$SIVE (-8.46%) Not sure if it was the best bet but my guts tell me it touched a hard bottom.

- Markets

- Stocks

- Sivers Semicondu

- Forum Discussion

Sivers Semicondu

Stock

Stock

ISIN: SE0003917798

Ticker: SIVE

SE0003917798

SIVE

Price

Discussion about SIVE

Posts

15

2Wk·

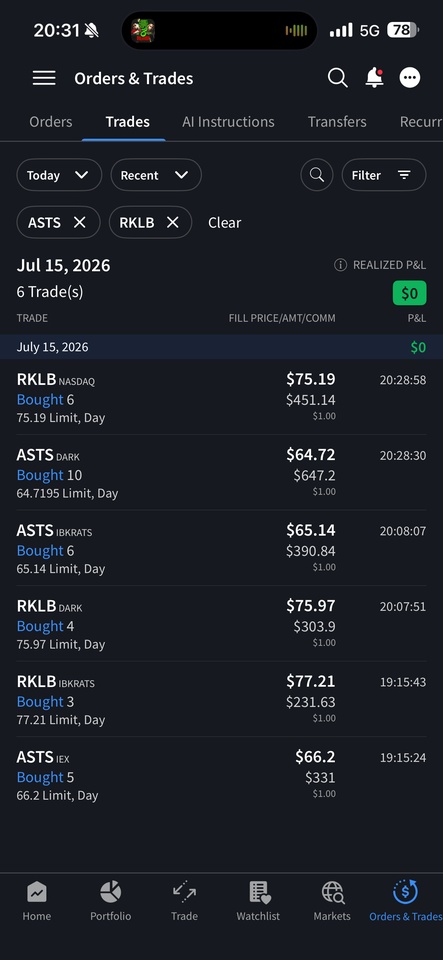

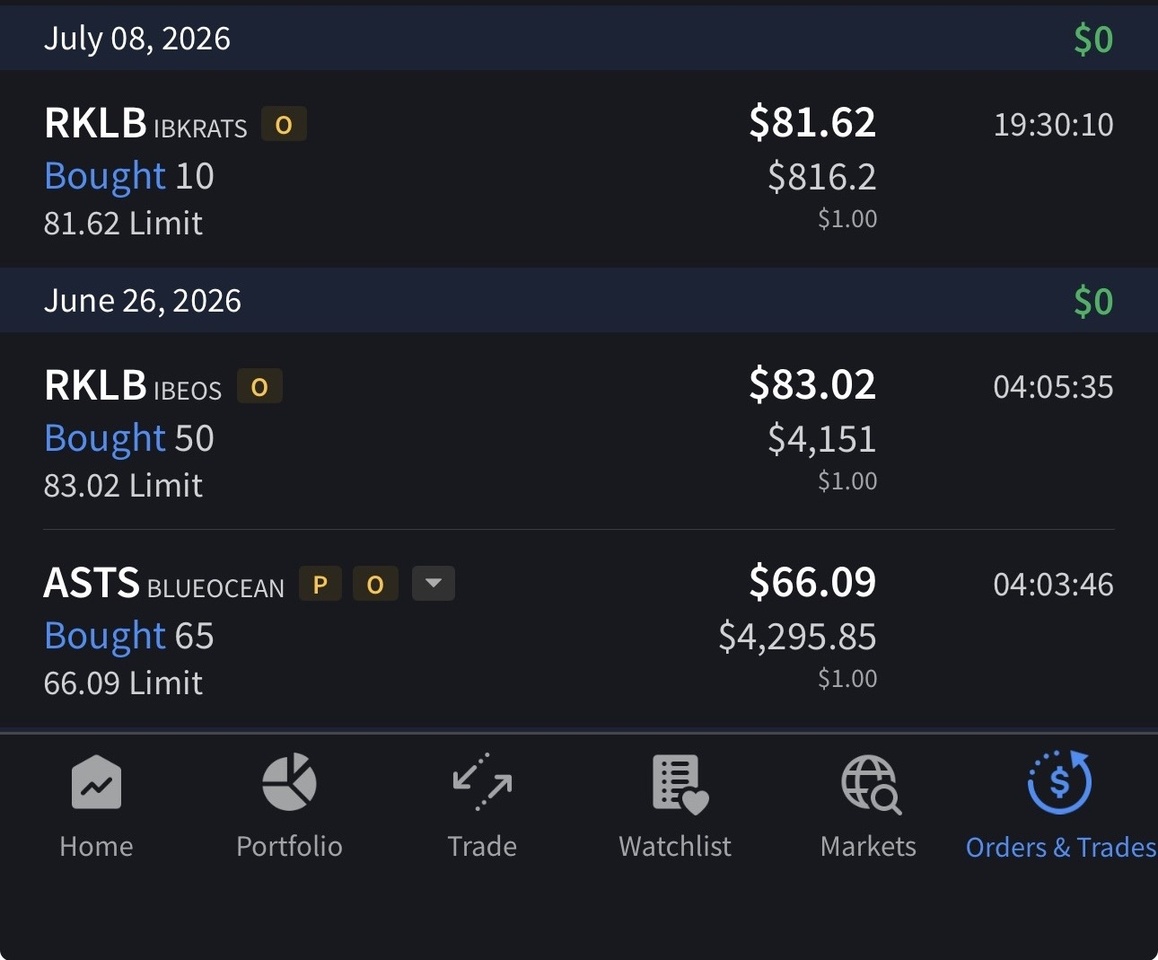

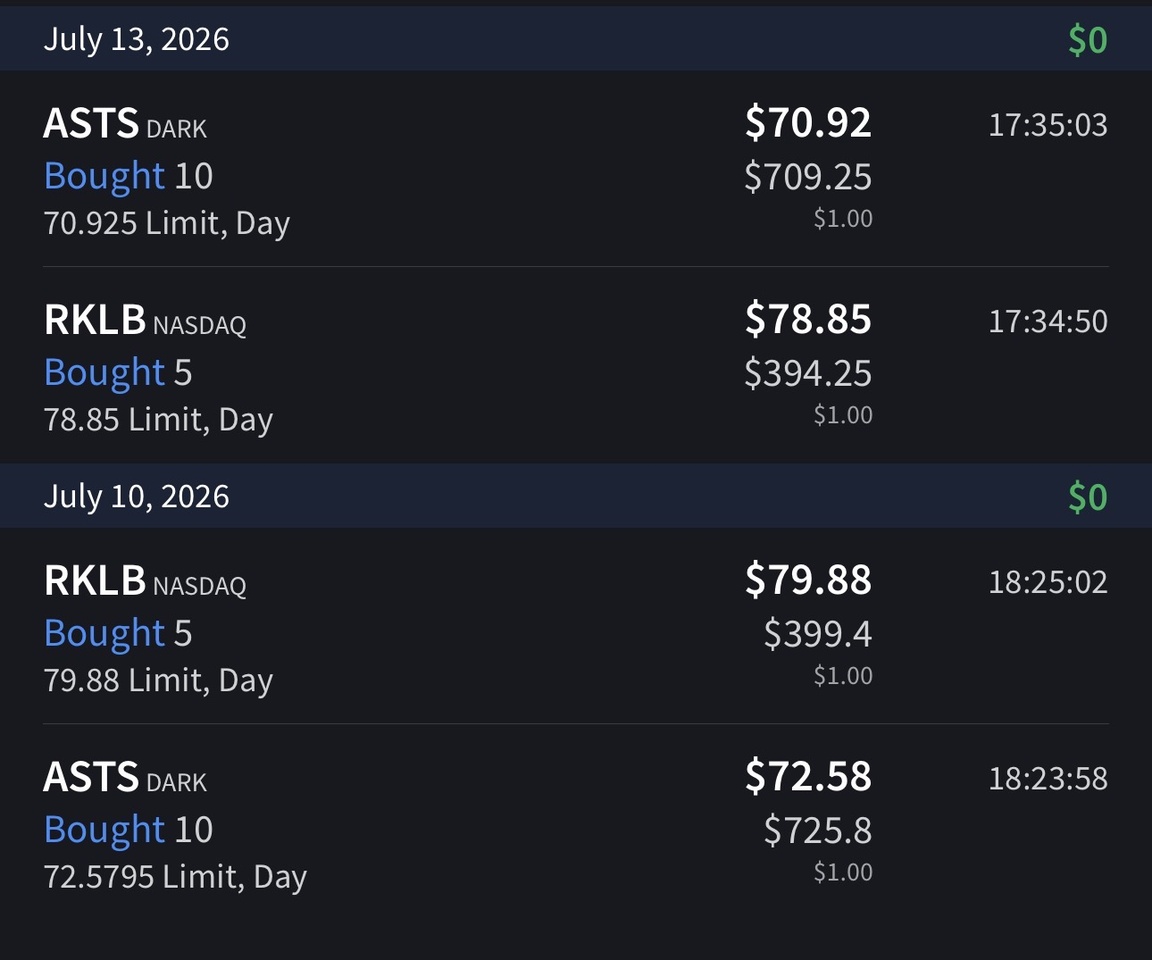

Accumulation continues… RKLB ASTS

Im building a very high risk/high growth portfolio, im very aware of that. But I’m young, have a very long way to go and I can stomach volatility. I’m betting on two of the most explosive, capital-expensive trends of the decade: space economy and photonics/semis.

This portfolio is being built to capture multibagger asymmetric returns. However, the coming months won’t be easy to stomach, having 5% to 10% days in the portfolio.

My bull case scenario: $100K to $120K in the coming years without further deposits

My bear case scenario: $10K to $25K

I will never be content with 8% a year returns, I’m here to make gains that can change my life. If it does not play out, I still have a family, a job, a home and a healthy life.

$RKLB (-10.41%)

$ASTS (-8%)

$AAOI (-15.94%)

$FLY (-7.7%)

$SIVE (-8.46%)

88

2 Comments

Go for it and keep us posted, I'm not that young so I need a bit more stability, I just allocate around 5% to growth drivers similar as that.

•

22

•2Wk·

Sivers Semiconductors

The waiting is finally over, decided to get back in on $SIVE (-8.46%) , down almost 65% from its ATH.

Today’s price action suggests momentum shifting from semis to mag7, but I rather much being a contrarian and position myself accordingly. I don’t expect a quick turnaround, I’ll buy more if it dips. Also, continuing to add more $AAOI (-15.94%) , planning to increase even more my stake in the company if it goes below $100. I expect them to crush earnings coming early August.

99

3 Comments

2Wk

My prediction is, that you will be able to collect $AAOI around 60$. Let’s see :)

•

11

•

1Mon·

That's how fast it can happen!

Over $SIVE (-8.46%) the past few days, you can see just how quickly prices can move with such rocket-like gains. I became aware of the company through several posts by our good friend, the Next Limits Wiki operator @ScaleLimits . I find the business model exciting, but after a gain of over 3,000% in just one year (congratulations again to @ScaleLimits for getting in early and, more importantly, for locking in profits), I decided to sit this one out for now. Now, the annual performance has dropped to “just” 1,300% within a few days. If the price reaches €4 or below, it might be worth considering getting back in. We’ll see.

1616

17 Comments

Thank you. I took profits on a large portion of my Sivers holdings some time ago, both in my personal portfolio and on Wikifolio. That’s why I can watch the current correction with a sense of calm.

My fundamental assessment hasn’t changed. I still find the story exciting. The next two years will be decisive.

At the same time, I view Sivers as one of the more speculative stocks within the photonics sector. This distinguishes the company, for example, from an established player like Coherent.

For now, I therefore see no reason to trade and will remain invested for the time being.

My fundamental assessment hasn’t changed. I still find the story exciting. The next two years will be decisive.

At the same time, I view Sivers as one of the more speculative stocks within the photonics sector. This distinguishes the company, for example, from an established player like Coherent.

For now, I therefore see no reason to trade and will remain invested for the time being.

•

1010

•

1Mon·

Do we ever make money? 💸

I’ve seen various people wondering if we ever make money considering our, sometimes sudden and repetitive moves, so here’s a screenshot montage of a part of our portfolio from 3 days ago.

These screenshots alone show cumulative profits of ~$214,021 and cumulative losses of ~$29,239.

This is not to flex, brag or anything, this is to provide context. We’re a team, and when there’s a concern that is raised about an asset, or a suggestion, we have to acknowledge it and act accordingly. We have no problem changing parts of the portfolio, readjusting positions and strategies or selling/buying assets in a short period of time. The whole organization is built for this.

55

1Mon·

Update on my portfolio

Last week, I decided to reduce the size of some positions in my portfolio in order to invest more in the current AI boom.

This involved 35 $BRK.B (-1.09%) and 350 $SHEL (+1.85%) shares were sold from my portfolio.

The following additions were made:

- $SIVE (-8.46%) 1,500

- $AAOI (-15.94%) 50

- $XFAB (-0.9%) 400

- $SHT B (+8.97%) 750

I didn’t quite time the entries perfectly in some cases, but let’s see what happens over the next few months and in 2027/2028. I’m curious to see how it goes.

In addition, the following stocks are on my shortlist for future purchases:

Have a nice evening, everyone!

66

6 Comments

I think the Switch is a little too aggressive. Good luck anyway 💯

•

99

•1Mon·

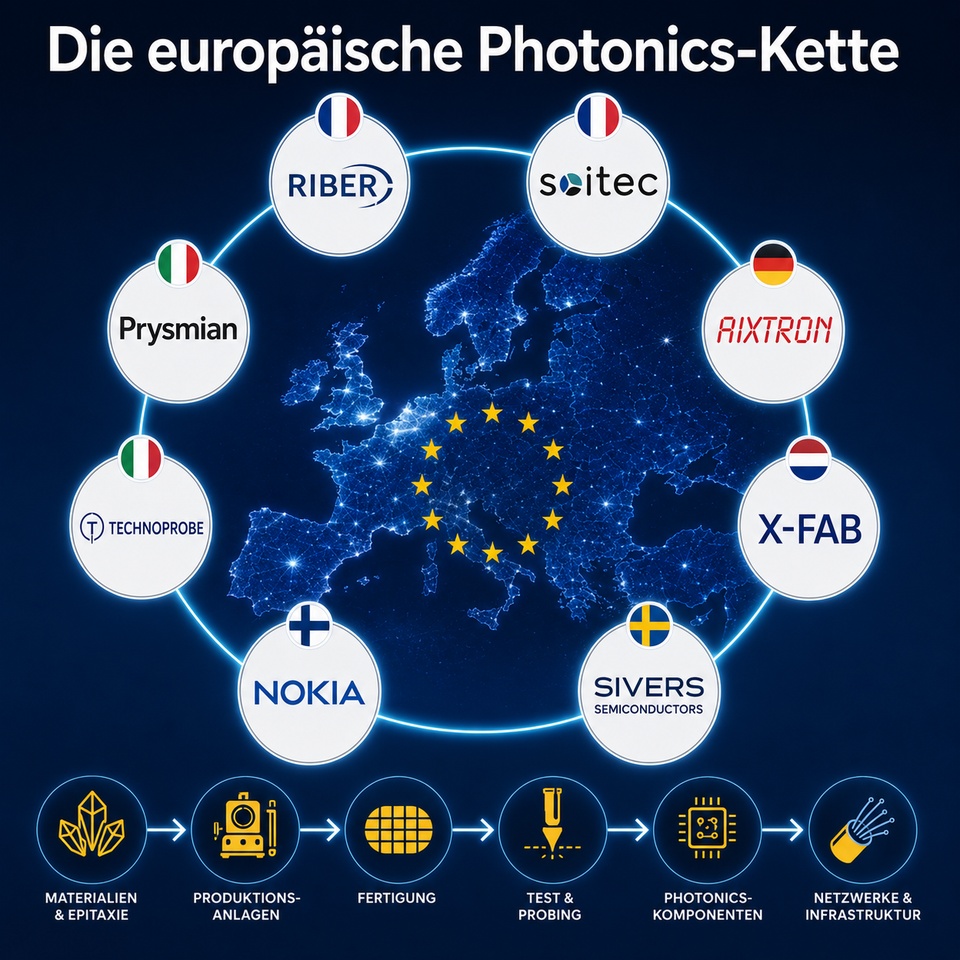

🇪🇺 Has Europe missed the AI boat?

Probably not. Perhaps a European photonics cluster. When people talk about AI, it’s usually about NVIDIA, data centers, or the next language models. At the same time, something exciting has happened in Europe: In the planned Chips Act 2.0 , photonics has been explicitly named for the first time as a strategic field of the future.

This comes as no surprise. After all, modern AI systems need more than just computing power. Above all, they must process ever-larger amounts of data quickly, reliably, and energy-efficiently. This is precisely where a future infrastructure bottleneck could emerge.

What I find exciting is that (with the exception of X-Fab and Nokia) my own portfolio and, to some extent, the bottleneck wikifolios already include several European companies that together almost form a complete photonics value chain :

🇫🇷 Riber

$ALRIB (-3.79%)

MBE systems for the production of highly specialized III-V semiconductors.

🇫🇷 Soitec

$SOI (-0.89%)

Specialty substrates and wafer technologies as the foundation for photonic integration.

🇩🇪 Aixtron

$AIXA (-4.42%)

Production equipment for InP, GaN, and other photonics applications.

🇳🇱 X-Fab

$XFAB (-0.9%)

European foundry expertise for sensor technology and photonic applications.

🇸🇪 Sivers Semiconductors

$SIVE (-8.46%)

Photonics and high-frequency chips for data transmission.

🇮🇹 Technoprobe

$TPRO (-4.41%)

Probe cards and test solutions for increasingly complex semiconductor structures.

🇫🇮 Nokia

$NOKIA (-6.26%)

Optical networking technologies for the next generation of data transmission. The acquisition of Infinera makes Nokia an increasingly relevant European player in the field of optical networking.

🇮🇹 Prysmian

$PRY (-2.58%)

Fiber-optic infrastructure as the physical backbone of digital data transmission.

Taken individually, some of these companies seem rather unremarkable. Taken together, however, they tell a different story. Not that of a continent that has fallen behind. But rather the story of a potential European photonics ecosystem in the making.

Whether this will actually give rise to global champions, no one knows today. But that is exactly where I look for bottlenecks: one level below the obvious winners. Where new technologies are made possible in the first place.

⚠️ Not investment advice.

2929

15 Comments

1Mon

I’ve also been reallocating my portfolio over the last few days… and invested in $SIVE, $XFAB, and $AAOI. I also invested in a smaller, lesser-known small-cap company called $SHT B. They have a partnership with $HEN.

I also find$NOKIA very interesting… Thanks for your research! I’ll take a look at the other stocks as well. 🙂

I also find$NOKIA very interesting… Thanks for your research! I’ll take a look at the other stocks as well. 🙂

•

33

•

1Mon·

wtf

$SIVE (-8.46%) who's holding this?

1111

7 Comments

Always wanted to, but was to scared of the vola sadly 😭

•

22

•1Mon·

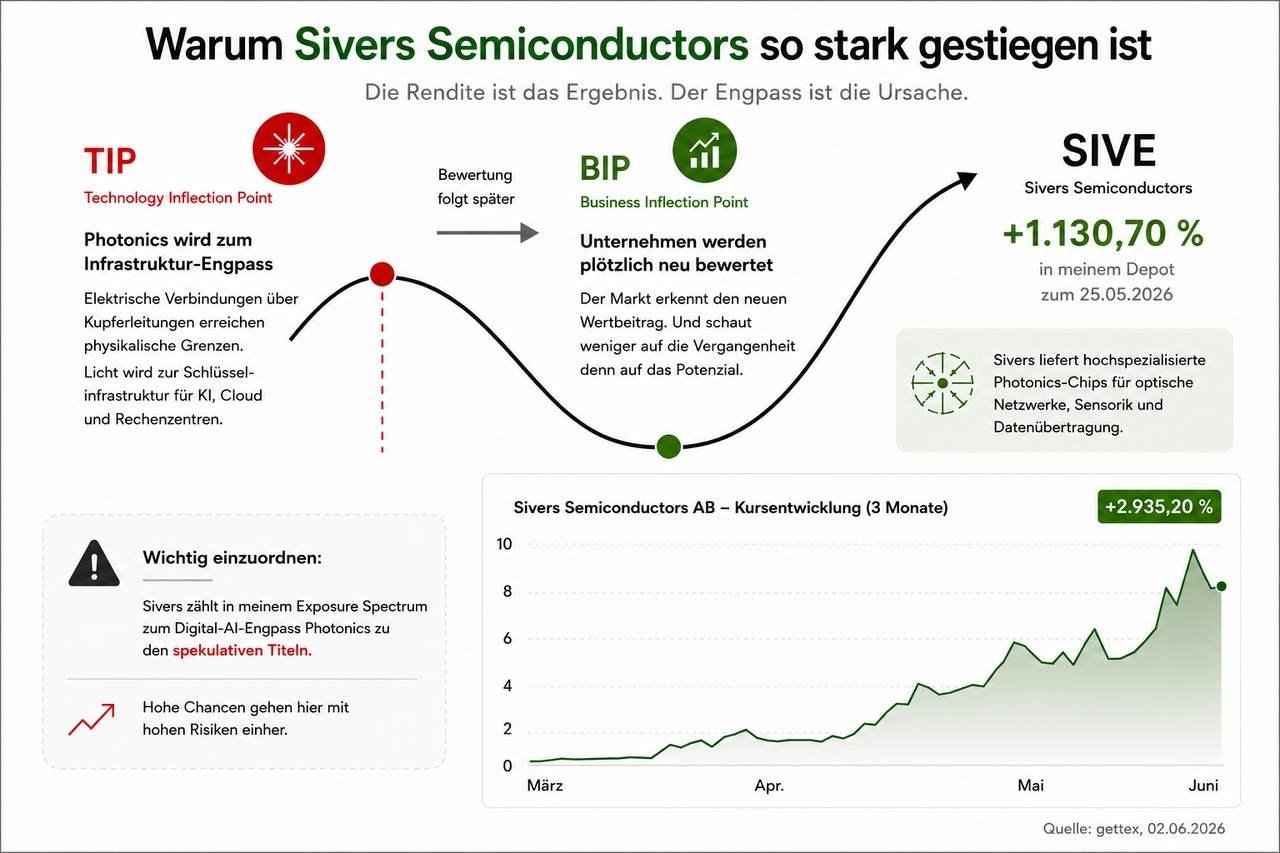

Why Sivers Semiconductors is rising so strongly today 📈

If you only look at the price trend, you will see a classic high flyer. If you dig a little deeper, you will see something else: a potential possible infrastructure bottleneck that is just beginning to become economically relevant.

For me, the development of $SIVE (-8.46%) well explained by two terms:

🔴 TIP = Technology Inflection Point

A technology inflection point occurs when a technology goes from being an interesting niche solution to a potentially indispensable infrastructure.

This could currently be the case with photonics could happen. AI systems are generating ever larger data streams. At the same time, electrical connections via copper are increasingly reaching their physical limits. Energy consumption, heat and signal losses are increasing.

This is why the industry is investing heavily in optical data transmission. Light instead of electricity. Photonics is therefore increasingly developing from a specialist topic into a potential AI infrastructure bottleneck.

🟢 GDP = business inflection point

The business inflection point often comes later. It occurs when companies suddenly benefit economically from this technological change. also benefit economically.

New orders.

New customers.

New sales potential.

New valuations.

A current example is the example is the collaboration between Sivers Semiconductors and GlobalFoundries that was announced today. This is interesting for me because such partnerships can show that a technology is finding its way out of the development phase and towards industrial scaling.

This is precisely the point at which a reassessment by the market. The market then looks less at the past and more at the question: "How big could this market become if the technology catches on?"

Nevertheless, it remains important that Sivers is still one of the speculative stocks in my exposure spectrum. speculative stocks in my exposure spectrum. The company is not an established infrastructure heavyweight like Coherent. It is much earlier in the cycle. The opportunities are therefore greater.

But so are the risks.

For me, Sivers therefore remains above all a bet that the current technology inflection point will eventually become a sustainable business inflection point.

After all, returns are rarely generated when everyone is convinced. They often arise when a new infrastructure bottleneck is just becoming apparent.

Incidentally, Sivers is also my driving force in the NextLimits wikifolio with a current gain of 822%.

2121

10 Comments

Cool post, thanks. I know a few people who are completely in FOMO thanks to Sivers... I'm a bit put off by the company but it actually seems to be an interesting thing. Is there another comprehensive post like this about Sivers?

LG

LG

•

44

•2Mon·

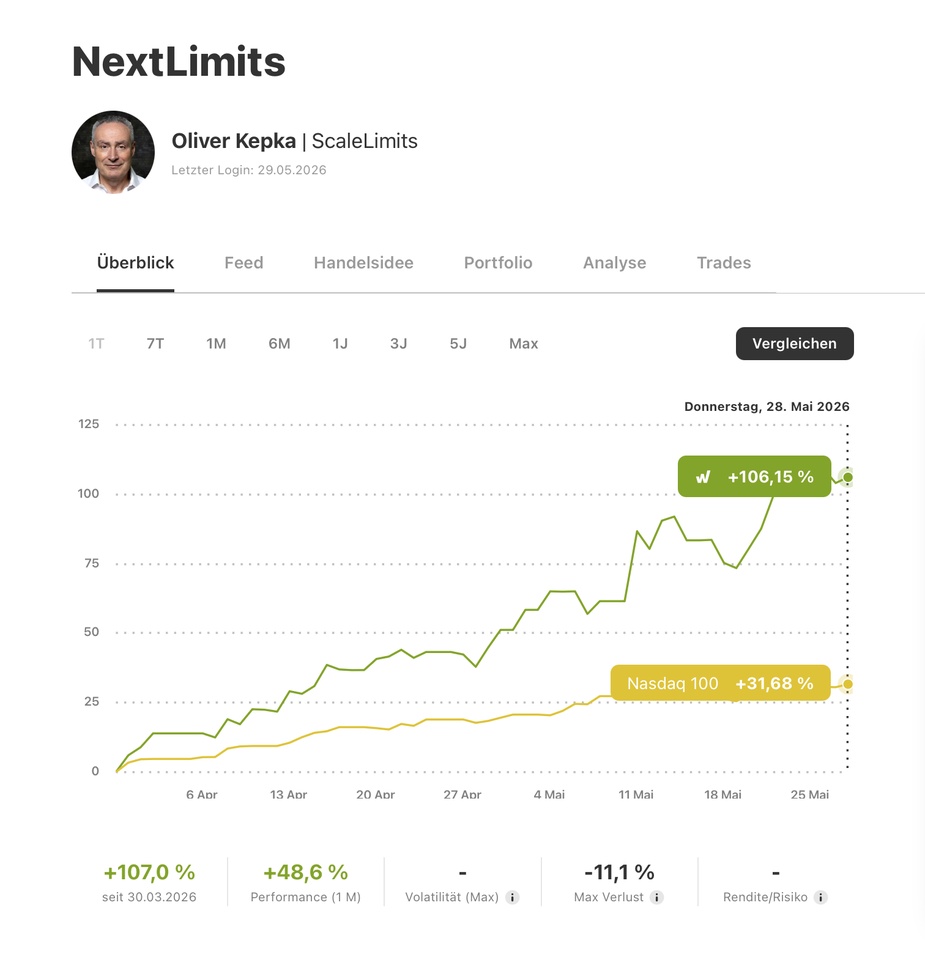

Update on NextLimits, the bottleneck wikifolio - after 2 months +107 %

NextLimits is at +107 %. All 20 positions are currently trading in positive territory 🟢 That makes me happy, of course. But what I find more interesting than the pure performance is the question of where it comes from.

Many of the strongest developments stem from topics that I have been observing for months as future technological bottlenecks:

- Photonics

- Advanced Materials

- Space Infrastructure

- sensor technology

- Directed Energy

Companies like Sivers Semiconductors $SIVE (-8.46%) or Everspin Technologies $MRAM (-9.22%) have performed particularly strongly. At the same time, the current development shows that the performance is not only being driven by individual outliers, but has so far been quite broadly distributed across the entire portfolio.

Interim conclusion: The underlying bottleneck theses currently appear to be confirmed. My thinking model here is DIBS (Dynamic Infrastructure Bottleneck Stack).

Nevertheless risk management as the search for opportunities. That is why I have already realized partial gains twice in Sivers Semiconductors and also made a partial sale in Everspin Technologies in order to limit the position sizes in the portfolio.

NextLimits deliberately focuses on topics where the next technological bottlenecks could arise. Not on what is already common knowledge today, but on the infrastructure, material and technology layers below. TechLimits stands for acute bottlenecks, CoreLimits for stability. All three form my ScaleLimits system.

This is still only just under two months. But so far the wikifolio is developing in exactly the direction I had in mind when I launched it.

2424

14 Comments

Is the 10% performance fee included in the chart?

If not, what does the chart look like without 0.95%pa + 10% for new ath?

If not, what does the chart look like without 0.95%pa + 10% for new ath?

•

22

•Trending Securities

Top creators this week

Real-time data from LSX · Fundamentals & EOD data from FactSet