Hello to the community,

The EarningsSeason has hit the start button this week. To minimize the euphoria a little😂 and get the weekend off to a good start, I would like to introduce you to some "indirect" players in the cybersecurity sector, which I am sure many of you are not yet familiar with.

Today we are talking about A10 Networks $ATEN (+1,09%)

🛡️ A10 Networks : The invisible gatekeeper of the AI infrastructure

A10 Networks is not a hyped software store that burns money on marketing. It is the specialized high performance engineer in the engine room of the Internet. While Crowdstrike, for example $CRWD (+3,52%) protects the end devices, A10 ensures that the huge data streams from AI, 5G and data centers do not collapse and arrive safely.

1. the business model: the "floodgate" in the data tsunami 🌊

A10 $ATEN (+1,09%) acts as a specialist for Application Delivery Controller (ADC) and DDoS protection at carrier level.

- The mechanism: When millions of users access an app simultaneously or AI models eat up gigabytes of data, A10 distributes this traffic (load balancing) while filtering out malicious attacks (DDoS) in real time.

- The genius: A10 $ATEN (+1,09%) sits directly in the hardware layer of the major telcos (Verizon $VZ (+2,76%) T-Mobile $TMUS (+1,48%) and data centers. Without A10 $ATEN (+1,09%) the network stands still.

- AI as a growth driver: AI data centers need extremely efficient data distribution. A10 $ATEN (+1,09%) provides exactly the "locks" that prevent expensive GPUs from having to wait idle.

2. the key figures (as of April 2026) 📊

- Market capitalization: Approx. USD 1.8 billion (A compact mid-cap with takeover potential).

- Share price: Currently approx. USD 25.00 (Stable in a volatile tech market).

- Gross margin: Outstanding 80-82 %. That's software level for physical infrastructure. ✅

- Return on equity (ROE): approx. 20-22 %. Extremely solid for an infrastructure company.

- Balance sheet strength:

Net cash position of approx. USD 160 million. No debt, which is a burden with high interest rates. ✅

- Dividend: approx. 1.0 % yield - rare in the tech sector, underlines the cash flow strength.

Summary & outlook

Strengths:

1. High cash generation: The company is accumulating massive amounts of liquidity.

2. Scalability: With a gross margin of 80%, almost every additional dollar of sales flows directly into operating profit.

3. Market position: 9 of the top 10 telecom operators and 8 of the top 10 cloud providers use A10 $ATEN (+1,09%) which indicates very high customer quality (hyperscale).

3. why is the share exciting right now? 🚀

1. AI infrastructure leverage: While Nvidia sells the shovels, A10 builds $ATEN (+1,09%) builds the railroad tracks on which the AI traffic rolls. This "second wave AI play" is not yet fully priced in by the market. ✅

2. Profitability monster: A10 $ATEN (+1,09%) has changed from a pure growth promise to an FCF generator. The operating margins (adj. ~24%) show massive operating leverage. ✅

3. Moat through specialization: In the world of 5G carriers, there are few alternatives. Once you have installed the Thunder series from A10 $ATEN (+1,09%) will not switch to a competitor because of a few dollars (high switching costs). ✅

4. Valuation discrepancy: While cyber security players such as Crowdstrike $CRWD (+3,52%) or Palo Alto $PANW (+3,43%) are trading at P/E ratios above 60, you can get A10 $ATEN (+1,09%) for a moderate P/E ratio of approx. 18-20. ✅

5. Takeover candidate: For giants like Cisco $CSCO (+0,54%) or F5 $FFIV (+0,33%) A10 would be $ATEN (+1,09%) would be a "snack" to secure dominance in the AI traffic market. ✅

Additional insider facts (The "Deep Dive" bonus) 💡

- Stickiness: Customer loyalty among telcos and governments is extremely high. Once certified, the hardware often remains in use for 5-10 years.

- Security synergy: A10 $ATEN (+1,09%) combines traffic management with security. This saves customers hardware space and power - a critical argument in modern data centers.

- Software transition: A10 $ATEN (+1,09%) is increasingly switching to subscriptions. This makes revenues more predictable and valuable.

5. risks ⚠️

- Competition: F5 Networks $FFIV (+0,33%) is the big gorilla in the market; A10 $ATEN (+1,09%) must always be one step ahead technologically to avoid being crushed. ❗️

- Cyclicality: The expansion of 5G networks is taking place in waves. A halt in investment by the major telcos has a direct impact on sales. ❗️

- Cloud migration: If absolutely everything moves to the public cloud (AWS/Azure), dedicated hardware will become less important - A10 $ATEN (+1,09%) must win here with its virtual solutions. ❗️

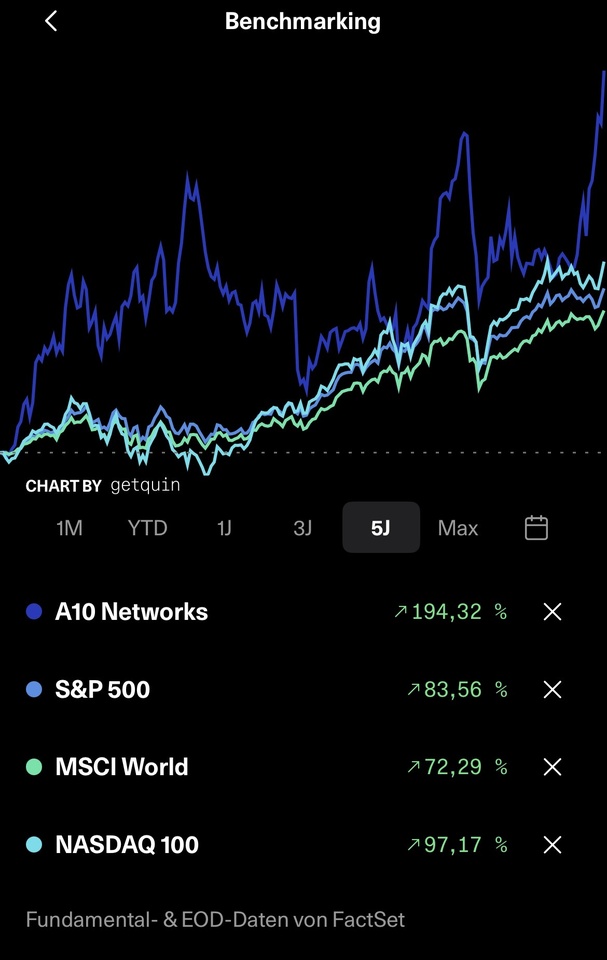

A10 Networks $ATEN (+1,09%) has proven to be a massive alpha generator over 5 years and has clearly outperformed both the S&P 500 and the Nasdaq 100. The company benefited disproportionately from the special boom in cybersecurity and network resilience.

🗓️ EARNINGS-PREP: A10 NETWORKS ($ATEN) - Q1 2026

1. DATE & CONSENSUS

- Date: April 28, 2026 (after US market close)

- EPS expectation: $0.18 - $0.20 (adj.)

- Revenue expectation: ~$70.5m - $72m.

- Whisper Number: If they crack $73m, the house will burn (positive).

6.personal conclusion + Reaper verdict bonus😂

A10 Networks $ATEN (+1,09%) is the sensible bet on the data boom. While others speculate on the next AI chatbot, here you are investing in the physical necessity of data flow.

The valuation is almost outrageously cheap for this quality and net cash position. Anyone looking for a profitable tech stock with a safety net will find it here.

🤖 Jack's mustard: "A10 $ATEN (+1,09%) is the guy who doesn't sell maps in a gold-digger mood, but builds the bridges over the rivers. Everyone has to cross, whether they find gold or not. While people are buying $NVDA (-0,26%) sell their grandmother for Nvidia shares, you get A10 $ATEN (+1,09%) for the price of a proper dinner. Anyone who doesn't grab it here doesn't understand how the internet works under the hood. A10 Networks $ATEN (+1,09%) is not a Ferrari $RACE (+1,91%) but a solid Toyota $7203 (-0,24%) with a built-in cash machine. The valuation is fair to favorable, the balance sheet is cleaner than an operating room. Anyone hoping for "AI moonshots" is in the wrong place. Those looking for cash flow stability and shareholder yield are right.

We see ourselves at $35 when the market realizes that you can't squeeze AI through Wi-Fi cables from the hardware store."

Reaper Score: 8/10

@Get_Rich_or_Die_Tryin

@Tenbagger2024

in that sense, have a nice weekend

your stock master ✌️