Stock market in status monitor this weeks ;

$MRVL (+4,63%) , $CAMT (+5,68%) , $WOLF (+4,04%) , $HPE (+8,02%) , $MX (+8,63%) , $STM (+0%)

■ $TQQQ , $SPY , $SOXL ,$SOXX (+1,25%) ,$SMH (+1,68%)

■ Super cycle-Super computer -Moment in Cycle

Messaggi

4Stock market in status monitor this weeks ;

$MRVL (+4,63%) , $CAMT (+5,68%) , $WOLF (+4,04%) , $HPE (+8,02%) , $MX (+8,63%) , $STM (+0%)

■ $TQQQ , $SPY , $SOXL ,$SOXX (+1,25%) ,$SMH (+1,68%)

■ Super cycle-Super computer -Moment in Cycle

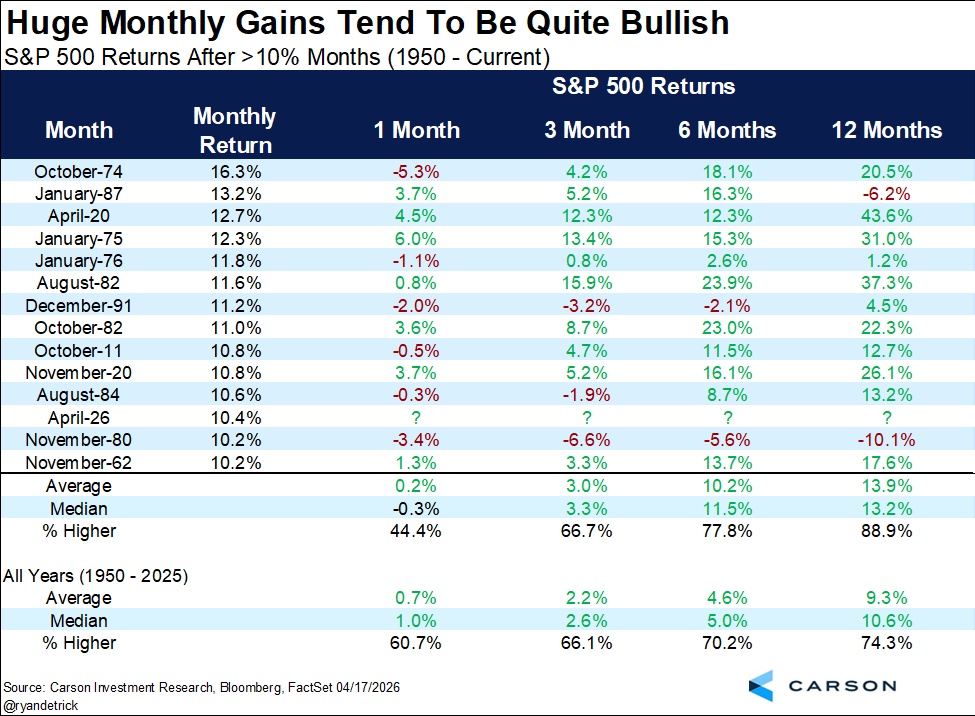

First day of the month, and it is worth looking at what April left behind.

The $SPY closed the month with a gain of more than +10%, a move that has only happened 14 times since 1950.

That alone shows how rare this kind of event is.

What is even more interesting is what happened next.

In those 14 cases, the market was higher 12 months later in 12 out of 14 times. That means it closed negative only 2 times.

The average return over the following 12 months was around +13.9%.

Of course, history is not a prediction or a guarantee for the future. Every period comes with different conditions such as interest rates, inflation, and geopolitical risks.

However, historically, strong monthly moves like this have often been associated with continued positive momentum.

We begin the new month with an interesting market statistic worth watching.

Earnings season continues to confirm something we often discuss. In the end, markets focus on profits, growth, and future expectations.

A few hours ago, we saw excellent results from several tech giants, and now $AAPL (-1,55%) has joined the list. This shows that the world’s biggest companies continue to create enormous value.

$MSFT (+4,92%) reported strong growth, with Azure remaining very powerful and demand for AI services rising sharply. $AMZN (+4,18%) delivered strong revenue and impressive profitability, with AWS continuing to be a key earnings engine. Alphabet impressed with major Cloud growth and solid advertising performance. $META (+6,34%) also posted strong revenue growth, although the market remained cautious about rising AI infrastructure spending.

Apple completes the picture. Revenue reached $111.2 billion, up around 17%, driven by strong iPhone sales and a solid rebound in China. The company also announced a new $100 billion buyback and a dividend increase.

In simple terms, when the largest companies in the $SPY keep delivering results like these, it becomes clear why the market remains resilient despite wars, rate fears, and constant negative headlines.

This does not mean corrections cannot happen. It means that behind the headlines there are real businesses producing profits, cash flow, and growth.

Markets are forward-looking. Right now, they are seeing that the giants continue to perform.

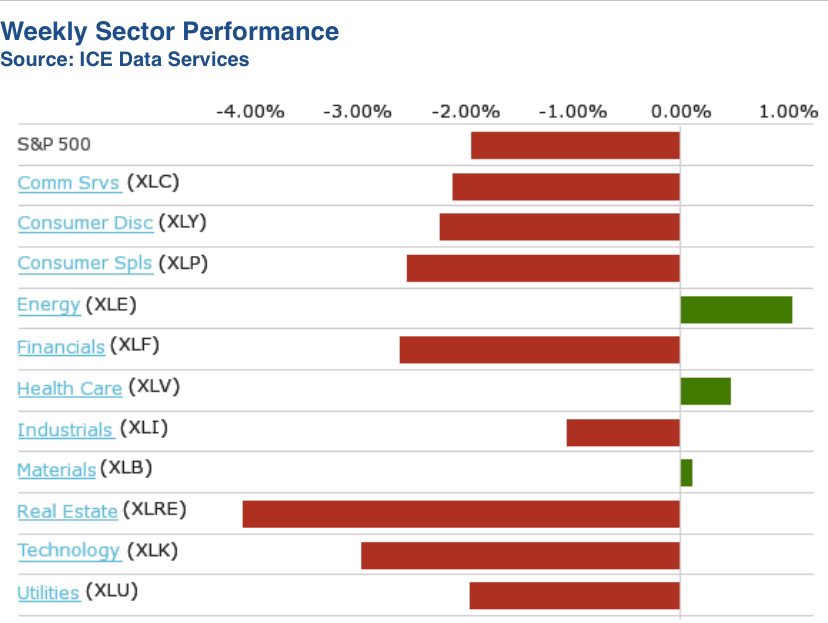

S&P 500 posts weekly decline as stronger-than-expected labor market data dampens hopes for rate cuts

The Standard & Poor's 500 Index fell 1.9% this week as stronger-than-expected December labor market data dampened hopes for interest rate cuts this year.

The market index closed Friday's session at 5,827.04 points. The weekly decline came in four trading days as the US stock market was closed on Thursday for a national day of mourning in honor of former President Jimmy Carter.

This is the second consecutive weekly decline for the S&P 500 and the index is now down 0.9% for both the month and the year.

According to government data, the US economy created more jobs than expected in December, while the unemployment rate fell unexpectedly. Nonfarm payrolls rose by 256,000 last month, beating the Bloomberg consensus estimate of a 165,000 increase. The unemployment rate fell from 4.2% in November to 4.1%. Analysts had expected it to remain at 4.2%.

The real estate sector was the hardest hit this week, falling by 4.1%, followed by a 3.1% decline in the technology sector and 2.7% in the financial sector.

Among the losers in the real estate sector, shares of BXP (BXP) and Federal Realty Investment Trust (FRT) were down 9% and 7.3%, respectively.

In the technology sector, shares of ON Semiconductor (ON) fell by 16% due to negative analyst ratings. The company was downgraded by Truist and analysts from Deutsche Bank and Goldman Sachs lowered their price targets.

The energy sector led the gainers, rising 0.9%, followed by a 0.5% rise in the healthcare sector and a 0.1% rise in materials.

The rise in the energy sector coincided with a rise in crude oil futures. Gainers included shares of Texas Pacific Land (TPL), up 7.4% for the week, and Devon Energy (DVN), up 6.1%.

In the coming week, investors will focus on inflation data. The Producer Price Index for December is due on Tuesday, followed by the Consumer Price Index for December on Wednesday. Later in the week, retail sales for December are due on Thursday and housing starts and building permits for December on Friday, among other reports.

Also, the fourth-quarter 2024 reporting season kicks off, with results expected from several financial companies, including JPMorgan Chase (JPM), Wells Fargo (WFC), BlackRock (BLK), Citigroup (C), Bank of America (BAC) and Morgan Stanley (MS). UnitedHealth Group (UNH) is also expected to present quarterly figures.