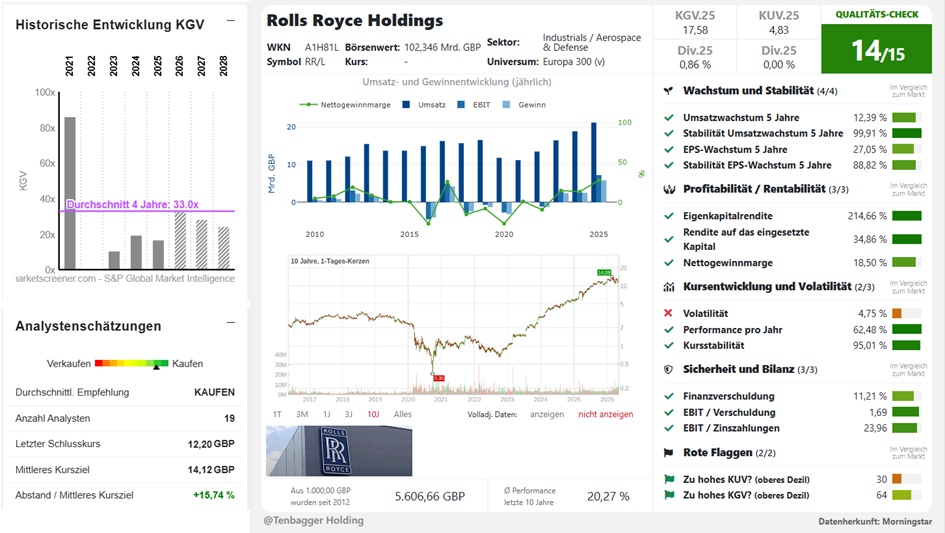

Here's the hot stuff from Rolls-Royce Holdings $RR. (+2,75 %)

(LSE: RR. / OTC: RYCEY) H1 2026 Earnings, fresh from London:

🚀 Turbines at Full Throttle & Record Cash Flow

Under CEO Tufan Erginbilgic, Rolls-Royce continues its epic turnaround unabated. The British engine and energy giant shattered analysts’ expectations in nearly every respect in the first half of 2026:

Revenue growth: Operations are booming—consolidated revenue rose, on a currency-adjusted basis, by +14% to GBP 9.92 billion (previous year: GBP 8.80 billion).

Flying Hours Booster (Civil Aerospace): Large engine flying hours reached 106% of the pre-COVID-19 level from 2019 —a massive catalyst for the high-margin spare parts and maintenance business (LTSA).

Cash Surge: The free cash flow soared by +38% to an incredible 1.60 billion GBP in the first half of the year. The company is simply printing money.

🔮 Profitability Surge & Record Margins

The radical cost and pricing adjustment strategy is having maximum impact—operating leverage is kicking in across all three core divisions:

Underlying Operating Profit: Climbed by a spectacular +40% to GBP 1.61 billion (previous year: 1.15 billion GBP).

Operating Margin: Reached a record level of 16.2% (compared to 13.1% in H1 2025).

Business Unit Strength:

Civil Aerospace: Operating profit climbed to GBP 1.02 billion (margin of 19.5%).

Defense: Profit rose to GBP 380 million (margin 14.8%, supported by global rearmament).

Power Systems: Record profit of GBP 245 million thanks to the boom in data centers and emergency power generators.

🤖 Significant upward revision of the full-year forecast & dividend comeback

With the engine running at full throttle, management is once again raising the bar significantly for the full year 2026:

Underlying Operating Profit (FY26): Now raised to GBP 3.1 to 3.3 billion (previously: GBP 2.7 to 2.9 billion).

Free Cash Flow (FY26): Revised upward to GBP 2.7 to 2.9 billion (previously: GBP 2.1 to 2.3 billion).

A Gift to Shareholders: As promised, the Group is paying the interim dividend as promised and is signaling a further increase in the payout ratio for the full year.

⚡ 💡 Jack’s take

What Tufan Erginbilgic is pulling off at Rolls-Royce is one of the most spectacular turnaround masterpieces in European industrial history! In a very short time, a company in dire need of restructuring has been transformed into a highly profitable cash cow.

The quality verdict: The moat in commercial aviation (a duopoly with GE in wide-body aircraft) combined with tailwinds from defense and data centers is massive. Although the stock has already had a massive run, Rolls-Royce is currently underpinning its valuation with rock-solid record figures. The absolute benchmark in the engine sector! ✈️🔋