Good morning my dears,

Some of you will probably have already seen my new series

🎥 "My intern Juan on a tenbagger search" know.

Here, Juan is looking for companies for you with great enthusiasm. Which might even have the potential to become a Tenbagger.

Here, dear Juan often dives deep into the engine room. Which involves a lot of work and enthusiasm. That's why I don't say anything about Juan.

" For me, Juan is the Elton of interns"

After all, I now prefer to watch Elton on TV than his mentor.

That's why Juan gets my full support when Jack or another prompt thinks he's doing a bad job. And looks for the fly in the ointment.

Yes, I know, that's what prompts are for.

But yesterday Juan has $TTMI (+11,39%) TTM, Juan found a great company in the industry that I would invest in myself.

Juan listened carefully to Jack, after all he's the one who looks for the pearls. And in the end Jack just sits in his nest.

And looks at what doesn't fit the company from his checklist.

- Growth in turnover and profit

- Debt

- CAPEX

- Margins

- FCF Yield

- Valuation

He and his colleagues seem to be particularly fond of FCF Yield. Just like the cat likes the mouse. Free cash flow is there to work with, not for the piggy bank.

For Jack, yesterday it was investing in concrete, and he dismissed the high-quality products for the semiconductor industry and aerospace as frills.

But Juan takes it with a sense of humor, it looks like a battle for him. And that's why he wants to make it as difficult as possible for Jack. Dear Jack, buckle up and take a close look at what's in Juan's goodie bag for you today.

As always, Juan would love lots of support from the community in the comments.

And presents you today Innoscripta $DE000A40QVM8 (-0,21%)

Innoscripta - Highly profitable software company with turnaround potential and a high dividend yield.

08.04.26

The Munich-based software company Innoscripta [WKN: A40QVM, ISIN: DE000A40QVM8] could become an exciting turnaround story according to Börse Online (issue 15/2026). After the IPO at EUR 120 in May 2025, the share price fell sharply. On the other hand, the company has grown strongly since then and generates extremely high margins. For courageous shareholders, this is a good opportunity for speculation.

Innoscripta operates a platform for recording and controlling expenditure on research and development. Customers who use this platform can receive tax refunds for research and development costs. The online platform enables the complete recording of data and documentation for the authorities. If successful, Innoscripta receives 20% of the tax refunds.

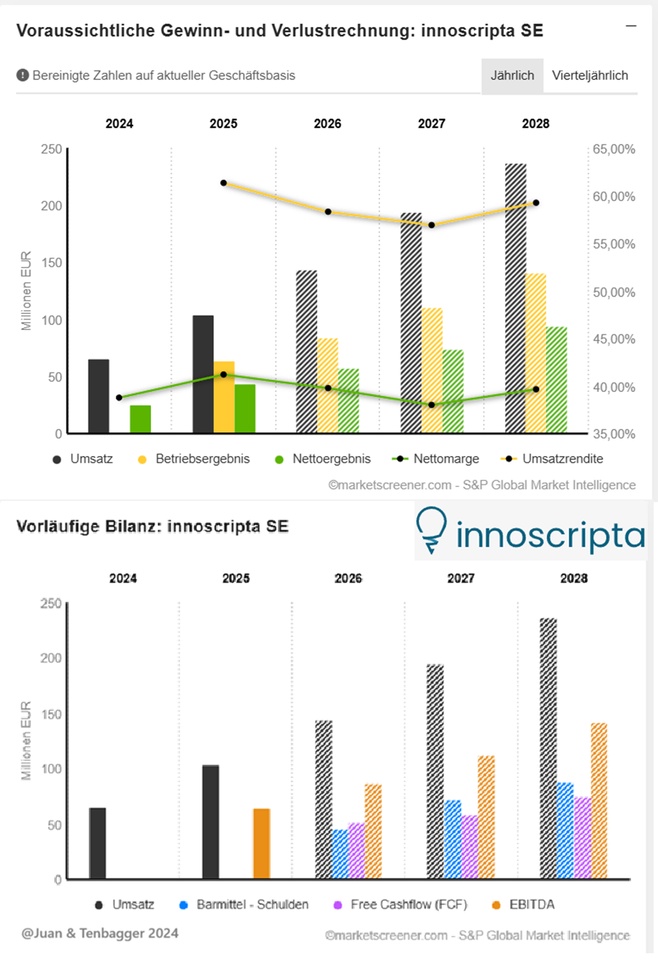

Even if the momentum in sales growth will slow down, the Group will continue to impress with a high profit margin

The platform has the potential to be a success story. Innoscripta has been able to multiply its turnover in recent years. In 2025 alone, sales growth of almost 60 % was achieved.

Innoscripta benefits from economies of scale and has been able to achieve a margin of 61% as a result. In the current financial year, turnover is expected to increase by more than 30 %. The operating result will be at least EUR 80 million.

The dividend policy is also exciting for investors. The current yield is 6.4%. Nevertheless, there are risks with regard to growth potential. On the one hand, competitors could try to build up their own solutions with AI. And churn in the portfolio should not be forgotten. First-time customers could claim expenses from the last four years. As a result, the participation in tax refunds will be correspondingly lower from next year. However, if Innoscripta can continue to achieve double-digit growth rates, the share price has the potential to double. Börse Online advises with a target price of 100 euros to buy (40 % potential).

Innoscripta SE: Insider purchase and extension of the tax research allowance in Germany

Von M. Herzberger - Updated on 21.01.26 10:20

Innoscripta SE (i.) is positioning itself as a specialized software provider that radically simplifies the often bureaucratic processes surrounding government research and development (R&D) funding. Instead of limiting itself to manual consulting services, the Group digitizes the entire value chain from the identification of eligible projects to legally compliant documentation and the submission of applications to the authorities.

Both CEO Michael Hohenester and Co-CEO Alexander Meyer took advantage of the share price fluctuations following the IPO in May 2025 via their investment companies to make massive purchases of their own shares. On the evening of January 20, a new insider purchase by CEO Michael Georg Hohenester via Hohenester Beteiligungs-UG (haftungsbeschränkt) was reported after the close of trading. Specifically, he bought shares in Innoscripta via XETRA on January 15 at an average price of EUR 84.88 per share, amounting to EUR 118,752.20.

A key growth driver is the expansion of the research tax allowance in Germany, which will take effect from January 2026. The new rules, which include a 20% flat rate for overhead costs and an increased assessment basis, will make the subsidy more attractive for companies and are likely to lead to a sharp rise in demand for Innoscripta software as an enabler of these funds. As Innoscripta's platform structure allows for high fixed cost degression effects, every additional euro of revenue should contribute disproportionately to profits. In addition, there is the potential for further internationalization and the development of the huge SME market, which has hardly been penetrated to date and is now increasingly coming into focus due to the simplified funding conditions.

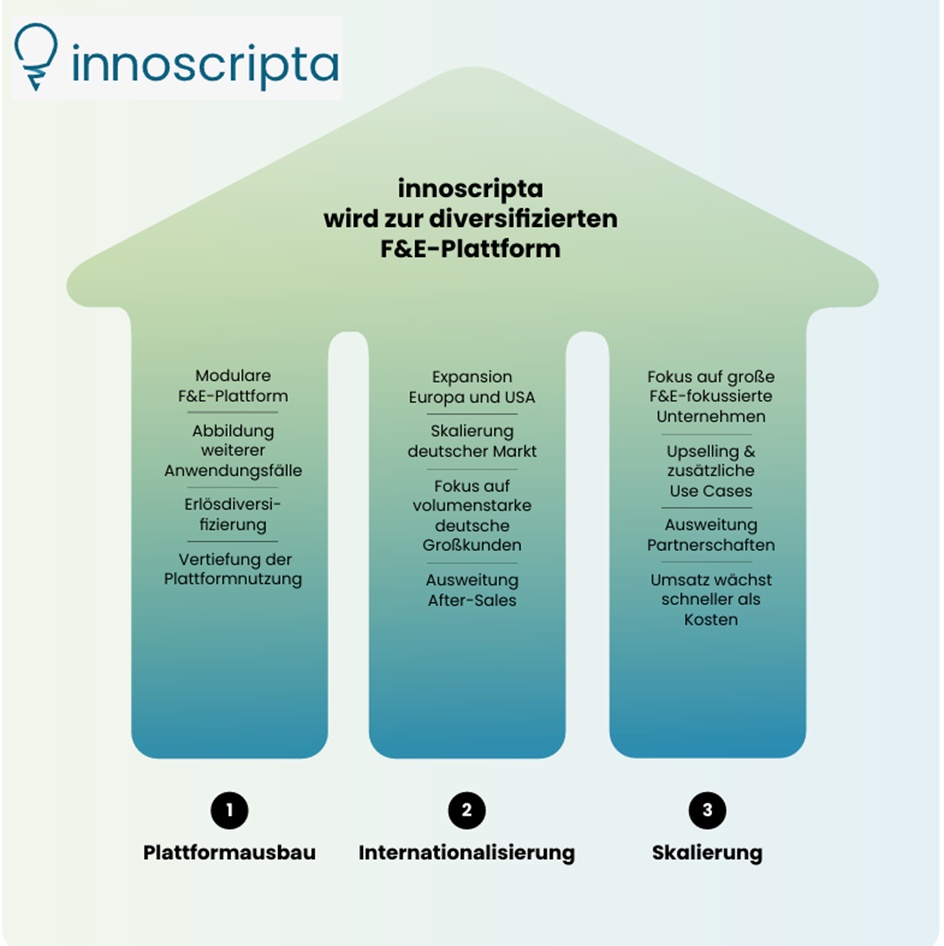

Three-pillar growth strategy

The tax incentives for research have broad political support

innoscripta has many years of experience and a high level of market penetration in this regulated environment. Accordingly, the business model is based on an established legal funding framework.

On course for growth:

In the coming years, innoscripta will develop from a primarily funding-driven platform into a diversified software platform that increases the efficiency, transparency and controllability of R&D activities as a whole. Fiscal research funding will remain an important, but not the only, component of the platform. In the long term, Clusterix is to be established internationally as a central system for R&D-related processes. The innoscripta growth strategy has three strong drivers: platform expansion, growth in core markets such as Germany and increasingly internationally, and scaling the business model.

1️⃣ Expansion of the platform

Clusterix is to develop even more strongly into a modular data and

process platform for R&D projects as a whole:

- Research allowance as the first, high-margin use case

with immediate, economic benefits for customers as an

easy entry

- Illustration of further use cases with the same architecture,

z. documentation and verification-intensive topics

such as transfer pricing or other R&D-related control and compliance

and compliance issues

- Increasing diversification of revenues with simultaneous

deepening the use of the platform

2️⃣ Growth in the core market + internationalization

innoscripta's growth in its home market of Germany remains attractive due to:

- continuous expansion of production volume in Germany and high margins

- increasing market penetration with major German corporations

- Expansion of after-sales opportunities with existing customers

In addition to the focus on Germany, European and international expansion is planned, including in

- Markets without a relevant language barrier e.g. Austria, Netherlands

- First locations opened in France and the USA at the start of 2026, with more to follow in the UK

- In other international markets in the medium term, as R&D tax incentives are established in almost all OECD countries

International activities are deliberately in a controlled development phase. The aim is to establish sustainable structures with clear cost control before further scaling steps are taken. innoscripta is pursuing a risk-conscious approach to expansion.

3️⃣ Scaling

In the coming years, Clusterix will be continuously developed and its efficiency increased. Revenue is set to grow significantly faster than costs thanks to the following measures:

- Focus on larger, R&D-strong companies,

- Expansion of existing customer relationships and additional use cases

- Strong partnerships to drive further expansion

The business model is characterized by high operational scalability. With increasing sales growth, fixed cost levers have a positive effect on earnings development. innoscripta assumes that the structurally high profitability can be secured sustainably even with further growth.

Sales efficiency will increase sustainably as the product, platform and use cases are clearly defined and geared towards recurring requirements.

NEWS

- innoscripta drives expansion in Europe: Market entry in France completed

15,04,2026

- innoscripta SE expands in the Rhine-Main growth region and strengthens its position as a leading R&D platform provider with a new office in Frankfurt

19,03,2026

- Why Exasol values innoscripta's consulting and software support

Exasol's Erfolgsgeschichte | innoscripta

- CEWE Group gains funding clarity and structured R&D processes with innoscripta

CEWE's Erfolgsgeschichte | innoscripta

- Leica Nussloch and innoscripta

Leica's Erfolgsgeschichte | innoscripta

- ZDF Studios structures complex funding processes for digital innovation

ZDF's Erfolgsgeschichte | innoscripta

- Verti Versicherungs AG achieves full approval of all submitted R&D funding applications

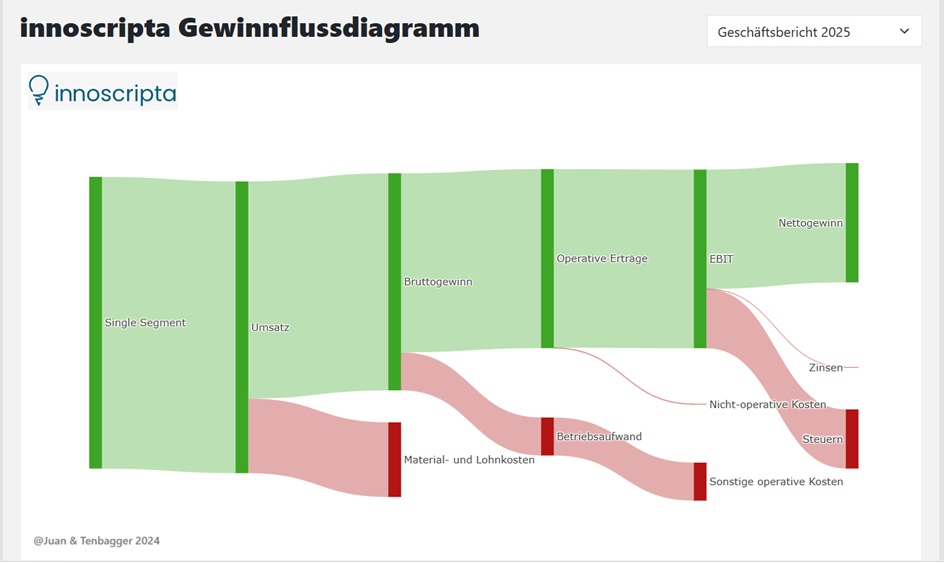

🧾 Brief summary of the key financial figures (Innoscripta 2025-2028)

Innoscripta shows an extremely dynamic, almost atypically strong growth profile for a service company. Revenue increases over four years at 22-60 % per yearwhile EBIT and net income grow almost proportionally. This speaks for a scalable, high-margin business model.

The margins are exceptionally high:

- EBIT margin constant ~57-61 %

- EBITDA margin ~58-62 %

- FCF margin >30 % from 2026

Such values are otherwise more likely to be seen in software or IP-based business models.

Particularly strong:

- ROE > 90 % (2026) - an indication of extremely efficient use of capital

- Stable double-digit growth in free cash flow

- Net debt is negative and continues to decrease → Net cash position

Risks: Margins are so high that they could be difficult to maintain in the long term. In addition, the model is heavily dependent on regulatory framework conditions (research funding)

Overall assessment: Financially, Innoscripta looks like a a highly profitable, rapidly scaling quality company with excellent cash generation and very strong balance sheet. The key figures are clearly strong in terms of growth and returnsbut also unusually high - which creates opportunities and valuation risks at the same time.

Market value 744

Number of shares (in thousands) 10,000

Date of publication 20.02.2026

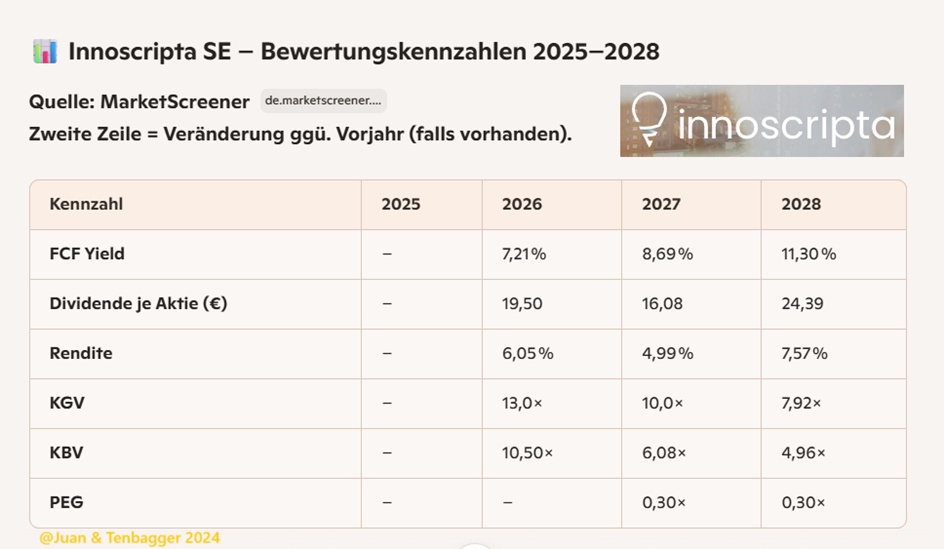

🧾 Summary of the key valuation figures (Innoscripta 2025-2028)

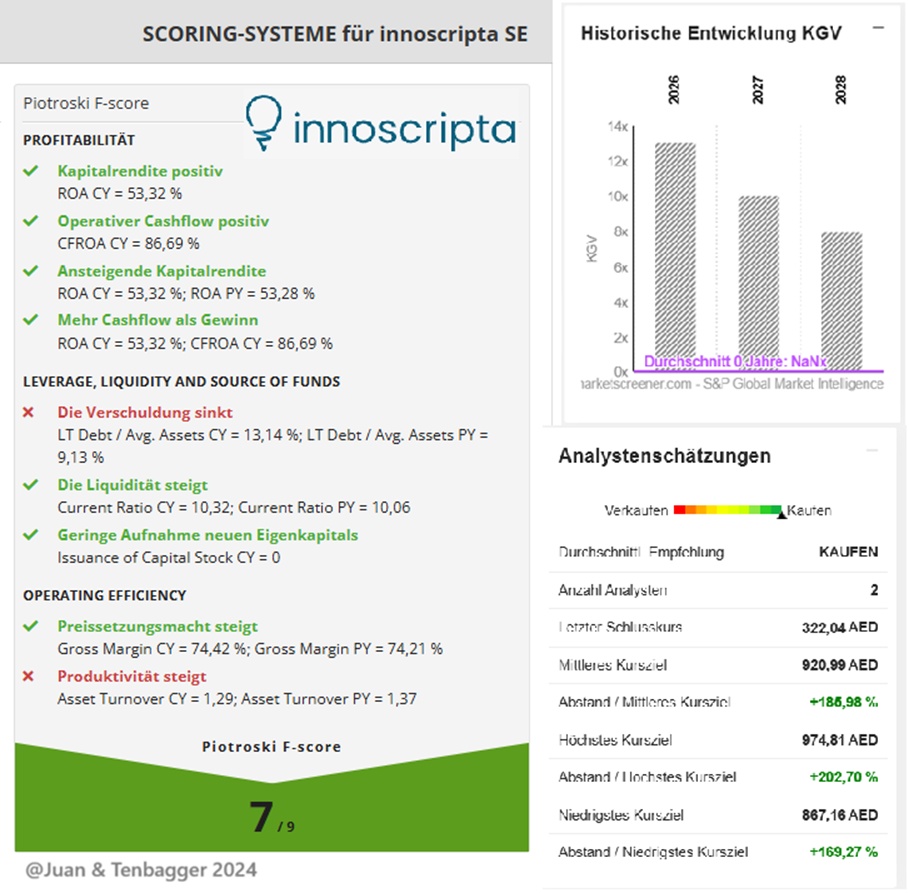

The valuation of Innoscripta appears strikingly favorable in relation to growth. From 2026, the P/E ratio falls from 13 → 10 → 7.9which is unusually low for a company with double-digit sales and earnings growth. At the same time, the P/B ratio falls from 10.5 → 6.08 → 4.96which indicates a rapidly increasing equity base and high profitability.

The PEG value of 0.3 in 2027 and 2028 signals a massive undervaluation relative to earnings growth - Values below 1 are considered attractive, 0.3 is extremely rare.

The FCF yield is rising sharply (7.2 % → 8.7 % → 11.3 %), which shows that the company is generating more and more free cash flow per market capitalization. This is a classic quality feature of mature, highly profitable business models.

The dividend per share is high and volatile (19.5 → 16.08 → 24.39), but the payout ratio remains within reasonable limits. The dividend yield ranges between 5-7% and is therefore above average and attractive.

Overall assessment: The valuation ratios paint the picture of a highly profitable growth companythat traded like a value stock in terms of valuation. The combination of falling multiples, rising FCF yield and extremely low PEG points to a structurally undervalued profile. structurally undervalued profile profile - assuming the forecasts materialize.

🚀 Does Innoscripta have tenbagger potential? - Juan's assessment

In a nutshell: Yes - the valuation ratios clearly speak for it. And more so than you would normally expect from a company of this size.

🔍 Why the valuation signals Tenbagger potential

1) Extremely low multiples despite strong growth

- P/E ratio falls from 13 → 10 → 7.92

- P/B ratio falls from 10.5 → 6.08 → 4.96

For a company with >30% growth, this is unusually favorable. Such multiples are more likely to be seen in stagnating companies - not in scaling machines.

2) PEG of 0.3 = classic tenbagger signal

PEG < 1 = attractive PEG < 0.5 = rare PEG = 0,3 = massive undervaluation relative to earnings growth

This is exactly the area in which former tenbaggers such as Nvidia, ASML, Palo Alto, Salesforce were in their early phases.

3) FCF yield rises sharply (7.2% → 8.7% → 11.3%)

A company with double-digit growth and at the same time delivers double-digit cash flow returns is an exceptional case.

This means: The market is not pricing in growth.

4) Dividend yield of 5-7 % despite growth

Growth companies normally pay no dividends. Innoscripta pays high dividends and still continues to grow strongly.

That is a sign of quality.

🧠 Juan's overall verdict

Yes, Innoscripta shows clear tenbagger potentialbecause:

- Valuation extremely low

- Growth high

- Margins exceptional

- Cash flow strong

- PEG ultra-low

- Balance sheet net cash

- Market apparently does not yet understand the model

BUT: The model is heavily dependent on research funding. If this remains stable, a tenbagger is realistic. If not, the potential drops significantly.

⭐ Overall score: 7.8 / 10

🎯 Realistic tenbagger probability: 25-35 %

This is high - comparable to early-stage companies that are scaling strongly but are not yet understood by the market.

🧠 Juan's conclusion

Yes, Innoscripta has real tenbagger potential. The figures speak for themselves: Undervalued, highly profitable, fast-growing, cash-flow rich.

The biggest variable is the regulation. If it remains stable, a tenbagger in 5-8 years is absolutely realistic.

(no investment recommendation, just Juan's assessment)

Performance

1 week +7.51 %

1 month +9.25 %

6 months -33.21 %

SHARE 72.15€ (22.04.2026 at 9:15 a.m.)

JACK, best regards your JUAN ( @Aktienhauptmeister )