Good evening getquin community,

First of all, a bit about me:

I am 25 years old and have been investing for 2.5 years. I'm currently training to become a technical product designer because I just didn't like my old job anymore. In relation to this, my monthly savings rate is "only" around €400. In 1.5 years, however, I will have finished my training and my savings rate will increase.

Now to my problem:

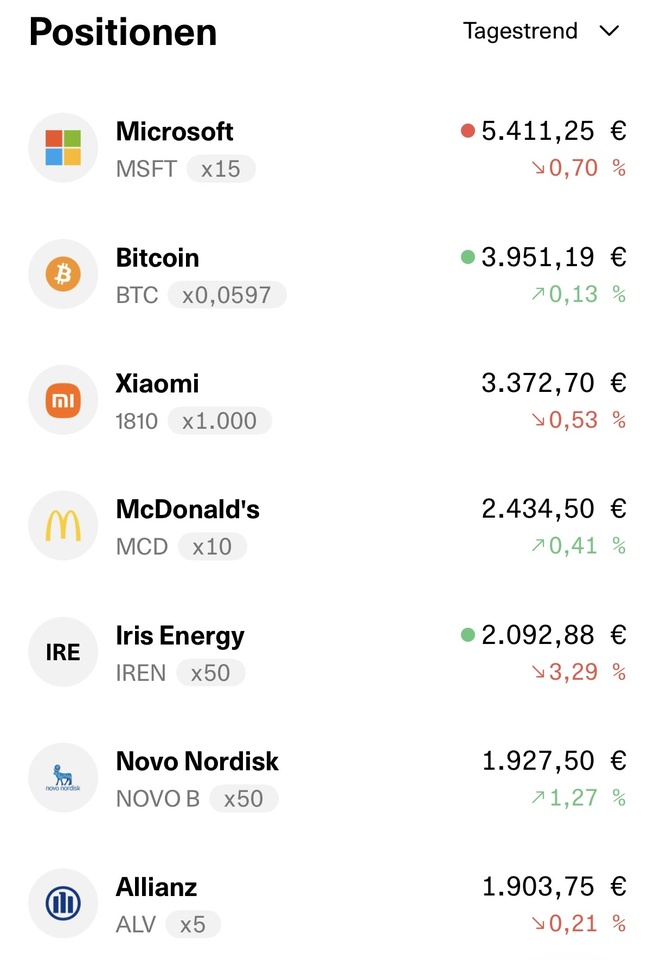

I have a - in my opinion - (very) vulnerable portfolio where there is some gambling involved. Maybe that's because I think I want to get a lot out of it with a low savings rate per month. So far, however, nothing has really gone wrong. In any case, I'm happy with the companies I've chosen in the long term. Despite all this, I can't get rid of the idea of simply investing stubbornly in 2 ETFs and continuing to invest in Bitcoin. That would put less stress on my inner self and I can just let my savings plan run its course.

How would you go about it? Continue with the current portfolio and buy on dips? What is your opinion on my current portfolio? Do you think I am better off with 2x ETF ($IWDA (+1,01%) & $EIMI) (+1,99%) and 1x $BTC (+0,97%) better?

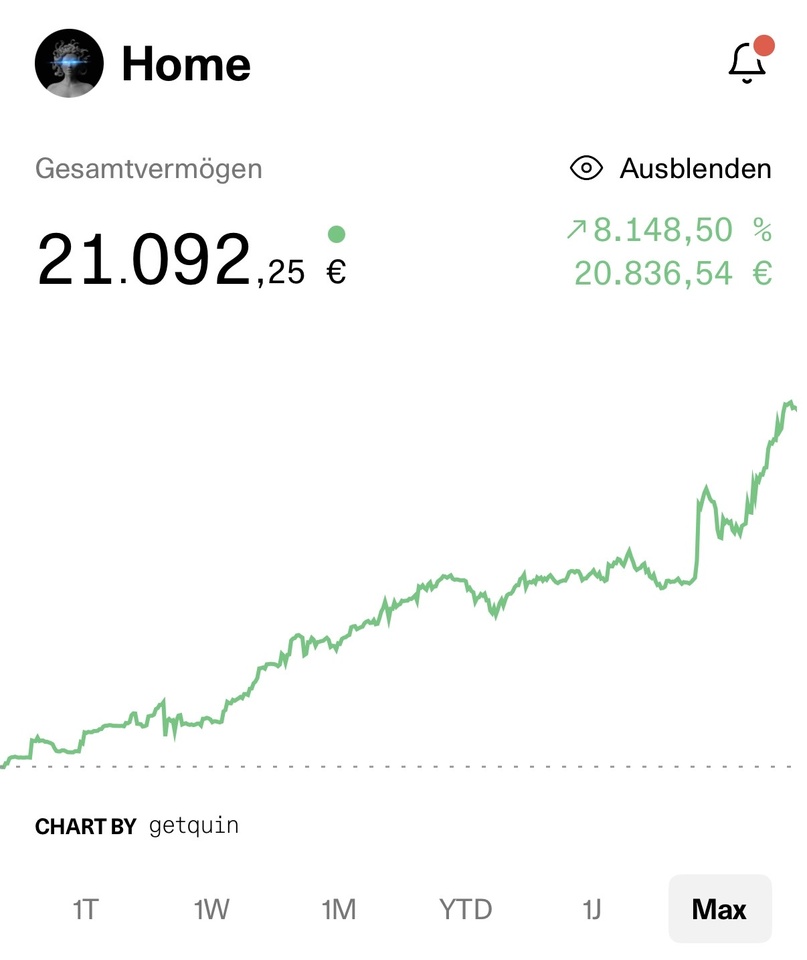

Attached is my current portfolio.

I look forward to any comments and would be grateful if you could help me with my decision!😊🐍☝🏼