Hello my dear GQ community, since dear @Tenbagger2024 somehow has problems with his company presentation post, I'm jumping in for a change 😝 so that you have something to read 😂 I hope I still reach a few of you readers 🤓

have fun 😬

Today I would like to introduce you to a company that I am sure many of you are not yet familiar with.

It is the Japanese BioTech Pharma / Tech (?) company with the name: PeptiDream $4587

PeptiDream $4587 is not a classic pharmaceutical company that only sells its own pills. It is a technology platformthat provides the "operating system" for the discovery of new active ingredients. In the world of biotechnology, PeptiDream $4587 is the undisputed king of macrocyclic peptides.

👤 Management: Visionary & Strategic

- CEO: Patrick C. Reid

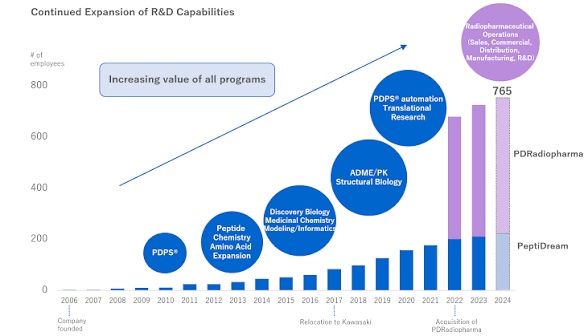

- Reid is not a typical Japanese CEO, which gives the company a very international and agile culture. Under his leadership, PeptiDream has been transformed from a small university spin-off to a global player with over 120 research programs.

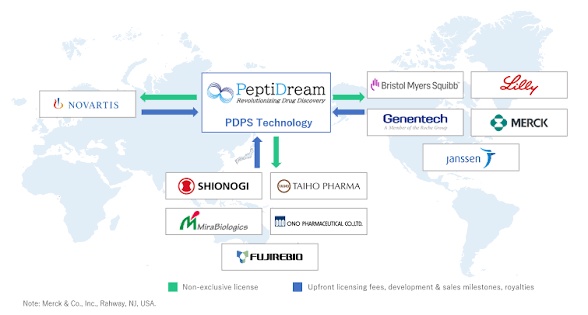

- Strategy: He consistently focuses on collaborations with "big pharma" (Novartis $NOVN (-0,67 %) , Eli Lilly $LLY (+0,32 %) Merck $MRK (-0,3 %) Genentech $GENETEC ) in order to shift the risk of failures in clinical trials onto the partners, while PeptiDream $4587 profits from milestone payments and license fees.

--------------------------

🔬🏭The business model: "The Discovery Powerhouse" 🎯

PeptiDream $4587 pursues a strategy of massive scaling through partnerships. Instead of investing billions in their own research and hoping for a "blockbuster", they let the giants of the industry work for them.

1-core technology PDPS: The Peptide Discovery Platform System is a kind of "Google high-speed search engine" for active ingredients. It can screen trillions (!) of different peptides in just a few weeks to find exactly the one molecule that binds to a disease target.

PDPS in detail:

Imagine you are looking for a matching key 🔑 for a very complicated lock (a protein that causes a disease). Classic pharmaceutical companies laboriously try out a few thousand keys 🔐.

- PDPS (Peptide Discovery Platform System): PeptiDream builds a "library" in a test tube trillions (10¹²) different macrocycles (ring-shaped peptides).

- The highlight: Each peptide is labeled with a DNA "barcode". When a peptide binds to the target protein, the barcode is read and the company knows immediately: "This is the active ingredient!"

- Success rate: PeptiDream $4587 states that for over 95 % of all biological objectives🎯 (targets) within just 4 weeks. This is record-breaking in the industry.

Technology licenses: Partners such as Lilly $LLY (+0,32 %) or Novartis $NOVN (-0,67 %) pay millions to be allowed to use the PDPS technology themselves.

🚀2 The growth pillar:

The "PDRadiopharma" transformation:

Through the acquisition of the radiopharmaceutical business of Fujifilm Toyama Chemical PeptiDream has $4587 vertically integrated. They now own the entire chain: from the discovery of the peptide to the production and marketing of nuclear medicine diagnostics and therapeutics in Japan.

This is currently the most exciting transformation. With the acquisition of PDRadiopharma (formerly Fujifilm $4901 (+0,23 %) ), PeptiDream is no longer just a software developer, but also a logistics giant. logistics giant in Japan.

- Why radiopharmaceuticals? These drugs decay quickly (radioactivity!). You need an extremely precise network to get them from the reactor to the patient. PeptiDream now has this infrastructure in Japan.

🔁3 The " $AMZN (-2,34 %)

Amazon model" of the pharmaceutical world

PeptiDream $4587 follows the principle of reinvestment:

They are using the stable cash flows from radiopharma sales in Japan to further automate their PDPS platform. The screening system is now largely robotized, which reduces the marginal costs per new project to almost zero.

--------------------------

🆕📰- Latest news (February/March 2026): PeptiDream $4587 has just completed the first patient dose in a Phase 2 trial for a new treatment for prostate cancer (177Lu-PSMA-I&T) in Japan. This is in collaboration with the Curium Group.

Strategic realignment 2026

The latest earnings calls (February 2026) show that

- Focus on in-house development: PeptiDream is moving to bring more programs to clinical phase 1 or 2 itself before licensing them. Although this will increase costs in the short term (R&D budget for 2026 increased to approx. JPY 6.4 billion), but massively increases the value of the deals.

- Pipeline turbo: The number of clinical programs (the phase where it gets really expensive and valuable) has almost doubled in the last year. The target for T2026 is 6 to 12 new clinical programs

--------------------------

🤝The "Big Three" alliances

These are the most lucrative and strategically important partnerships, often worth billions (in milestones).

- Novartis $NOVN (-0,67 %)

: Probably the closest partner. In May 2024 the collaboration was massively expanded. Novartis paid USD 180 million in advancewith the prospect of a total of up to USD 2.71 billion. Focus: Radioligand therapy (RLT). Novartis uses PeptiDreams peptides to precisely steer radioactive particles to tumors.

- Eli Lilly $LLY (+0,32 %) A partnership worth up to 1.2 billion USD. Lilly is using the PDPS platform primarily to find peptides that can deliver drugs across the blood-brain barrier or for the next generation of metabolic drugs (keyword: weight loss injection optimization).

- Bristol Myers Squibb $BMY (-0,75 %): BMS has "inherited" an existing alliance with PeptiDream through the acquisition of RayzeBio. This is also about targeted cancer therapy.

The global network (excerpt)

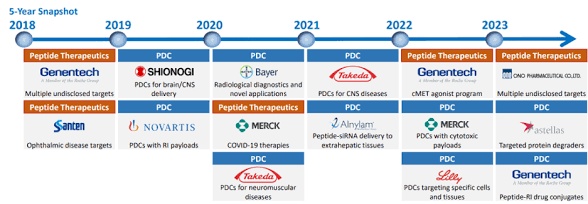

In addition to those mentioned above, there are over 120 research programs. The partners include:

- Merck (MSD) $MRK (-0,3 %)

: Focus on various therapeutic areas.

- Genentech (Roche): $ROG (-3,01 %) Collaboration on multi-specific antibodies and PDCs.

- Astellas $4503 (-1,1 %)

& Takeda $4502 (-1,67 %) Strong local partnerships in Japan.

- Amgen $AMGN (+0,33 %)

& Bayer $BAYN (-2,91 %)

: Licensees of the PDPS technology.

--------------------------

📊Sales development (growth leap through acquisition) in recent years:

- 2021: approx. JPY 9.4 billion

- 2022: approx. JPY 26.8 bn (massive leap due to the integration of the Fujifilm radiopharmaceuticals business)

- 2023: approx. JPY 31.1 bn

- Trend: Sales have more than tripled within three years. While milestone payments used to account for almost 100% of revenue, stable revenue is now generated from the sale of radiopharmaceutical diagnostics in Japan.

📈Profitability and margins

PeptiDream $4587 is an exception in the biotech sector, as they have been almost consistently profitable:

- Operating margin: This often used to be over 40-50% (before 2022) as there were hardly any production costs. Since the acquisition of the radiopharmaceutical business, the operating margin has fallen to around 20-25 % has fallen. This sounds like a step backwards, but it is a sign of a more mature business model with physical products.

- Net result: After a dip in 2022 (acquisition costs), net profit stabilized significantly in 2023 and 2024. For 2025/26 the economies of scale of the PDPS platform are expected to lead to rising margins again.

Expenditure on research and development

A critical point for biotech:

- PeptiDream $4587 continuously spends about 20-30 % of its turnover on R&D.

- The special feature: Since partners (such as Eli Lilly $LLY (+0,32 %) or Novartis $NOVN (-0,67 %) ) pay for phase 2 and 3 clinical trials for the joint programs, PeptiDream's burn rate remains extremely low compared to US biotechs. $4587 remains extremely low compared to US biotechs. They conduct research "at the expense of others".

💴The cash position and debt:

- Cash reserves: At the end of 2023/beginning of 2024, the company held approx. JPY 28-30 billion in cash and cash equivalents.

- Debt: Debt was raised through the acquisition of PDRadiopharma, but the ratio of net debt to EBITDA is very healthy (often below 1.0), which means a very conservative balance sheet for a growth company.

The "pipeline" key figures

The most important non-financial key figure for PeptiDream $4587 is the number of programs:

- 2020: approx. 100 programs

- 2024: over 120 programs️

- Meaning: Each program is a "ticket" in a lottery in which PeptiDream $4587 does not pay for the stake, but participates in the winnings. According to management, the hit rate of PDPS technology in identifying binding agents is almost 100%.

The current key figures 2025/26 📊

- Market capitalization: approx. USD 2.5 - 3 billion (depending on exchange rate).

- Exchange rate: approx. 2,200 - 2,500 JPY (TSE: 4587).

- Sales forecast 2026: approx. 32 billion JPY.

- Profitability: PeptiDream $4587 is one of the few biotech companies that has been consistently profitable for years.

- Growth turbo: For 2026, profit growth of over 30 % driven by new clinical programs (target: 6-12 new programs in 2026).

- Return on equity (ROE): Forecast at approx. 17 %which is exceptionally efficient for the biotech sector.

Key figures for the last few years:

The market often punished the share between 2021 and 2023 because the integration of the radiopharmaceuticals division diluted the clean "software margins".

Since 2024, however, the market has recognized the strategic value 👀:

PeptiDream $4587 is now no longer just a supplier of ideas, but controls the platform and the delivery (PDCs).

--------------------------

Why is the share exciting? (Bull case) 🚀

1. Validation by giants: When companies like Eli Lilly $LLY (+0,32 %) (market leader in weight loss products) sign contracts worth USD 1.2 billion with PeptiDream $4587 shows the quality of the technology.

2. Scalability: PeptiDream $4587 can earn money on hundreds of drugs simultaneously without bearing the full development costs.

3. Radiopharma boom: The market for targeted radiation therapy (radioligand therapy) is exploding right now. PeptiDream $4587 is perfectly positioned here thanks to PDRadiopharma and the $NOVN (-0,67 %) Novartis deals perfectly positioned.

4. Enormous upside potential: Many analysts see a price target of over JPY 3,000which corresponds to a potential of +30 % to +50 %.

Risks (bear case) ⚠️

- Dependence on partners: If a major partner stops a program, planned milestone payments are lost.

- Currency risk: As many contracts are in USD but invoiced in JPY, exchange rate fluctuations affect the balance sheet.

- Clinical setbacks: Despite the best technology, drugs can fail in phase 2 or 3 due to side effects.

--------------------------

✍️Meine personal conclusion & rating:

At first glance $4587 an absolute disaster in terms of share price and key figures, but Peptidream $4587 is the "paddlewheel stock" in the gold rush of modern drug discovery. If you don't want to bet on a single drug, but on the technology that makes them all possible, you will find a highly profitable niche king here. The potential is definitely there.

- Status: Growth stock with solid cash position (approx. JPY 28 bn reserves).

- They do not develop drugs, but the "peptide keys" that bring active ingredients precisely into the cell. In 2026, their radiopharma division will be the big driver.

- Status: Platform model with many global partners (license fees)

-The big $LLY (+0,32 %) & $NOVN (-0,67 %) - effect

unfortunately the share is not (yet) tradable in Germany only on the Tokyo Stock Exchange 🥲

Your stock master ✌️

Looking forward to your assessment of how you rate the company?

@Tenbagger2024

@Get_Rich_or_Die_Tryin

@PikaPika0105

@Multibagger

@Klein-Anleger

@Raketentoni

@Liebesspieler

@HoldTheMike

@Shiya and of course others from the community 🙇♂️