A shock report from HSBC $HSBA (-0,79%) questions the financial viability of OpenAI and its gigantic cloud obligations into question.

Despite optimistic growth scenarios, the revenues are nowhere near sufficient to cover the massive data center costs.

》Free cash flow not in sight《

OpenAI, the pioneer behind ChatGPT and the catalyst of the current AI boom, is facing a potentially huge financial problem. A recent analysis by investment bank HSBC comes to an alarming conclusion: the contractually agreed obligations for computing power far exceed the forecast revenue - even if extremely optimistic assumptions are made.

》The bill《

36 gigawatts and $620 billion in rent!

In order to operate the enormous AI models and secure future growth, OpenAI has concluded massive contracts and cooperations with cloud providers and companies from the AI environment.

From chip manufacturer Nvidia$NVDA (+0,16%), Amazon $AMZN (+0,67%)Oracle$ORCL (+4,71%) or Meta$META (+1,28%) - OpenAI is associated with virtually every big name in the industry.

Some refer to this as a Ponzi scheme. In recent months, reports of contracts and numerous declarations of intent have boosted the shares of many players.

Anyone who announced a contract or cooperation with OpenAI often saw their shares rise by double-digit percentages in a single day. Investors were in a frenzy.

However, HSBC sees the financing of these deals as virtually impossible. An overview:

》Contractual obligations《

According to estimates, OpenAI has committed up to 250 billion US dollars in cloud compute with Microsoft and 38 billion US dollars with Amazon.

》The hunger for power《

The total contractually agreed computing power amounts to an astronomical 36 gigawatts. Some data centers in the USA are already at a standstill because they cannot get the required connection to the power grid, see here:.

》The cost explosion《

Based on a total value deal of up to USD 1.8 trillion, HSBC estimates that OpenAI is heading for annual rental payments for data centers of around USD 620 billion.

》The gigantic financing gap《

HSBC has set OpenAI's revenues up to 2030 (and beyond) against these exploding costs. The result is sobering:

》Item:Cumulative total to 2030《

● Cumulative rental costs (data centers) $792 billion

● Cumulative free cash flow (HSBC estimate) $282 billion

● Additional financing (capital injections, loans, etc.) $67 billion

● Total funds available $349 billion

● Shortfall (financing gap) -$443 billion

The HSBC calculation results in a cumulative funding gap of $207 billion by 2030, plus a recommended safety buffer of $10 billion.

》The optimistic assumptions that are still not enough《

The remarkable thing about the HSBC analysis is that this massive gap arises despite the assumption of best-case scenarios:

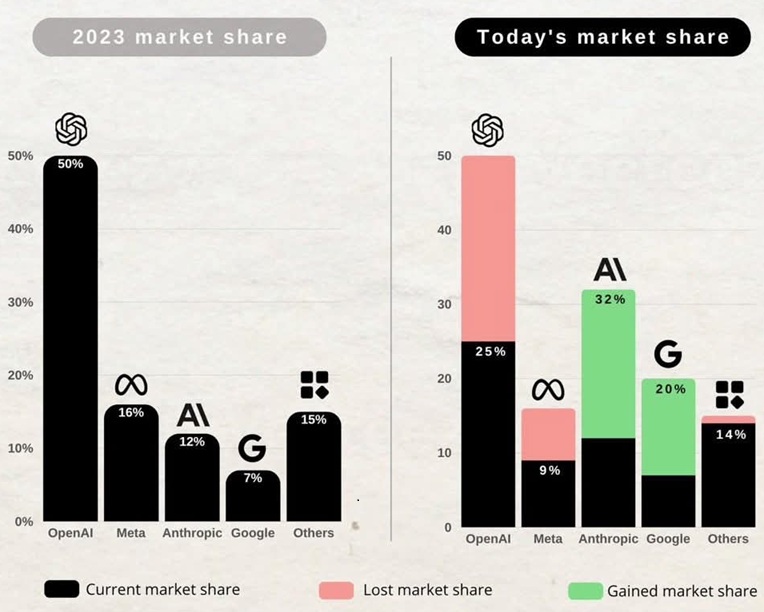

1. massive user base: OpenAI reaches 3 billion users by 2030 (44% of the global adult population outside China). Our take: impossible, as the competition from Google $GOOGL (+1,18%) (Gemini) or Anthropic has been catching up since 2024, as the following graph (estimate) shows:

2. high paying ratio: 10 percent of these users will become paying subscribers, but currently it is only around 5 percent.

3. advertising market share: OpenAI captures two percent of the total digital advertising market.

4. enterprise AI: The enterprise AI sector generates 386 billion US dollars annually.

Even if all these very ambitious assumptions are true, the company will not be able to fulfill its commitments.

There has long been speculation about an IPO of OpenAI, with a valuation of between 500 billion and 1 trillion US dollars being floated.

》Conclusion《

The HSBC study suggests that OpenAI may have to "back away from data center commitments" and hope that the major partners will show "flexibility".

This is a polite way of saying that the current business model is not sustainable in this form and the contracts may need to be ignored to avert a liquidity crisis.

We would even say: this is impossible. It all smells like a bubble that will burst at some point.

And it is practically impossible to finance such amounts.

The question remains whether these data centers on this scale are even necessary.

Mistral AI, the only European player, for example, and the four Chinese providers, expect far less demand.

Of course, there are also those who claim that MICROSOFT, which has close ties to OpenAI and is a major shareholder, is snapping up the fillet pieces of the company and leaving the rest to die a miserable death.