My DCF model $UQA (+1,12%) resulted in a FW of €15 at the time, the rise is too fast. I am therefore switching to the $MUV2 (-0,31%)

Uniqa Insur Grp

Azione

Azione

ISIN: AT0000821103

Ticker: UQA

AT0000821103

UQA

Price

Discussione su UQA

Messaggi

88Mes·

UNIQA after three quarters: profit increases by 26 percent - increased outlook confirmed

The UNIQA $UQA (+1,12%) Insurance Group is continuing on its growth path and recorded a strong earnings performance after the first nine months of 2025. The profitable growth from all lines of business and regions as well as a high level of cost discipline are once again clearly reflected in the key figures.

Highlights of the first three quarters of 2025

- Premiums written increased by 9.2% to €6,411 million

- Net combined ratio improved to 91.0

- Profit before taxes increased by 24.4% to EUR 423 million

- Consolidated profit increased by 26.1% to EUR 333 million

- Capital ratio according to Solvency II remains at a very high level: 283

55

2 Commenti

burnheart@burnheart

8Mes

•

11

•11Mes·

UNIQA H1 2025: Strong growth & improved profitability!

A look at UNIQA's half-year results shows an impressive performance that underpins the corporate strategy.

Growth in the core business: premiums and sales increase significantly.

* Premium growth: +9.7%

* Increase in sales: +8.9%

The growth is broad-based, driven by Austria (+4.8%) and the CEE markets (+10.8%).

Profitability improves despite a challenging market environment.

* Profit before taxes: +6.5% to €295.5 million

* Consolidated profit: +5.3% to €232.5 million.

Key performance indicator: the net combined ratio improves to an excellent 90.5%. This figure shows that the core business is very profitable - income is significantly higher than costs.

Management confirms its confidence in the future: the outlook for profit before taxes in 2025 has been raised to €490-510 million.

Conclusion: UNIQA is not only growing strongly, but also very profitably and efficiently. The raised forecast and the solid key figures prove that the company is well positioned to achieve its strategic goals.

66

4 Commenti

Unfortunately, the price is falling sharply today, but you don't necessarily have to understand that.........Buy on setbacks!

•

22

•1Anno·

Uniqa still undervalued?

I have been buying into Uniqa since April and am clearly of the opinion that the share is still undervalued even after the 44% YTD price increase.

Forecast EPS increase of over 10% to 2025 and long-term EPS CAGR of 6%

without special effect from partial sale of Strabag shares (approx. another € 0.60 per share)

Calculation according to DDM model

Expected dividend: EUR 0.60

Expected dividend yield: 10% as small cap (normal value in the insurance industry is 8%)

Expected dividend growth: 6%

From the perspective of a dividend investor, this results in a fair value of 15 and the share is therefore currently trading around 34% below this.

Is anyone else here interested in Uniqa?

77

2 Commenti

1Anno

Yes, I am invested and also consider it to be undervalued, if only because of the Strabag share. This alone accounts for around 50% of the current market capitalization of $UQA.

••

1Anno·

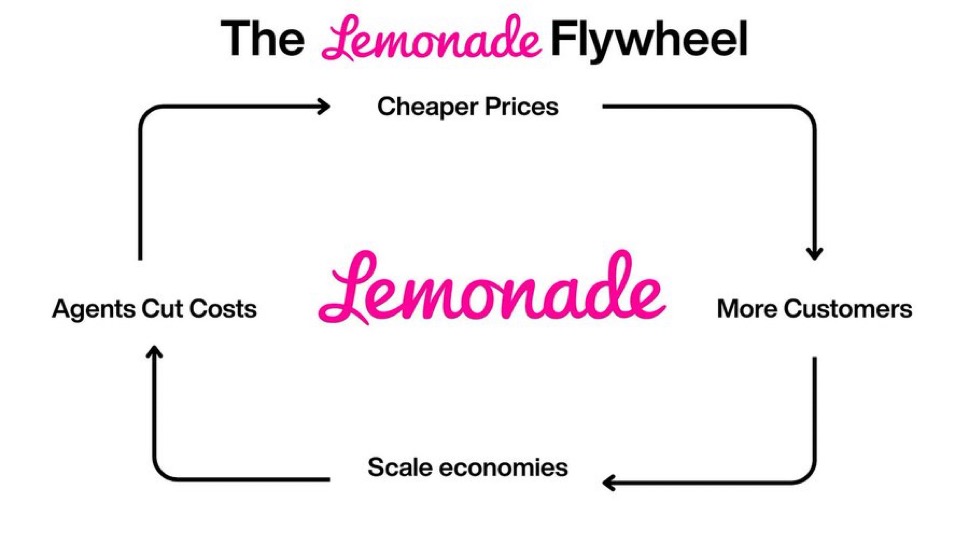

Lemonade Potential 🚀- Disruption in the insurance industry ? Brief company presentation

History:

$LMND (+0,47%) is an insurance company that was founded as a public benefit corporation and has its headquarters in New York and its European branch in Amsterdam. Lemonade has been traded as a public company on the New York Stock Exchange since July 2020.

$LMND (+0,47%) Insurance was founded in 2015 by Daniel Schreiber and Shai Wininger with the goal of revolutionizing the insurance industry through technology. The company started by providing home insurance and relies heavily on artificial intelligence and chatbots for claims processing and customer service.

$LMND (+0,47%) has experienced rapid expansion, including an IPO in 2020 and expansion into Germany

business model:

Lemonade, Inc. offers renters, homeowners, auto, pet and life insurance.

Current market capitalization 3 billion

The company's full-stack, artificial intelligence-powered insurance carriers in the United States and European Union replace brokers and bureaucracy with bots and machine learning. The company's digital substrate enables it to integrate marketing and onboarding with underwriting and claims processing, and to collect and utilize data.

Its technology includes Data Advantage,

AI Maya, AI Jim, CX.AI, Forensic Graph, Blender and Cooper.

AI Maya, the onboarding and customer experience bot, uses natural language to assist customers in the onboarding process.

AI Jim, the claims reporting bot, receives the customer's first claim and pays the claimant or rejects the claim without human intervention.

The company offers pet insurance policies that cover diagnoses, procedures, medication, accidents or illnesses. Even the basic pet insurance covers blood tests, urinalysis, laboratory tests and CT scans.

What is the Lemonade $LMND (+0,47%)

Giveback?

Giveback is at the heart of Lemonade. This core element of the business model enables customers to use their Lemonade insurance policies to support causes that are close to their hearts.

Since 2017, Lemonade has $LMND (+0,47%) donated over 10 million US dollars to help build new homes, provide clean water, improve education, promote animal rights and much more.

Here's how it works:

When a customer purchases a $LMND (+0,47%) renters, homeowners, auto or pet insurance, charges a flat fee to cover $LMND (+0,47%) a flat fee to support and grow the business. A portion of the premiums goes towards claims settlement and the balance goes directly to one of their Giveback Partners - non-profit organizations selected by our customers.

$LMND (+0,47%) is a non-profit corporation:

$LMND (+0,47%) is a Public Benefit Corporation and a certified B Corp, which means they are legally committed to making a positive social impact. B Corp certification is awarded to companies that demonstrate that they balance profit and purpose while putting people and the planet at the center.

Every three years, they undergo a comprehensive assessment of their entire organization.

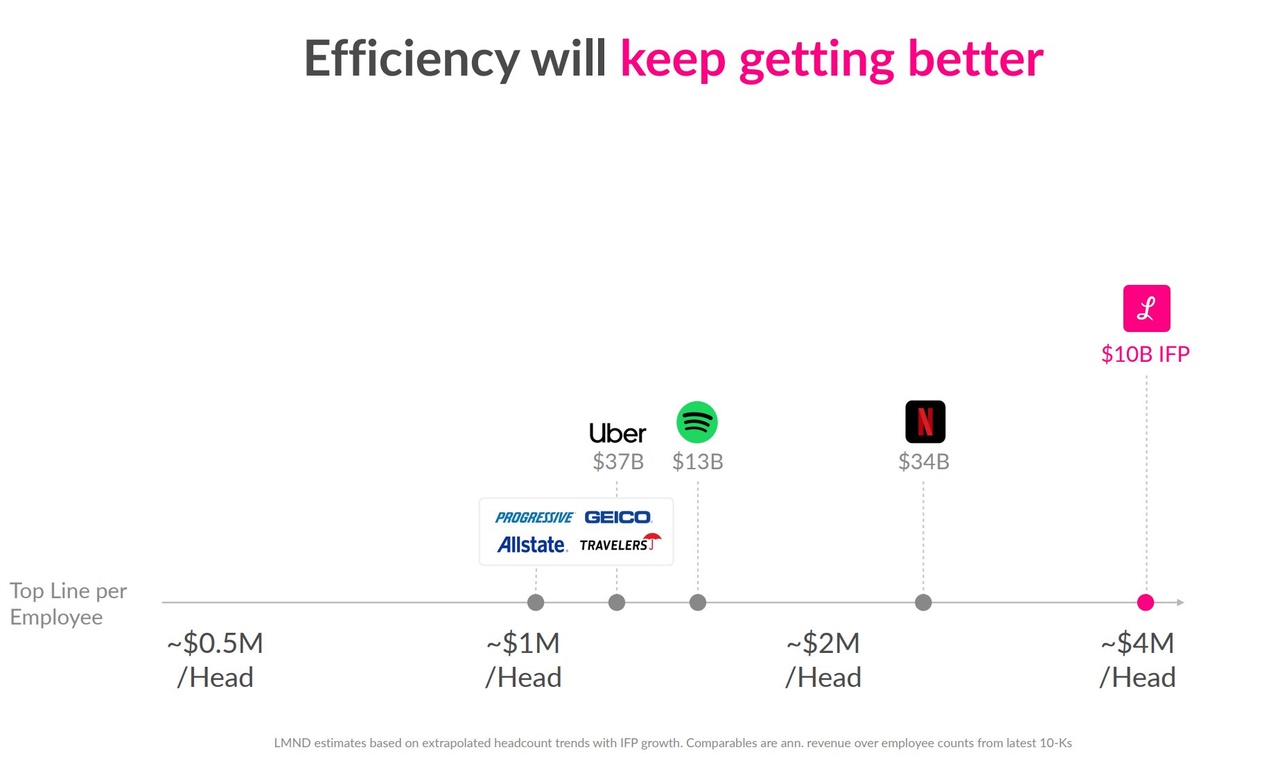

Number of employees: 1 258 (end of 2024)

Profitability:

$LMND (+0,47%) Approaching a turning point, possibly offering a promising investment opportunity.

Profitability increases with size, as costs do not rise due to additional premiums, as is normally the case with conventional insurance companies.

Management expects EBITDA profitability in 2026 and net profit profitability in 2027.

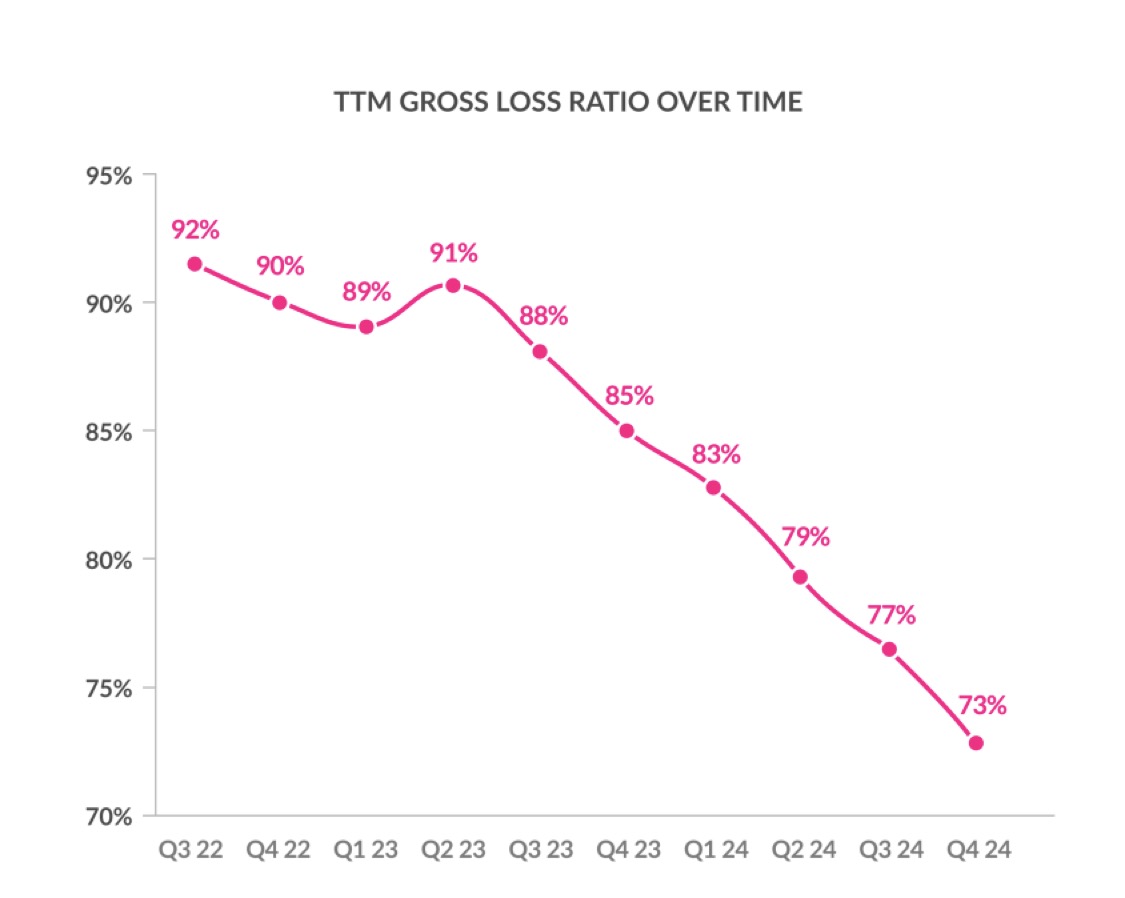

They see an extremely clear path to profitability:

They also have a clear path to profitability :

- Loss ratio from 92% to 73

- Net profit margin -123% to -20.2%

- Continued increase in sales growth rates

Growth:

Growth is currently still controlled, but the real growth is yet to come, with sales growth rates continuing to rise in the last two quarters.

They have been able to achieve these growth rates without an expansive expansion (both in existing and additional potential states) of automobile insurance, which represents a huge opportunity for $LMND (+0,47%) represents a huge opportunity.

Car insurance

$LMND (+0,47%) currently has around 2.3 million customers who use renters, pet and other insurance products. These customers use $LMND (+0,47%) for one reason: favorable price and convenience.

The share of car insurance is currently still very small and has a lot of room for expansion, so if we were to assume that only 30% of them become car insurance customers with an average annual turnover of USD 1,800, that would be an additional USD 1.24 billion in turnover per year ... just by cross-selling 30% (without any other new customers)

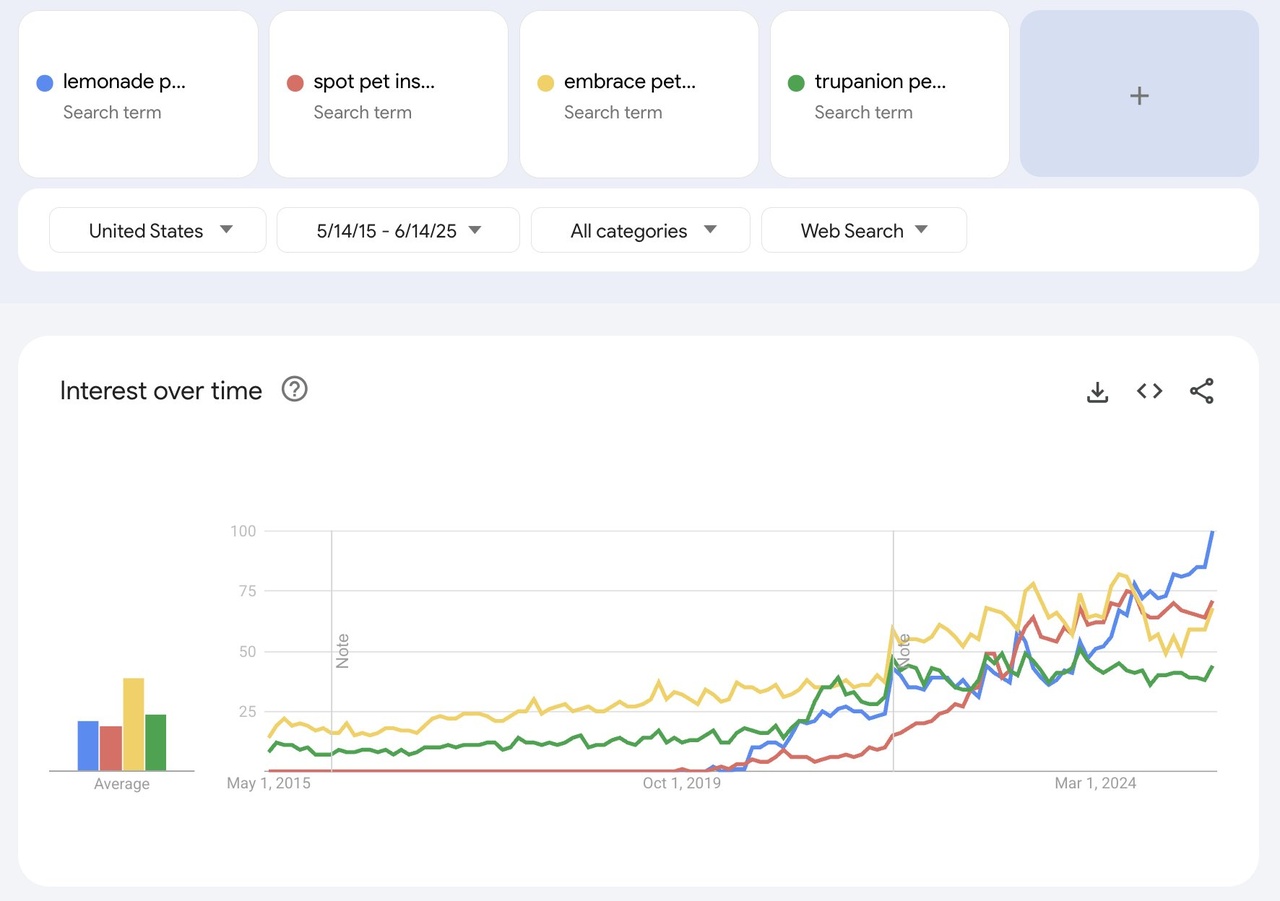

Pet insurance:

The pet insurance market was a $5 billion market in the US last year. It is expected to reach 6 billion dollars in 2025 and 15.7 billion dollars by 2030, growing by 22% annually.

$LMND (+0,47%) - Total annual premiums recently surpassed the $1 billion mark. So if you were to capture 50% of the pet insurance market, premiums would increase eightfold in just five years (800% assuming the projected growth above)

Trupanion (green line) has a 25% market share today. $LMND (blue line) is around 5%.

However, the search trend will continue to have a positive effect for $LMND (+0,47%) especially as it is only just beginning to expand further into all states. (This also applies to the other insurance segments)

Opportunities/long-term potential:

I think the future possibilities and opportunities for $LMND (+0,47%) a supposedly boring industry are enormous.

The insurance market has one of the largest TAMs of all.

The global insurance market was worth around USD 8 trillion in 2024. The USA and China are the largest insurance markets worldwide, with the USA leading the way with a market share of around 45% and China with around 10%.

- Slight international expansion (online)

- Product expansion (additional lines)

- Enormous cross-selling potential

- Decreasing dependence on reinsurance

- Simple and fast premium calculation, conclusion and claims settlement (through AI)

- Already tested/calculated in-house: https://www.lemonade.com

- 10-fold sales opportunity

$ALV (-0,03%)

$MUV2 (-0,31%) , $HNR1 (-0,59%) , $PGR (-0,89%) , $GEC , $ALL (-0,52%) , $AIG (-0,01%) , $UNH (-0,19%) , $CVS (-0,01%) , $UQA (+1,12%) , $G (+0,39%) , $VIG (+1,28%)

+ 3

4040

44 Commenti

1Anno

great article!

very interesting and never heard of it before.

are you getting in yourself?

have you already determined a fair price with an opportunity to buy?

LG

very interesting and never heard of it before.

are you getting in yourself?

have you already determined a fair price with an opportunity to buy?

LG

•

55

•1Anno·

Exchange in the medium-term portfolio

In the last 2 days I have made a reallocation. I have sold the well performing $VIG (+1,28%) and sold it and $UQA (+1,12%) into the portfolio. In my opinion, it offers more upside potential and also has a higher dividend yield.

44

5 Commenti

1Anno

I would at least wait for a correction :)

••

1Anno·

Hello to all my hard-working investors,

Today I decided to make a difficult but rationally sound decision and finally sell Uniqa. Back then I bought because of the dividend, but at completely the wrong time and without proper analysis. Every now and then you have to realize losses.

I am sure that my money will be better off in another investment. I will probably tend to increase $GOOGL (+6,34%) tend to.

33

12 Commenti

When and at what price did you get in - if you don't mind me asking?

•

11

•