Another month has passed, and it’s time once again to take a quick look into the engine room...

...actually, not much has changed in the big picture, except that after 38 months of consistent performance, the 40k mark has been broken, and so the final sprint of the first half has now begun...

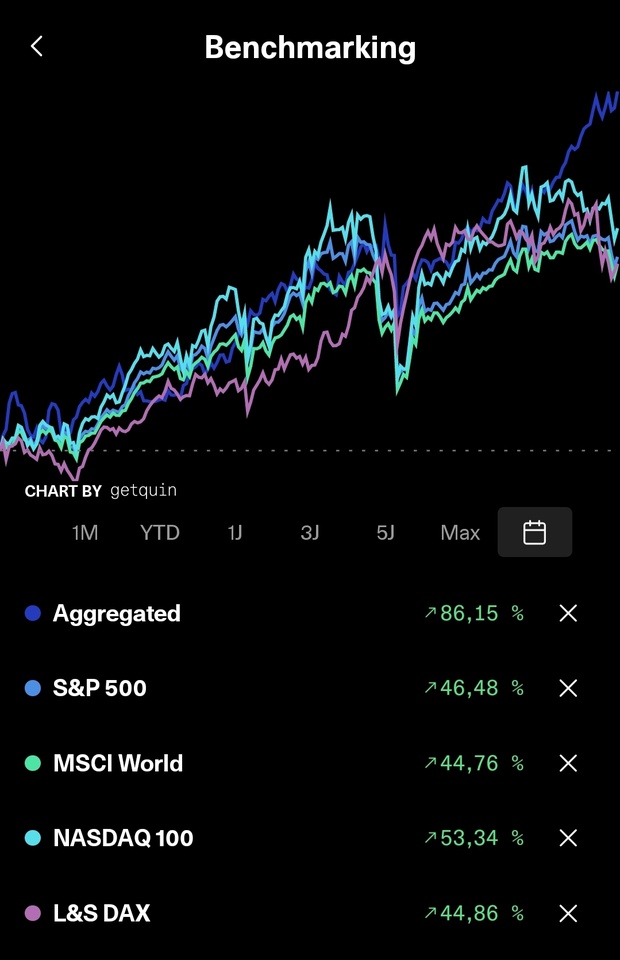

...it’s not a high-flyer portfolio, but so far it’s been a solid growth story, and as the saying goes, every little bit helps...

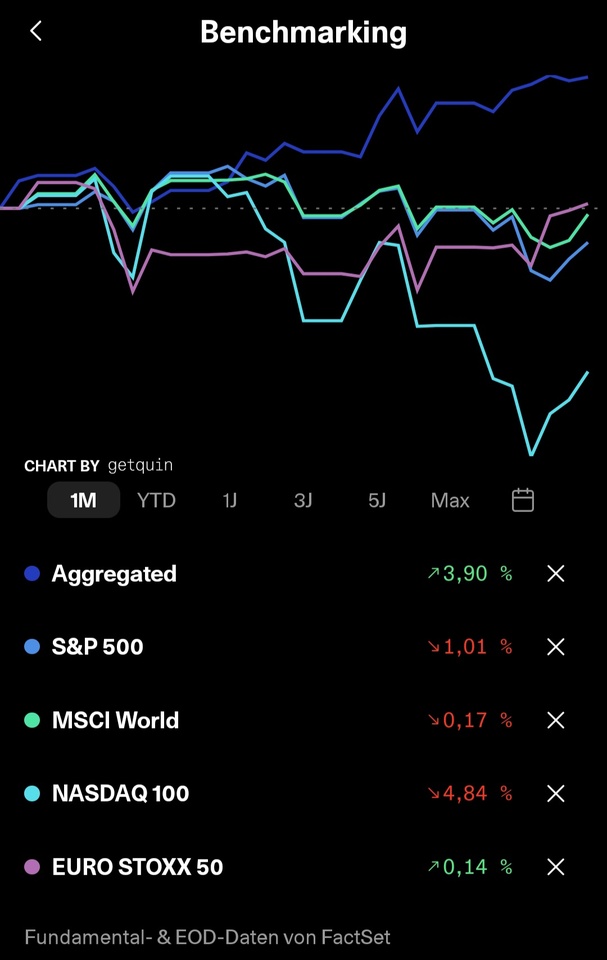

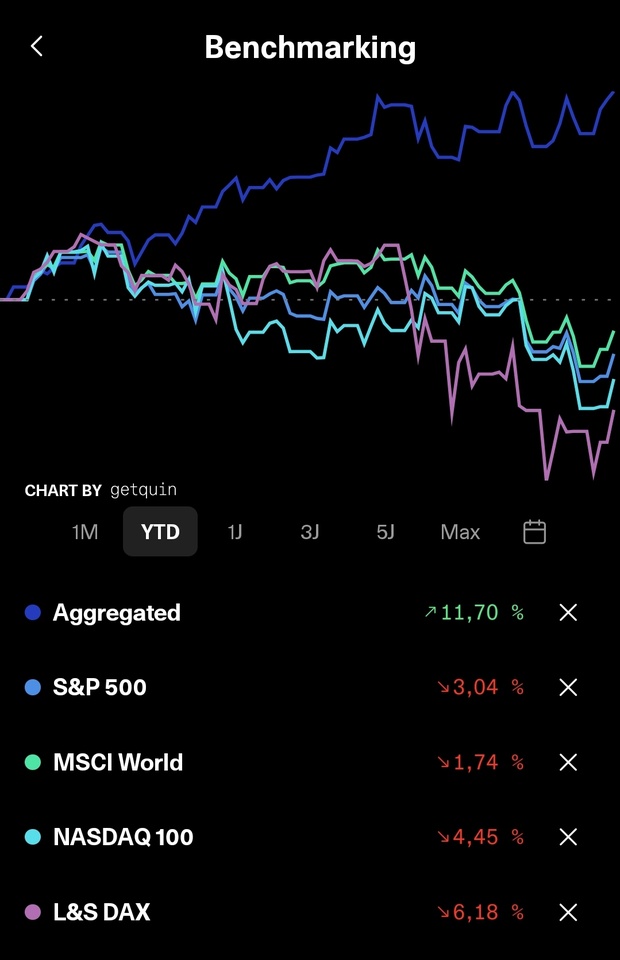

...which is why YTD hasn’t changed much either...

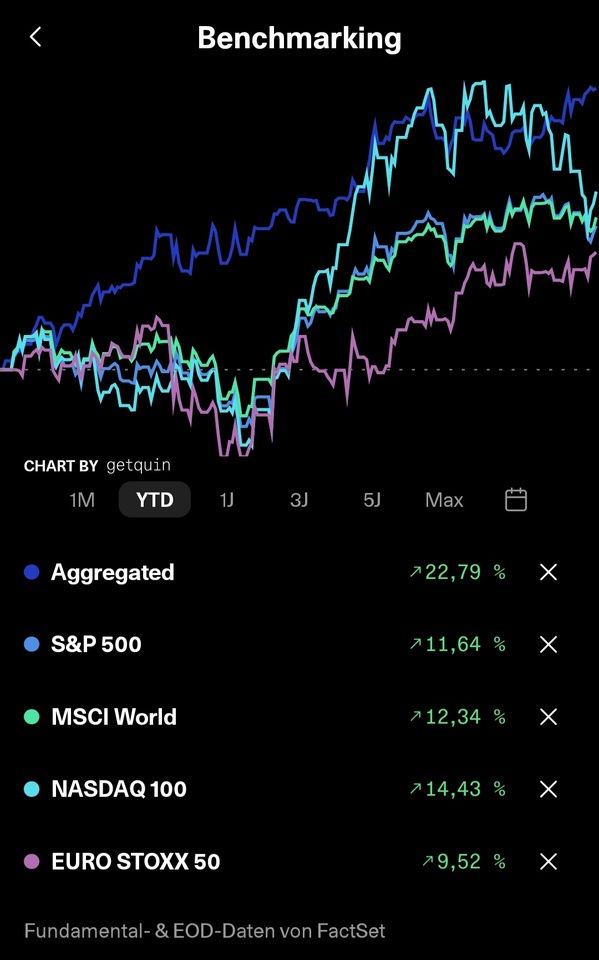

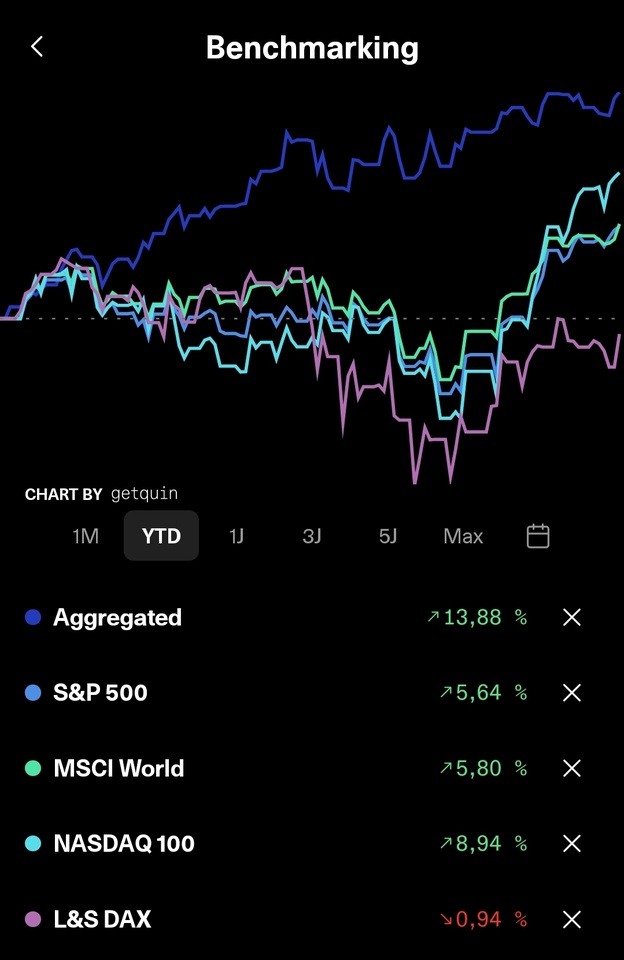

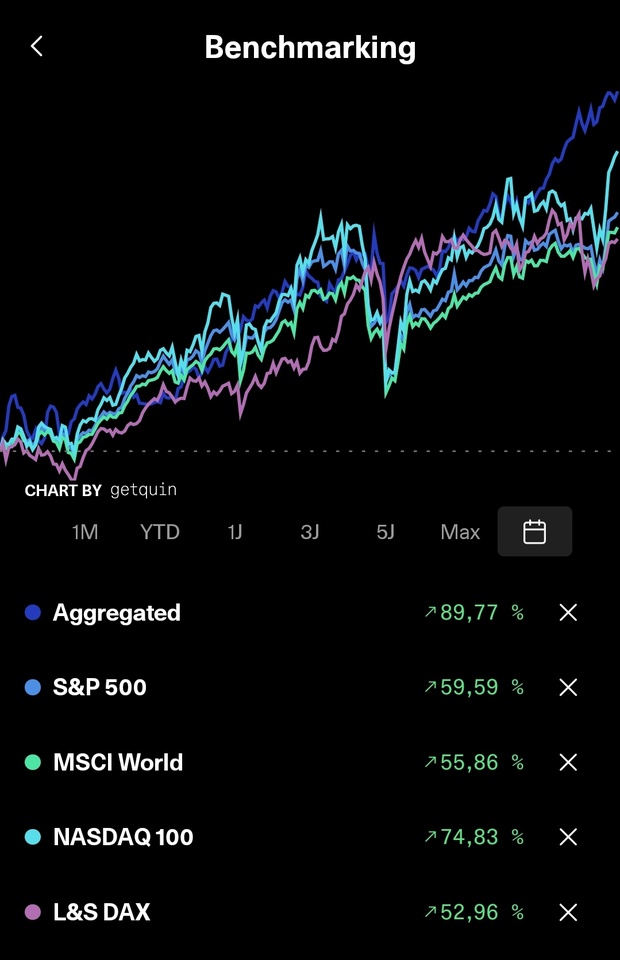

...nor has it since the very beginning...

...the structure, however, is a different story, and so there were a few changes to the portfolio this month...

》New Additions《

$WINC (-0,16 %) 244.01x

$AII (-3,07 %) 101x

》Exits《

$EVD (-2,7 %) 25x

》Top 3《

$HAUTO (+1,67 %) +24.42% (+122.67%)

$VAR (+2,03 %) +19.82% (+60.72%)

$DTE (+0,44 %) +10.61% (-1.53%)

》Flop 3《

$3750 (-1,03 %) -10.58% (+128.32%)

$ASWM (-1,11 %) -9.86% (+17.84%)

$YYYY (-0,59 %) -7.01% (-4.80%)

》Dividends《

This month, there were €252.24 in net dividends, representing a 12.24% increase year-over-year.

》CONCLUSION《

Everything’s business as usual, so we can relax and prepare for next Friday’s upcoming DATEV certification 👍🏻

I wish everyone continued success, and may dividends and growth be on our side 🫡