--> shares are up nearly 30% today. Congrats to the bulls 🚀🥳

- GigaCloud Technology (NASDAQ:GCT): Q2 Non-GAAP EPS of $1.14 beats by $0.56.

- Revenue of $322.6M (+3.8% Y/Y) beats by $32.52M.

Puestos

8--> shares are up nearly 30% today. Congrats to the bulls 🚀🥳

In case someone of you missed it:

EPS Normalized Actual

$0.83 (Beat by $0.30)

EPS GAAP Actual

$0.68 (Beat by $0.20)

Revenue Actual

$271.91M

Revenue Surprise

Beat by $12.11M

For the next quarter they expect revenues to be in the range of 275 to 305 million $.

Additionally they repurchased nearly 10% of their stocks with the recent Buyback Program of around 60 million Dollar. They added another 16 million to the buyback program and are still holding almost half of their market cap in cash.

Any of you guys may invested and has an opinion about the numbers?

Any thoughts about this stock $GCT (+0,92 %) ? It seems to be a bargain with no risk ar all looking at the valuation.

Hello everyone,

At the end of last year, I published my "top picks list" here, in which I presented the stocks that I have put on my watchlist for 2024 and am also partially invested in (unfortunately not in all of them 😁).

At the time, I had compiled a list of stocks recommended by well-known analysts and put them through "my requirements profile". The original 100 stock ideas then became the list below. A year later, I'm looking back. This was the performance:

🟢 $TMUS (+5,63 %) +1,63%

🟢 Sterling Infrastructure: +100.68%

🟢 $CRM (+3,71 %) Salesforce: +28.14%

🟢 $RR. (+3,42 %) Rolls-Royce: +92.56%

🟢 $MOD (-3,73 %) Modine Manufacturing: +98.68%

🟠 $MHO (+2,33 %) M/I Homes: -1.46%

🟢 $META (-1,77 %) Meta: +68.52%

🟢 $MCD (+0,95 %) McDonalds: +0.14%

🟢 $MA (+1,59 %) Mastercard: +26.26%

🟢 $ISP (+2,06 %) Intesa Sanpaolo: +45.44%

🟢 $ISRG (+1,87 %) Intuitive Surgical: +59.62%

🟠 $GCT (+0,92 %) Gigacloud Technologies: -0.66%

🟢 $FDX (-0,09 %) FedEx: +11.11%

🟠 $LPG (-1,02 %) Dorian LPG: -47.70%

🟢 $COST (+0,79 %) Costco: +43.34%

🟢 $US1011372067 Boston Scientific: +63.23%

🟢 $BKNG (+2,7 %) Booking: +44.19%

🟠 $ABX Barrick Gold: -14.73%

🟢 $APP (-1,77 %) Applovin: +753.81%

🟢 $GOOG (+0,1 %) Alphabet: +39.28%

🟢 $AMZN (-1,07 %) Amazon: +48,05%

🟢 $ANF (+3,25 %) Abercrombie & Fitch: +69.99%

As you can see, my stock ideas have done quite well. $APP (-1,77 %) with +753.81% was of course a big hit. $DORIAN With -47.70% it was a pipe-dropper.

🔥 I'm currently working on my top picks list for 2025. If you're interested, I'll be happy to share it again and put it up for discussion!

💬 What were your top picks in 2024? And what were the losers? I will reply to every comment and give you a brief assessment.

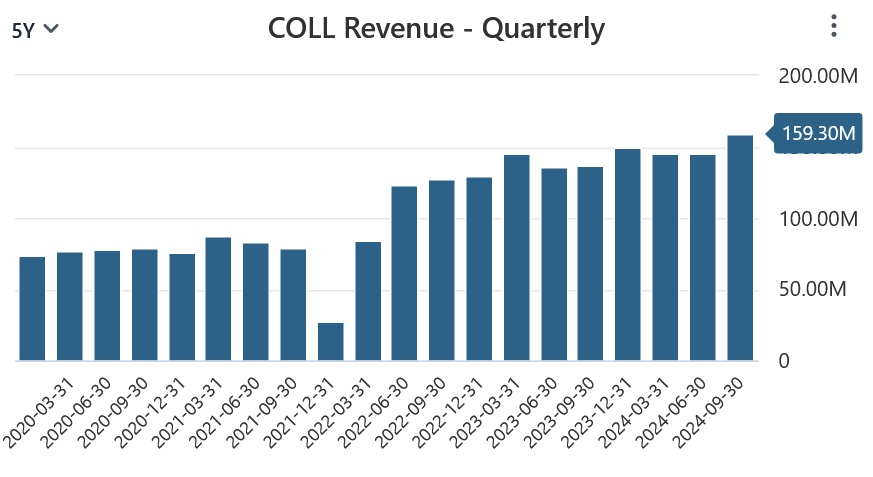

How to Invest in the rapidly growing ADHD market. $COLL (-1,28 %) , a value stock with promising growth!

Collegium Pharmaceutical is a specialty pharmaceutical company that engages in the development and commercialization of medicines for pain management.

The company is not missing a beat. They are growing revenue quarter after quarter and I believe they are worth a second look. Let me give you some quick insights!

$COLL (-1,28 %) has become part of Joel Greenblatt Magic Formula List in August 2023. Since then it has never graduated from the List even after the stock gained over 75%. This suggest that this stock is heavily undervalued. *You can find the updated Magic Formula list at the bottom of this post.

Recently, after going through an acquisition that impacted negatively the financials with one time items, the stock dropped significantly opening up new opportunities to buy in.

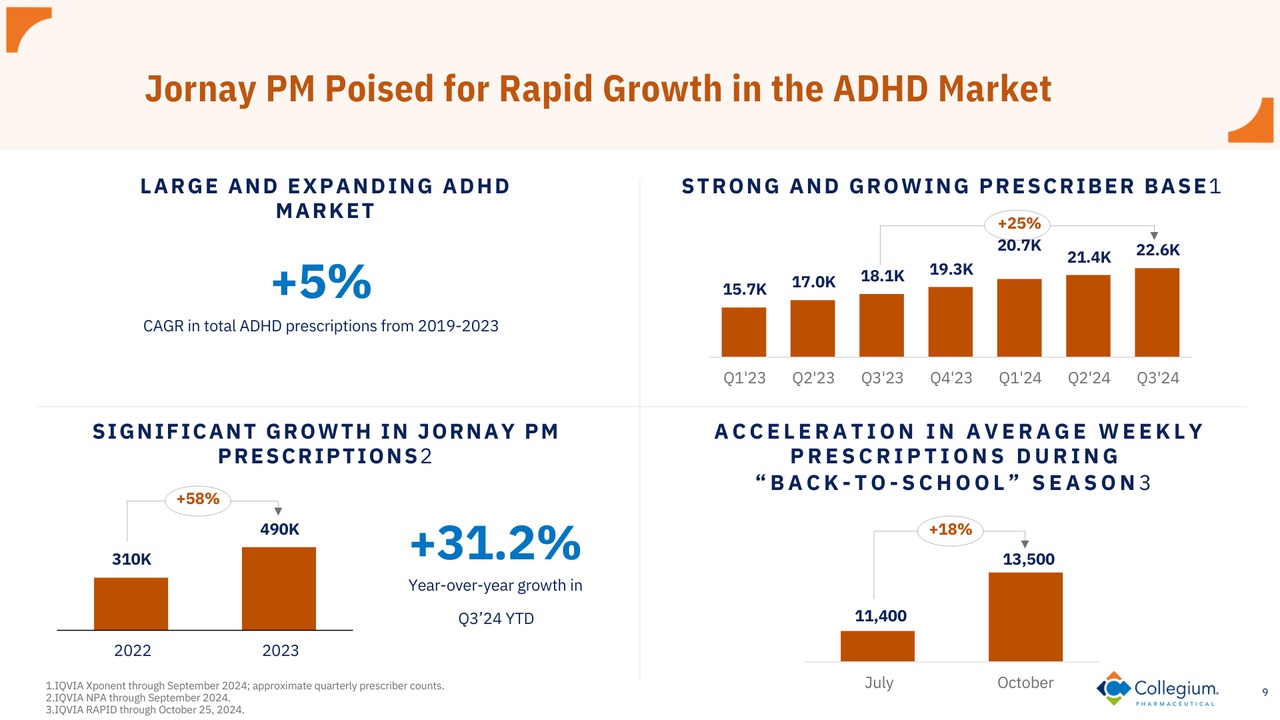

The new acquisition is very promising and will likely drive future growth. $COLL (-1,28 %) bought Ironshore that had an established presence in neurology (ADHD) with Jornay PM. The ADHD market is projected to reach $30.6 billion by 2032.

Collegium reported strong Q3 2024 results, with 17% YoY revenue growth and EBIT margins improving to 35.2%, showcasing operational efficiency.

Still, $COLL (-1,28 %) faces risks, including high financial debt, integration challenges for Jornay PM, and potential revenue concentration in pain management products.

At the same time, the management is executing very well on important areas:

I believe Collegium has compelling valuation metrics and good growth projections that indicate good upside potential.

In conclusion I think Collegium Pharmaceutical's earnings potential is at least as good as it seems, and maybe even better!

Considering all the above, I don't see many reasons against taking a position on this stock right now and holding it for one year as ruled by Joel Greenblatt.

Magic Formula's list (09/12/2024)

$CROX (+1,72 %), is it a value bet?

$CROX (+1,72 %) is a notorious stock for Magic Formula investors. Year after year it comes back into the list (you can find the latest Magic formula list after the picture down below).

Both Revenue and Cash flow keep on growing quarter after quarter, but the stock price keeps on following a wavy pattern. It runs up for a while trying to close the valuation gap and then suddenly it pulls back. Let's try to understand the current situation.

------

$CROX (+1,72 %) is currently trading at a notable low price-to-earnings (P/E) multiple, well below the averages of the Textile – Apparel industry and the broader Retail-Wholesale sector. With a forward 12-month P/E of 8x, the CROX stock reflects a discount to the industry average of 13.77x and the Consumer Discretionary sector’s average of 19.65x.

$CROX (+1,72 %) Stock Looks Undervalued

This shows the CROX stock is undervalued relative to its industry peers, presenting an attractive opportunity for investors seeking exposure to the Consumer Discretionary sector.

Crocs stock price has surged 13.5% year to date, significantly outpacing the industry’s decline of 12.8%. This performance can be attributed to the company’s strategic initiatives, including robust market expansion and product diversification efforts.

Factors Driving the Brand

Crocs is advancing its long-term strategy with key initiatives focused on sustainable growth. The company’s approach centers on three main pillars. These include elevating iconic products across brands to boost awareness and relevance, marketing, digital and retail expansion, and diversifying its product range to appeal to a broader consumer base.

Crocs has strategically expanded its product range, leveraging diversification to attract a broader consumer base. The Crocs brand’s remarkable growth in global awareness and desirability has been fueled by innovative collaborations and unique product offerings.

Current Pressures on CROX

Despite all the positives, Crocs' HEYDUDE brand underperformed, with revenues dropping 17.4% year over year in the third quarter. This decline was led by a 22.9% fall in wholesale revenues and a 9.3% drop in direct-to-consumer (DTC) revenues. Comparable DTC sales for the HEYDUDE brand also decreased by 22.2%.

Looking ahead, Crocs anticipates a relatively subdued consumer environment in the United States until the Black Friday/Cyber Monday holiday period. Per the company, the industry saw heightened promotional activities in China during the mid-season festival, reflecting a more conservative approach by China consumers. As a result, the company expects to see a greater pullback in major cities like Shanghai and Beijing.

Given the challenging macroeconomic conditions, Crocs has issued a cautious outlook for the fourth quarter and 2024, anticipating flat-to-slight revenue growth year over year, in constant currency. The Crocs brand is expected to grow 2% in the fourth quarter, while HEYDUDE revenues may decline 4-6%. International growth is projected to slow due to regulatory challenges in India, and North America faces consumer selectivity and wholesale timing pressures, though DTC revenues remain positive.

For 2024, enterprise revenues are projected to increase 3% year over year in constant currency, which is at the lower end of the previously guided 3-5% growth. Revenues for the Crocs brand are expected to grow 8%, while HEYDUDE brand revenues are anticipated to decline 14.5% due to weaker-than-expected sellouts in both wholesale and digital channels. Previously, management had estimated the Crocs brand’s revenues to grow 7-9% and HEYDUDE’s revenues to decrease 8-10%.

Investment Opinion on CROX

You may find Crocs stock attractive for its undervaluation compared to industry peers, with a lower price-to-earnings ratio. Given strategic initiatives, margin improvements, successful partnerships and a focus on sustainability, the stock presents a compelling investment opportunity for those looking to capitalize on the company’s growth trajectory.

However, CROX faces challenges, including soft revenue expectations, struggles with the HEYDUDE brand and headwinds in China, which could impact its near-term performance. These factors introduce some uncertainty, suggesting a more cautious approach to investing in Crocs at this stage.

Magic Formula's list (01/12/2024)

3 interesting stocks to analyze further!

A quick summary of my analysis on these 3 stocks.

*These stocks were selected from the Magic Formula's list you can find down below after the picture.

Stocks that ends up in the Magic Formula's list are normally beaten up for some reason. I illustrate them as well in my quick analysis.

$HRMY is a commercial-stage pharmaceutical company, focuses on developing and commercializing therapies for patients with rare and other neurological diseases in the United States.

Good news:

Bad news:

Is this stock beaten up for a valid reason?

Frankly I think this is good pick and I don't see any reason why this should not be held into your portfolio for 1 year as advised by Joel Greenblatt. It really sticks out at as one of the market's strongest value stocks in my opinion.

$GCT (+0,92 %) is a Chinese comprehensive B2B ecommerce solutions for large parcel merchandise in the United States. On some aspects it looks similar to Alibaba.

Good news:

Bad news:

Is this stock beaten up for a valid reason?

Many times in the past this company has been beaten up because of it's Chinese origin. Many allude on numbers too good to be true others are scared by the next US presidency. To make it short... there is a lack of trust in this company and it's future. It's undeniably a good company, but will the lack of trust ever evaporate? And will Trump's actions have any effect on it?

$BWMX (-3,93 %) is a direct-to-consumer company selling housewares in the United States and Mexico.

Good news:

Bad news:

Is this stock beaten up for a valid reason?

At the moment I believe so, but as soon as the profits rectify, I can see the stock price jumping and finally recognising the true value of the company. But it's kind of a bet on when this will happen. If you are in for the high dividend, you are patient and you are ready to take some risks this might be the stock for you.

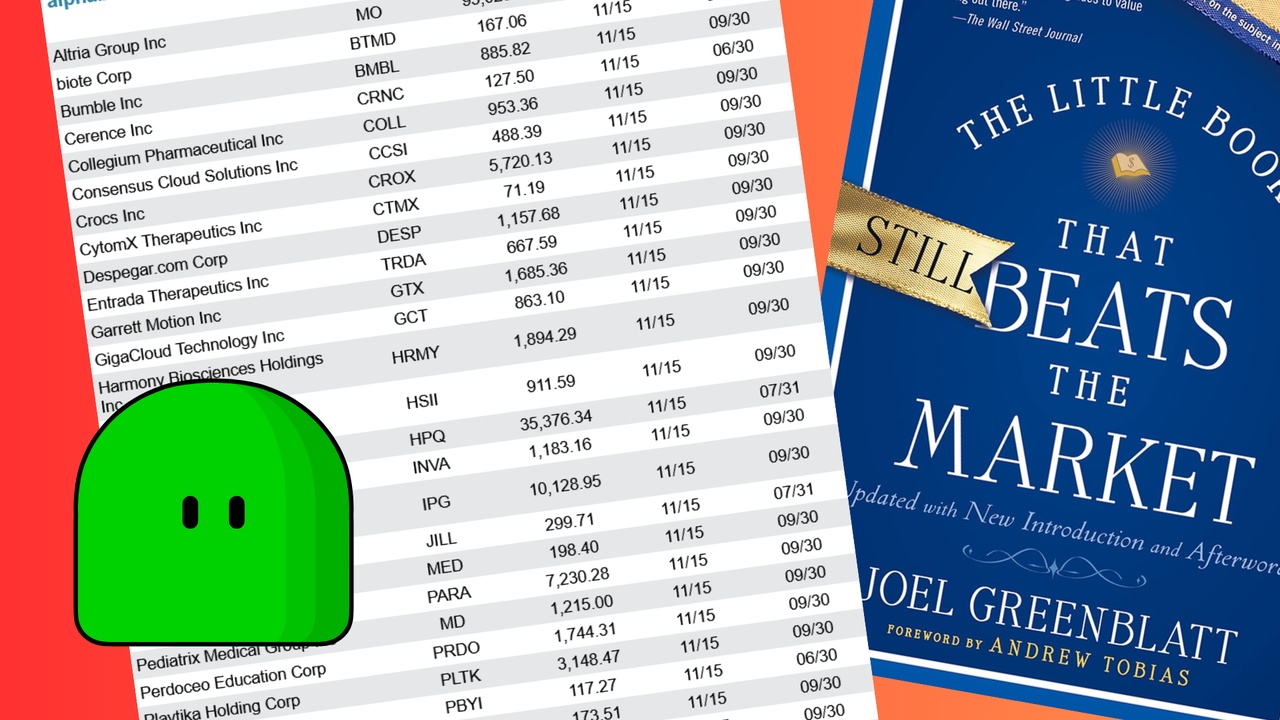

Magic Formula's list (24/11/2024)

#magicformula

#multibagger

#tenbagger

#joelgreenblatt

#greenblatt

What is your pick from this week Magic Formula list?

For all the Joel Greenblatt's Magic Formula enthusiast on this platform I think it will be fun to publish this week Magic Formula's list and get your take on the stocks in the list.

What stock would you pick and keep for 1 year? Why?

Magic Formula's list (17/11/2024)