As promised over the last two days, it’s finally time to reveal my buys amid the private credit selloff. On Monday I talked about what’s actually going on and why it’s likely less of an issue than people think. Yesterday, I explained how I freed up capital by selling my Netflix position. Today, let’s start with Brookfield Corporation.

Brookfield sold off roughly 20% from its highs along with the broader asset manager space. And at first glance, I understand why. The company does have a private credit arm. That alone is enough for the market to panic right now. But that’s exactly where I think the misunderstanding starts.

The current fear around private credit is centred on software lending. Loans given to often overvalued SaaS companies that might struggle to repay if growth slows or sentiment shifts. That’s not what Brookfield is doing.

Brookfield’s credit business is structurally different. Their focus is on real-asset-backed lending. That means loans tied to tangible, cash-generating assets like infrastructure, renewables, utilities or real estate. These are not abstract growth bets. These are assets that exist, produce cash flow and can serve as collateral.

That distinction matters. If something goes wrong, recovery dynamics are completely different. You’re not left hoping that a business model turns around. You have something you can restructure, operate or sell.

Another important point is that Brookfield has historically thrived in exactly these kinds of environments. They are one of the best distressed investors out there. Periods like post-2008 or during Covid were some of their strongest, because they had capital and discipline when others didn’t. To some extent, the business even works counter-cyclically.

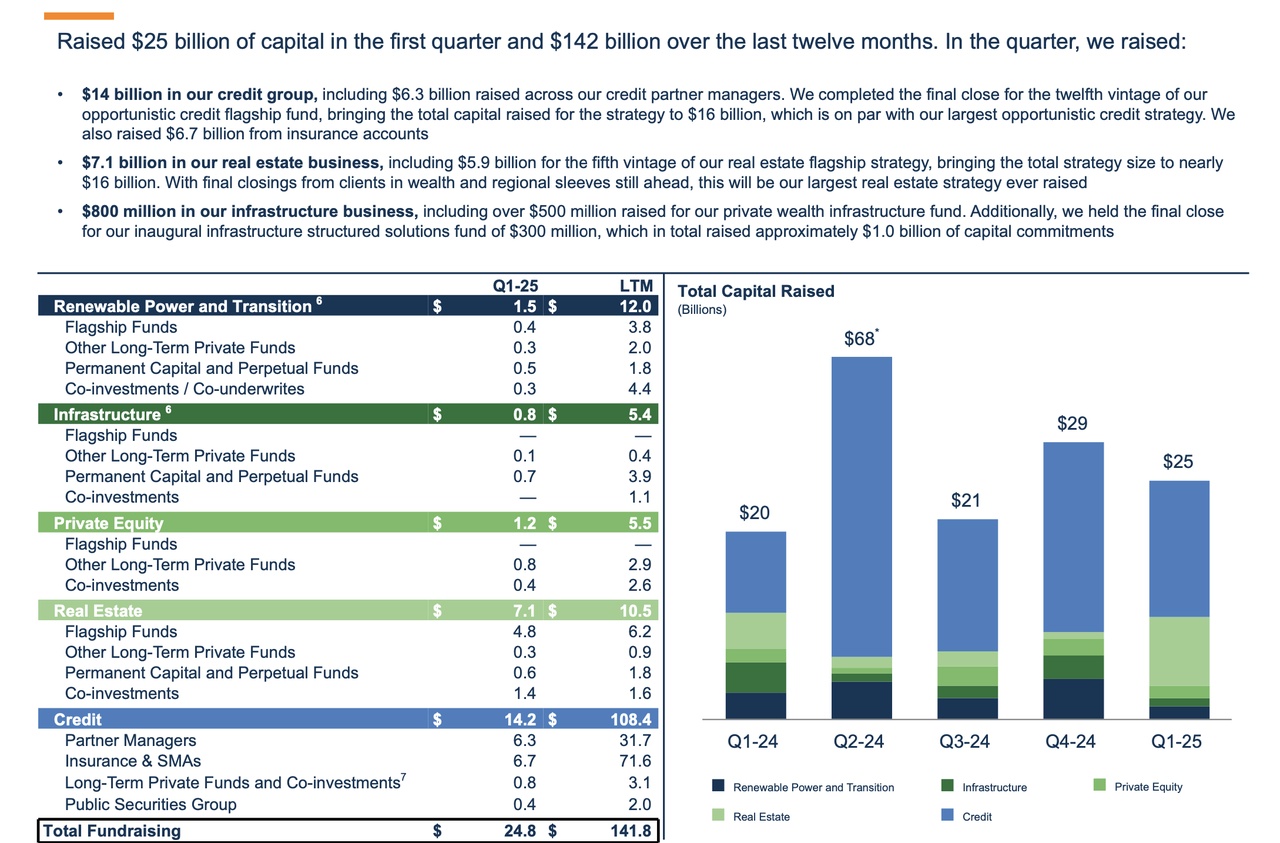

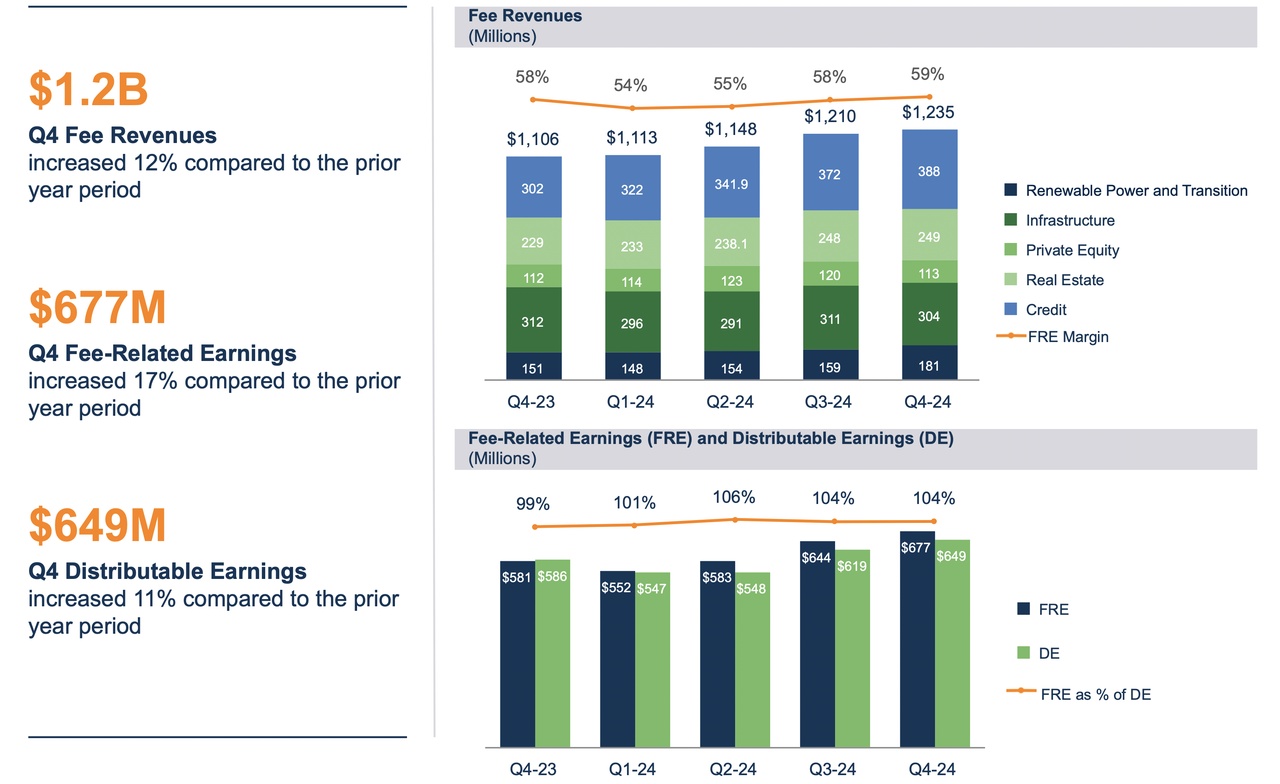

And it’s not like they are struggling in strong markets either. Brookfield just closed one of the largest fundraising cycles in its history, raising around $112 billion in 2025. At the same time, they’ve positioned themselves early in major secular trends like data centres, compute infrastructure and power supply for AI. That’s where a lot of capital is going over the next decade.

So yes, the company has exposure to credit. But not the kind the market is worried about. And I think that difference wasn’t properly reflected in the recent selloff.

Tomorrow, I’ll go into the second company I bought during this selloff, which in my opinion makes even less sense.