an average break-even of USD 30 per boe

● High quality exploration activities with six commercial discoveries in 2025

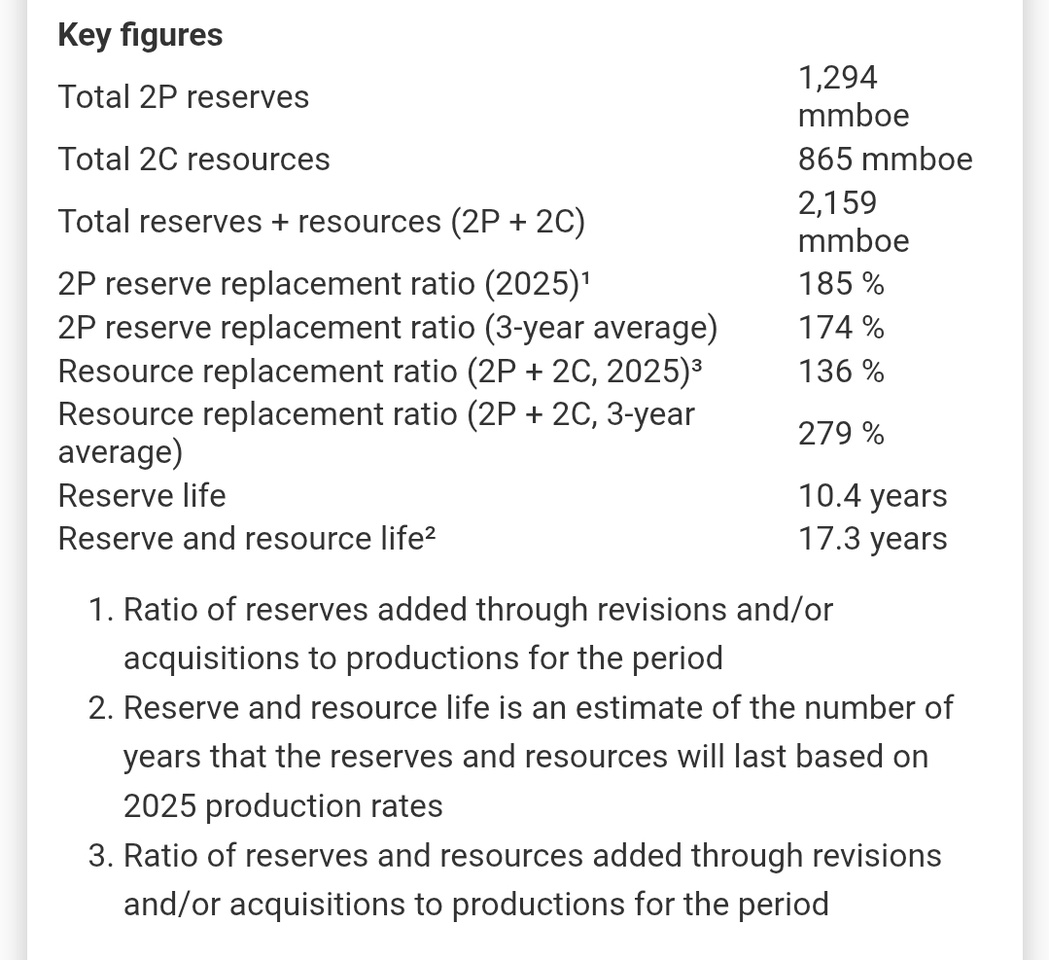

● Increase in reserves and resources2 by 2.2 billion boe by year-end 2025 with a 2P reserve replacement ratio of 185

》Attractive dividend payout《

● The dividend for the fourth quarter of USD 300 million (NOK 1.209 per share) will be paid on February 12

● Dividend guidance of USD 300 million for Q1 2026 in line with dividend policy of 25-30% of CFFO after tax over the cycles

CMU highlights - More value for longer:

》Targeting higher production and value creation for a longer period《

● Low-risk company with completed major projects, whose production forecast for the full year 2026 is in line with the previous forecast with a record value of 390-410 kboepd

● High quality barrels with full year 2026 production cost guidance of around USD 10 per boe, reiterating the aim to maintain this level in the long term

● Longer-term higher production, raising the production target to over 400 kboepd in the long term

● A significant resource base of around 2.2 billion boe of proven and probable (2P) reserves, as well as 2C contingent resources, provides a solid foundation for long-term value creation

● 13 projects under implementation unlock 210 mmboe of net 2P reserves with low operating costs, a break-even point at around USD 30 per boe and an IRR of over 30%

● Progress on around 30 high quality early stage projects with a target of around 550 mmboe of net 2C resources with attractive economics

● Up to 8 new project approvals in 2026

● Investments of USD 2.5 to 2.7 billion expected for 2026, with average annual investments of USD 2.5 billion in the period 2027-2032

》Creating more value《

● Continued high exploration activity with 12 planned wells in 2026 targeting approximately 75 million boe of net risked reserves

● Exploration expenditure for 2026 of USD 250 to 300 million

● A significant, diversified exploration portfolio with over 1 billion boe of net risked reserves

》Safe and responsible《

● Upper quartile emissions intensity in the industry of around 9 kg CO2e/boe

● Strong ESG ratings, among the top 15% of the oil and gas industry worldwide

》Securing long-term returns《

● Gradual improvement for greater resilience and flexibility

● Delivery of high-quality barrels with a free cash flow break-even of around USD 40 per boe in the period 2026-2032

● Strong free cash flow generation of USD 5 to 10 billion in the period 2026-2032 and a flexible capital expenditure program with around 60% uncommitted capital expenditure

● Robust project portfolio, balanced commodity mix and significant uncommitted capital support resilience, flexibility and long-term dividend policy

》FINANCIAL SUMMARY《

Vår Energi has delivered and the outlook remains rosy with consistently good dividends 💪🏻

.... Contrary to the information provided by GQ, according to the press release from $VAR (-0,29 %) today, the ex-dividend date for the dividend is today, 03.02.2026. The dividend will be paid on 12.02.2026. Incidentally, it is NOK 1.209 per share.

What a start to the new year - everything from high spirits to geopolitical tensions to a historic correction - and it seems to be continuing just as turbulently as it began...

...but despite the events and the fact that there were only 2 small additional purchases last month, these circumstances don't really seem to bother my portfolio and so a new ATH was reached on the penultimate trading day and closed just below it on the last day.

I am quite satisfied with the 4.70% achieved under the circumstances and it shows me that my selection (.oO dividends do not hurt) is not so bad at all in order not to get under water even in such waters.

In the long term, my strategy continues to pay off positively and there is no reason for me to really change anything here...

...except that this year there will be a little more focus on growth in addition to dividends.

Which brings us directly to the next topic...

...after a good +3804.58% dividend growth in 2024, it was another +148.57% last year and, with the +40.37% forecast so far this year, should easily be enough to achieve my basic target of €2000 net dividend.

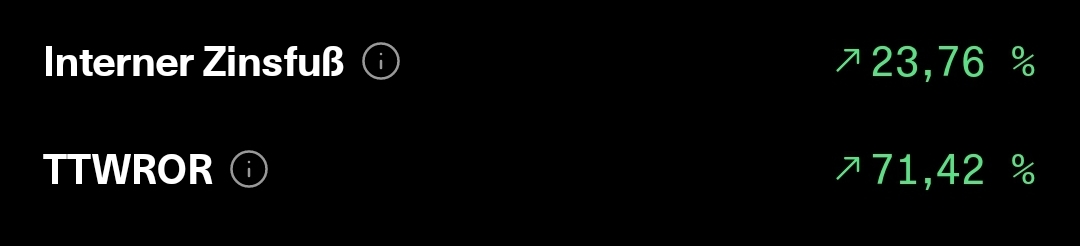

In my view, the overall rate of return is also suitable for the time being and will of course change somewhat over the course of the year...

...it is also fitting that January is a somewhat weaker dividend month, but still tastes good with a net dividend of € 104.16.

》Single stocks top 3《

$HAUTO (-1,69 %) +11,28% (+35,55%)

$RIO (-0,37 %) +10,28% (+41,03%)

$VAR (-0,29 %) +9,50% (+10,20%)

》 Individual stocks Flop 3《

$YYYY (+0,9 %) -7,96% (-4,27%)

$3750 (+3,28 %) -2,58% (+46,54%)

$VICI (+0 %) -0,84% (+17,41%)

》Additions/departures 《

none

》Increased《

$VICI (+0 %) (10x)

$1211 (+0,92 %) (10x)

Apart from that, there were 2 other pieces of positive news in my private life...firstly, the next check-up is still without findings and secondly, I now have confirmation from the pension provider that I can continue my further training as an accounting specialist (IHK) this year, which was interrupted by the operation. What's more, this will now be taken a little further and I'll also be taking the certification in DATEV and DATEV payroll accounting at the same time...can't hurt 🤫👍🏻

And so I wish us all continued good luck, a nice rest of the Sunday and maximum profits ✌🏻

+ 1

Vår Energi ASA $VAR (-0,29 %) publishes the annual report on the company's reserves for 2025, showing proven and probable reserves (2P) and contingent resources (2C) of approximately 2.2 billion barrels of oil equivalent (boe).

"2025 was a year of change for Vår Energi. We are pleased to have not only achieved significant production growth, but also to have further expanded our reserves and resource base. Total reserves and resources amount to 2.2 billion boe, with a 2P reserve replacement ratio¹ of 185% for the year and 174% on a three-year average. The lifetime of the reserves and resources² is around 17 years. This is a solid foundation to achieve higher production and value in the long term and we are working hard to realize a number of attractive projects to take advantage of this opportunity," says CEO Nick Walker.

In 2025, Vår Energi started production from nine new projects as planned and approved ten new development projects.

The company continues to implement initiatives to increase production from producing fields through additional infill drilling.

The approval of new development projects and the extension of the life of existing fields are the main reasons for the increased net reserve estimates.

Total 2P reserves as at December 31, 2025 amounted to 1,294 million boe (mmboe).

In addition, the significant 2C resources are an essential part of Vår Energi's strategy to create future value.

As of December 31, 2025, the total 2C resources amount to 865 mmboe, which is a slight decrease compared to 2024 as projects move into implementation.

Exploration successes and technical revisions contribute positively as the company actively mitigates risks and transfers discovered resources to new development projects.

Based on the combined 2P reserves and 2C resources, the resource replacement ratio³ for the year is 136% and the three-year average is 279%.

The 2P reserves and 2C resources at the end of 2025 correspond to the Petroleum Resources Management System (PRMS). International petroleum consultants DeGolyer and MacNaughton have conducted an independent evaluation of Vår Energi's portfolio of reserves in accordance with PRMS as of December 31, 2025.

Vår Energi ASA $VAR (-0,29 %) will publish its financial report for the fourth quarter of 2025 on February 10.

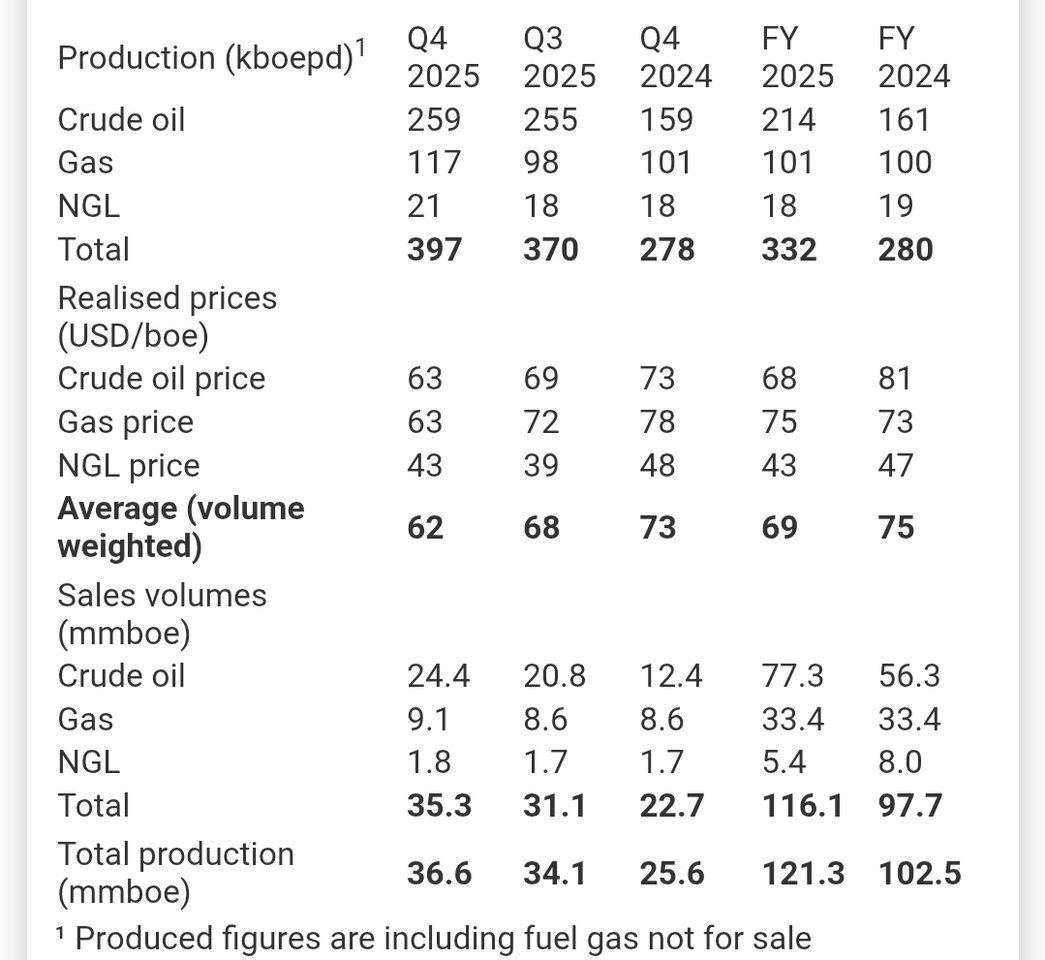

Today, the company is providing updated information on production, sales volumes and other relevant points.

Vår Energi's net production of oil, liquids and natural gas averaged 397 thousand barrels of oil equivalent per day (kboepd) in the fourth quarter of 2025, an increase of 7% compared to the third quarter and an increase of 43% compared to the fourth quarter of 2024.

Total production for the year as a whole averaged 332 kboepd, which is within the range forecast for the year.

The operational issues at Johan Castberg and Jotun FPSO reported in December were resolved in early January and production is now back to the expected level.

The production split in the fourth quarter was 71% oil and NGL (liquids) and 29% gas.

The total production volume amounted to 36.6 million barrels of oil equivalent (mmboe), while the sales volume in the quarter was 35.3 mmboe. The shortfall is mainly due to the timing of LNG deliveries in the quarter.

Vår Energi achieved an average realized price (volume weighted) of USD 62 per boe in the quarter.

The realized crude oil price was USD 63 per barrel.

The realized gas price of USD 63 per boe is around USD 4 above the average reference price on the spot market.

Fixed-price contracts accounted for around 15 % of the gas volumes sold in the fourth quarter, at an average price of USD 75 per boe.

》Other items《

Vår Energi's functional currency is NOK, while interest-bearing loans are denominated in USD and EUR. The weakening of the NOK in the fourth quarter of 2025 resulted in a net exchange rate loss of around USD 40 million.

Due to the company's history of mergers and acquisitions, Vår Energi has several assets that are measured at fair value in the balance sheet. Changes in assumptions, cost and production profiles can lead to impairment losses and reversals of impairment losses.

The non-cash impairment of technical goodwill in the fourth quarter is estimated at around USD 70 million before tax (around USD 70 million after tax) and is related to Njord Area, Gjøa and Snorre.

An adjustment following a revaluation process at Snorre, which reduced Vår Energi's equity share from 18.55% to 18.16%, accounts for most of the impairment in the quarter.

The net impairment for the full year amounted to USD 26 million after tax.

As previously disclosed, the following items impacted free cash flow in the fourth quarter:

3 cash tax payments totaling approximately NOK 8.2 billion (approximately USD 820 million) and a third quarter dividend payment of USD 300 million paid in November.

In addition, the company paid around USD 180 million in the quarter in connection with the acquisition of TotalEnergies' stake in the "Ekofisk Previously Produced Fields" project. This includes a cash payment of USD 147 million and a cash settlement payment for costs incurred in the period from January 1, 2025.

The above information is based on a preliminary assessment of the Company's financial results for the fourth quarter of 2025 and is subject to change until the financial statements are finally approved and published by the Company.

Meilleurs créateurs cette semaine