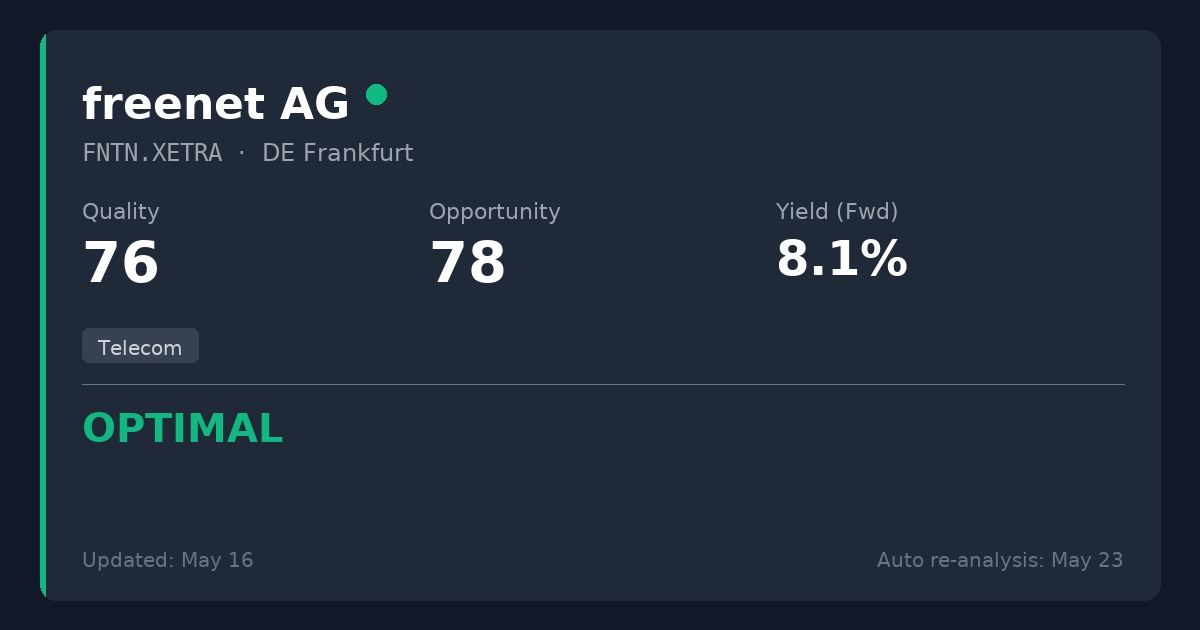

and it's not me. $FNTN (-0,71%)

Why is that? Let's take a look at that.

freenet AG is a holding company that offers telecommunications services. The company is divided into two central business divisions: Mobile Communications and TV and Media.

In the Mobile Communications segment, freenet bundles its traditional communications services. These include, in particular, mobile phone tariffs and, increasingly, internet-based applications such as digital lifestyle products.

The TV & Media segment comprises IPTV-related services. These include planning, project management, development, operation and marketing of broadcasting-related solutions for business customers in the radio and media sector.

The company was founded on March 2, 2007.

Management: Freenet has appointed Robin Harries as its new CEO with effect from August 1, 2025. He has many years of experience in the telecommunications and digital industry. At the same time, the Management Board structure was reduced to two members. Ingo Arnold remains CFO and his appointment has been extended. This indicates continuity and clearly defined responsibilities.

Strategy: The management is pursuing a so-called digital lifestyle strategy. Specific financial targets have been formulated for 2025 as well as a medium-term ambition to significantly increase EBITDA by 2028.

Capital allocation: In 2024, freenet achieved a record level of EBITDA and free cash flow. A record dividend of €1.97 per share was approved at the 2025 Annual General Meeting. In addition, the Management Board has launched a share buyback program with a volume of up to €100 million. Both of these factors indicate a high level of cash generation and an active dividend policy.

Freenet positions itself as a provider of digital lifestyle solutions. The core business consists of network-independent mobile services with its own brands and tariffs. This is supplemented by a growing TV and IPTV business, for example with freenet TV and waipu.tv. Revenue is primarily generated from subscriptions, device margins and additional services as well as from media offerings and service packages.

Freenet combines its own product design and brand management with a broad-based sales organization. This includes its own stores, the electronics trade and online channels. At the same time, the company relies on strong customer management and long-term customer relationships. Partnerships with network operators, device manufacturers and media providers reduce the need for in-house infrastructure and allow the company to focus on customer acquisition, cross-selling and stable, recurring revenues.

Freenet benefits from a network-independent business model in mobile communications and from a growing TV and streaming offering. The combination of direct sales and partner channels supports stable revenues, customer retention and additional sales opportunities. The expansion of IPTV services and the positioning as a digital lifestyle provider open up further growth potential.

Risks: The German telecommunications market is highly competitive, which can lead to price pressure. In addition, regulatory decisions, for example on network access policy or the allocation of frequencies, can affect margins and growth. Other risks include the strong dependence on the domestic market as well as technological changes and the associated investment requirements.

Sounds good, why am I not buying?

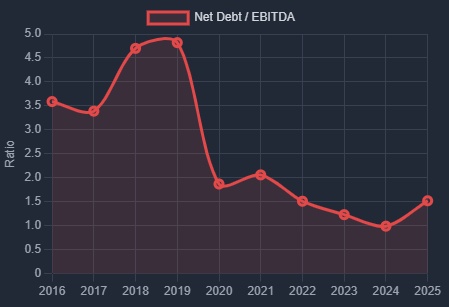

Quite simply, I don't like the dividend payout ratio...

I'm not as optimistic about Freenet as others are (even though I'm a Waipu fan myself ;))

With charts etc. and better structured... here: I'm not as optimistic about Freenet as others are (even though I'm a Waipu fan myself ;)) https://steady.page/de/finanzen-anders/posts/e7e8e6a1-3006-4173-91d7-283f094cb32b

This week I will still $XYL (-2,09%) and $AWK (-1,62%) this week. And maybe I still have time for $9988 (-1,48%)