Eventim

Price

Debate sobre EVD

Puestos

34

𝐂𝐓𝐒 𝐄𝐕𝐄𝐍𝐓𝐈𝐌: 𝐒𝐭𝐚𝐫𝐤𝐞𝐬 𝐐𝟏 𝐦𝐢𝐭 𝐃𝐞𝐮𝐭𝐥𝐢𝐜𝐡𝐞𝐦 𝐋𝐢𝐯𝐞-𝐄𝐧𝐭𝐞𝐫𝐭𝐚𝐢𝐧𝐦𝐞𝐧𝐭-𝐖𝐚𝐜𝐡𝐬𝐭𝐮𝐦

📊 𝐄𝐫𝐠𝐞𝐛𝐧𝐢𝐬𝐬𝐞

- Group sales: €613.5M (+23.0%)

- Adjusted EBITDA: €118.9M (+18.5%)

- Adjusted EBITDA margin: 19.4%

⠀

🎯 𝐀𝐮𝐬𝐛𝐥𝐢𝐜𝐤𝐜𝐜𝐤

- Executive Board sees Group and both segments in line with expectations for 2026

⠀

📌 𝐖𝐢𝐜𝐡𝐭𝐢𝐠𝐬𝐭𝐞 𝐏𝐮𝐧𝐤𝐭𝐞

- Live Entertainment revenue increases by 38.3% to €403.6M

- Live Entertainment EBITDA jumps by 151.1% to €29.1M

- Ticketing revenue increases by 2.5% despite strong comparative basis

- Ticketing EBITDA grows to €89.8M (+1.2%)

- Successful US tours and strong demand in Germany drive growth

- Stage Entertainment partnership extended long-term

⠀

💬 𝐌𝐚𝐧𝐚𝐠𝐞𝐦𝐞𝐧𝐭-𝐀𝐮𝐬𝐬𝐜𝐚𝐠𝐞𝐞

'CTS EVENTIM has made a successful start to the 2026 financial year and is continuing its profitable growth trajectory.

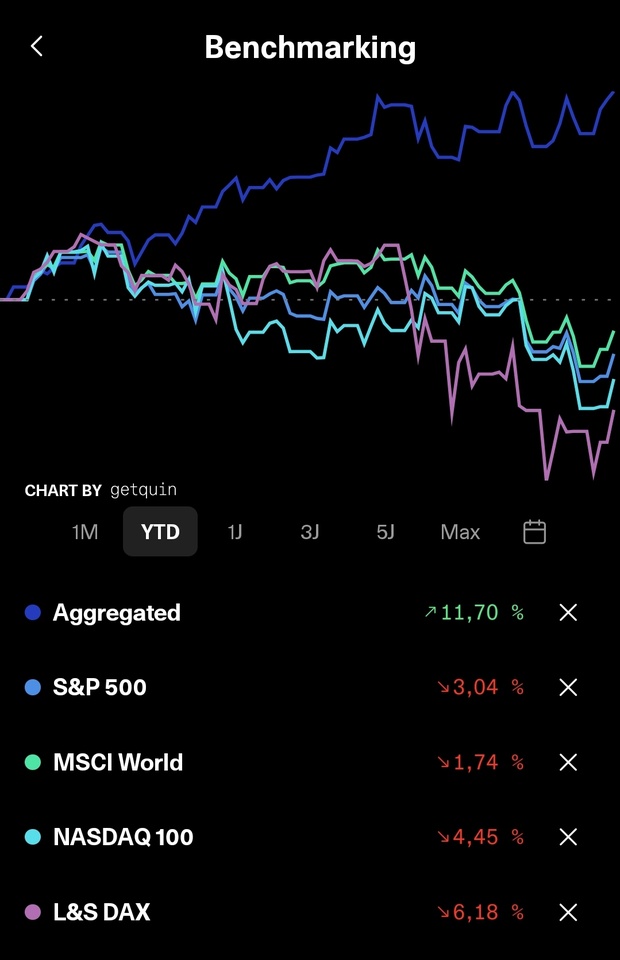

Next intermediate milestone reached and review of 04/2026

Even though the month of April was only average from my point of view, there are still a lot of positive things to report so far...

...on the one hand, all the sweating and work was probably worth it after all, because after the health-related interruption to my further training, I was able to successfully tick off the last IHK exam (tax law) and can now officially call myself a "financial accountant" 🫠😊

Now the certifications (bookkeeping/payroll accounting) in DATEV follow and then the whole thing is complete...

...well, Schalke also got promoted at the weekend 💙🫶💙💙🫶💙

And last but not least, the next small milestone was reached today, 3 months earlier than planned 💪🏻

Shows me at least that everything together is on the right track...

》But let's stick to April for now 《

Even though it was one of the few months in a long time where we didn't close above the market result, everything is in the green and, as already mentioned, the next milestone was also reached 3 months before the target...

...for the year as a whole, things have been pretty stable so far and are just purring along...

...although my approach is also rather conservative and based on value and dividends in the long term without hype and co...

...so at the end of the month I will have my 3rd full year on the stock market and in my opinion the whole thing doesn't look too bad 😊

Especially as the dividends have already built up a really good positive cash flow after this short time, in addition to the monthly savings installment, and so the snowball starts rolling all by itself...

》Dividends《

This month there were €374.69 in net dividends, which is an increase of 129.45% YOY...

...overall, the YOC ratio is now 6.734% and is slowly approaching my targets 👍🏻

》TOP 3《

$ASWM (+4,57 %) +19,09% (+9,64%)

$EVD (+0,35 %) +11,54% (+10,38%)

$YYYY (+1,3 %) +10,14% (-1,18%)

》FLOP 3《

$MUX (+0,74 %) -15,50% (+8,47%)

$DTE (-1,57 %) -14,58% (+0,98%)

$3750 (-1,05 %) -3,83% (+85,05%)

》Acquisitions《

none

》Disposals《

none

》》Conclusion《《

Things can't always go steeply uphill, but as long as the bottom line is that things are going steadily uphill, everything is fine and I wish us all continued success 🤝

+ 1

Chart experts wanted!

Hello everyone, I need help from the chart experts among you!

How do you see the chart development of $EVD (+0,35 %) ?

Where are the supports and resistances?

Many thanks in advance!

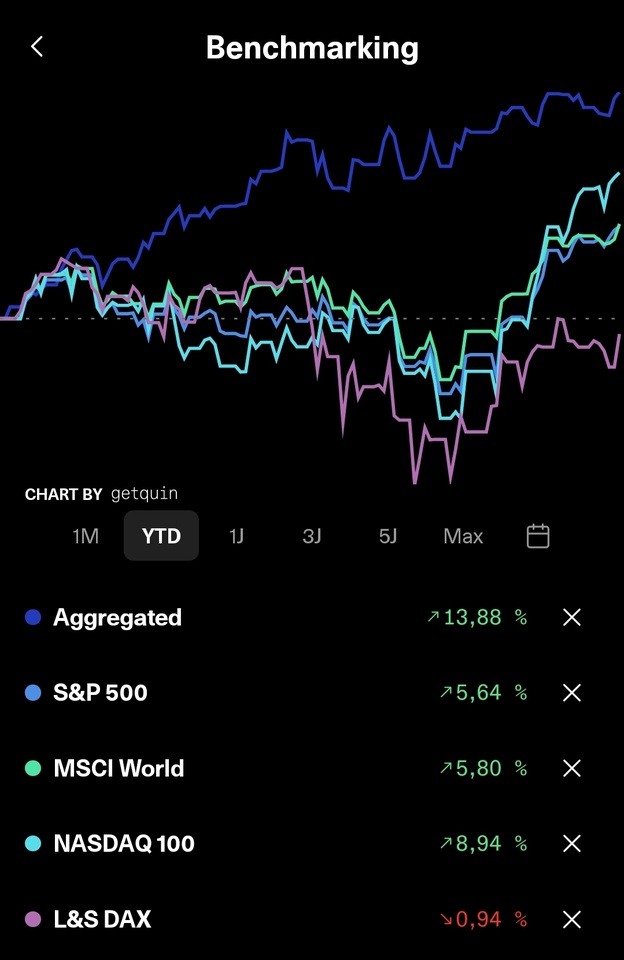

Review of March 2026

What a wild ride that was, please ?!? Even the poor kangaroo gets sick...

🦘📈🦘📉🦘📈🦘📉🦘📈 🦘

...and personally don't really believe that the current situation is the end of "Pinky and the Brain"...

... "Pinky" still has to live up to the bets of all his boddies, has his back to the wall domestically with regard to the mid-terms and "the Brain" still has no interest in the end, after all, he still wants to permanently occupy at least southern Lebanon (incorporate the country) and therefore continues to escalate...

...my conclusion from this is that "Pinky" will launch a limited ground offensive over Easter or shortly afterwards in order to sell it strategically at home or to be able to announce something successful at all, the outcome of which is still completely open, while "the Brain" is already forging plans on how he can continue to pursue his goals even after a possible US exit - the end is open - regardless of the fact that the energy issue will still not be resolved after the end 🤷🏻♂️

But let's get back to March...

...even though the month was difficult, it ended with a small gain on the bottom line or even just below the last ATH...

...shows me, conversely, that my consistent strategy and steady fingers have been able to survive such market phases relatively well so far 💪🏻

In terms of the year as a whole, the first quarter has also been relatively successful for the circumstances and when I think about the fact that the overall portfolio is just ~1.5-2% below my chosen September milestone, the whole thing reassures me immensely or rather... is going better than forecast 🫠

In the long term, of course, everything is still on target and so not only are the nights still calm and cozy, but I also know that the dividends will continue despite everything, which brings us back to the next topic...

》Dividends《

This month there were €116.68 net dividends, which means an increase of 164.41% YOY 💪🏻

YoC (TTM) is ~6% and thus slightly below the target range, although the good months are yet to come...

》Outflows《

$PDI (-0,07 %) (35x)

$VICI (-0,43 %) (35x)

》Accesses《

$ALV (+0,26 %) (5x)

$EVD (+0,35 %) (25x)

$FWRG (+1,32 %) (73x)

》TOP 3《

$3750 (-1,05 %) +28,67% (+89,65%)

$VAR (+2,45 %) +23,61% (+55,54%)

$HAUTO (+3,52 %) +11,31% (+79,18%)

》FLOP 3《

$HSBA (+1,79 %) -8,25% (+45,21%)

$ASWM (+4,57 %) -6,51% (-8,38%)

$MUX (+0,74 %) -5,70% (+27,30%)

Furthermore, all contracts for the continuation of my training were signed and sealed this month, which was also pleasing and comes with a small salary increase 😊

That's all from me for now and I wish us all a successful April

+ 1

CTS Eventim massively undervalued at this price right now 🤷🏻♂️

...after I had already made a first strike earlier, the position was increased by another 10 shares at € 50.90 and at € 49.40 another 5 shares were added.

In my opinion $EVD (+0,35 %) is massively undervalued at this corona price level (2023) and if it slips a little further, I will add to it again.

I have now gone through this scenario with many of my individual stocks and so far they have all performed well, so I am still optimistic that it will continue like this.

Another watchlist candidate gains entry

...think the market reaction is completely exaggerated right now, but the share is now available at the 2023 level 🫠

The shares of ticket marketer CTS Eventim were punished on Friday (March 27) following an outlook that investors found disappointing. The share (50.65 euros; DE0005470306) lost a fifth of its value, making it by far the weakest stock in the MDAX.

The reason for this is the cautious forecast for 2026: CEO Klaus-Peter Schulenberg expects only slight sales and profit growth, analysts had expected more significant increases. The share fell to its lowest level since November 2022, losing over a third of its value since the end of 2025 alone. In 2025, CTS Eventim had recorded a 13% decline in profits despite strong revenue growth of almost 10%. I am currently not invested in CTS Eventim.

CTS Eventim with record sales Profit declines.

CTS Eventim AG, a leading entertainment company, has reported record results for the full year 2025, exceeding the EUR 3 billion revenue mark for the first time.

Despite this success, the company's earnings per share (EPS) fell by 13% year-on-year, mainly due to currency effects and other external factors.

The most important points at a glance

- CTS Eventim's revenue exceeded 3 billion euros for the first time, an increase of 10% compared to the previous year.

- Earnings per share (EPS) fell by 13% to EUR 2.89, influenced by currency effects and special items.

- The company maintained an adjusted EBITDA margin of 19%, which is in line with historical levels.

- Strategic initiatives in the areas of technology and data are expected to drive future growth.

Development of the company

CTS Eventim AG delivered a strong operating performance throughout 2025, achieving significant revenue growth and maintaining a stable EBITDA margin. The company reported total revenue of EUR 3.1 billion, an increase of 10% year-on-year, driven by robust ticket sales and a growing live entertainment segment.

Adjusted EBITDA reached EUR 584 million, which corresponds to growth of 8% compared to the previous year.

Key financial figures at a glance

- Turnover: 3.1 billion euros, +10 % compared to the previous year

- Adjusted EBITDA: 584 million euros, +8% compared to the previous year

- Earnings per share: 2.89 euros, -13% compared to the previous year

- Net result: 277 million euros

- Gross transaction volume: almost 9 billion euros

Outlook and forecast

For the future, CTS Eventim forecasts EPS of EUR 3.7 for 2025 and EUR 4.06 for 2026, with expected revenue of EUR 3.5 billion in 2025 and EUR 3.655 billion in 2026.

The company plans to continue investing in technology and data capabilities to support sustainable growth and improve operational efficiency.

Management commentary

CTS Eventim executives emphasized the company's strategic focus on expanding its global platform and using data to strengthen customer loyalty.

They emphasized the importance of international diversification to reduce dependence on individual markets and events.

Risks and challenges

- Exchange rate volatility remains a significant risk impacting revenues and financial results.

- Dependence on major events and tours could pose a challenge if demand fluctuates.

- Macroeconomic pressures and changes in consumer behavior could impact ticket sales.

- The company's ability to successfully integrate acquisitions and expand its international presence is crucial for sustainable growth.

Q&A

During the earnings call, analysts inquired about the impact of exchange rates on the company's financial performance and the strategic initiatives planned to mitigate these effects. Management reaffirmed its commitment to increasing operational efficiency and developing new revenue streams through investment in innovation and technology.

CTS EVENTIM: Profitable growth in the 3rd quarter

CTS Eventim AG - the leading ticketing and live entertainment

entertainment group and the world's number two, once again grew profitably in the third quarter - despite a challenging economic environment in Germany.

economic environment in Germany.

Revenue and earnings increased year-on-year, although the prior-year quarter included temporary factors.

Profitability developed positively in the 3rd quarter:

The EBITDA margin increased compared to the previous year, even without adjusting for the ongoing integration effects for the Ticketing and

Live Entertainment companies acquired last year.

Other factors were growing synergies

synergies and consistent cost management throughout the Group.

The financial result in the third quarter is positive and has thus improved compared to the same period last year.

In the first 9 months, the financial result

continued to be influenced by the development of the first two quarters.

In the 3rd quarter of 2025, Group sales grew by 3.5% compared to the same

the same period of the previous year to 854.2 million euros.

Adjusted EBITDA rose disproportionately by 13.8% to 137.3 million euros.

The adjusted EBITDA margin was 16.1% (previous year: 14.6%).

Compared to the same period of the previous year, sales in the first three quarters rose

by 6.0% to 2.148 billion euros.

Adjusted EBITDA grew by 4.7% to

percent to 337.9 million euros.

The adjusted EBITDA margin amounted to 15.7% (previous year: 15.9%).

The Ticketing segment continued its growth trajectory despite the fact that the prior-year quarter was additionally boosted by non-recurring revenue, including from the Paris 2024 Olympic Games.

Revenue in the Ticketing segment in Q3 2025 increased by 2.1% compared to the

the same period of the previous year by 2.1% to EUR 211.0 million.

Adjusted EBITDA in the months of July to September grew by 8.1% compared to the

the same quarter of the previous year by 8.1% to EUR 91.0 million.

The adjusted EBITDA margin amounted to 43.1% (previous year: 40.7%).

Based on the months January to September 2025, revenue in the Ticketing segment increased by

Ticketing segment increased by 11.0% year-on-year to EUR 626.8 million.

Adjusted EBITDA grew by 7.1% to EUR 257.8 million.

euros.

The Adjusted EBITDA margin amounted to 41.1% (previous year: 42.6%).

Profitability in the Live Entertainment segment improved significantly in the third quarter.

Revenue increased by 5.5% compared to the same period of the previous

percent and Adjusted EBITDA by 27.0 percent.

This compensated for the decline

EBITDA from the first half of the year (-26.1%) was almost completely

nine-month period was almost completely offset.

In the third quarter of 2025, revenue in the Live Entertainment segment grew to

to EUR 663.0 million compared to the same period of the previous year.

Adjusted EBITDA amounted to

amounted to EUR 46.3 million in the 3rd quarter, which increased the adjusted EBITDA margin to

7.0% (previous year: 5.8%).

Revenue in the Live Entertainment segment increased by 4.2% year-on-year to EUR 1.557 billion in the first nine months of 2025.

At EUR 80.0 million, adjusted EBITDA was almost at the same level as in the

the same period in 2024.

Thanks to the strong 3rd quarter, the Adjusted

EBITDA margin for the first nine months was 5.1%, only slightly below the previous year's

below the previous year's figure of 5.5%.

Outlook:

Based on the robust growth of both segments in the 3rd quarter, the

Executive Board continues to adhere to the forecast made in the 2024 Annual Report

for the Group as a whole for the full year 2025.