Hello my dears,

we are once again traveling to Japan this weekend.

Without further ado, I would like to take you straight to the introduction. Because this one has become a bit longer again.

But maybe not quite so bad at the weekend.

Your opinions and assessments are welcome in the comments.

⚡ Is Kurita a beneficiary of the semiconductor industry?

Yes - one of the most important water infrastructure suppliers for the global chip industry.

Kurita is not just "somehow" active in the semiconductor sector. The company is deeply anchored in the chip production value chain - and the company presentation shows that the electronics sector is the key growth driver.

🧩 The company presentation clearly shows that electronics is the core segment

Kurita names electronics as one of the two main pillars:

"Electronics Industry - Global Expansion of Service Business based on Facility Projects"

This means:

- Pure water (UPW)

- Waste water treatment

- Reclaim systems

- Process water

- Chemicals

- AI-optimized operation

→ All essential for semiconductor factories.

💧 Why semiconductors wouldn't work without Kurita

Chip production is one of the most water-intensive industries in the world:

- Ultrapure water (UPW) for wafer cleaning

- Process water for etching and CMP steps

- Waste water treatment (chemical + biological)

- Reclaim

- cooling water

- Membrane technology

- Chemicals for water quality

Kurita supplies all these systems.

And: Kurita offers "Ultra-pure water supply services" and "AI-optimized operation".

This is a recurring revenue model that is directly linked to the capacity utilization of semiconductor factories.

📈 Figures from the presentation: Electronics is growing strongly

For FY2028, Kurita states:

- 230 billion yen sales in the Electronics segment

- 18% business profit margin

This is the most profitable segment of the entire company

🔥 Why Kurita is a "hidden semiconductor play"

Most investors are looking at ASML, TSMC, Applied Materials. But the infrastructure suppliers like Kurita are:

- less cyclical

- less volatile

- extremely sticky (high switching costs)

- tied to long-term capacity expansions

When TSMC, Samsung, Intel, GlobalFoundries or SMIC build new fabs, they need:

- UPW plants

- Waste water recycling

- chemicals

- Membrane technology

- AI-optimized operations management

→ Kurita earns money from every new Fab project.

🧠 AI + semiconductor = double tailwind

Kurita benefits twice over:

(a) AI boom → more chips → more fabs → more water systems

Every new AI GPU factory (TSMC, Samsung, Intel) needs huge amounts of water.

b) Kurita itself uses AI to increase efficiency

The presentation shows:

- "AI-driven design automation"

- "AI-optimized operation"

This increases margins and scalability.

🌍 Why water is becoming increasingly valuable globally

🔥 a) Water stress is increasing worldwide

The presentation shows that Kurita is already active in 3 critical river basins (Colorado, Citarum, PCJ) and plans to expand to 5 basins by 2028.

You don't do that if there was plenty of water.

📈 b) Industries consume more and more water

Especially:

- Semiconductors

- Batteries / lithium

- Chemicals

- Pharmaceuticals

- food

- Energy

These industries are growing - and with them their water requirements.

🌡️ c) Climate change exacerbates the shortage

Droughts, extreme weather, falling groundwater levels → water is becoming a geopolitical risk.

🏭 Why water is gaining "gold status" in the industry

Water is not just a raw material - it is a production factor without which the modern economy cannot function.

Particularly extreme: the semiconductor industry

A single modern fab (TSMC, Intel, Samsung) requires

- up to 20-60 million liters of water per day

- of which >70% is ultrapure water (UPW)

Kurita is massively active in precisely this segment:

- Global Expansion of Service Business based on Facility Projects

- Focus regions: Japan, Korea, Taiwan, USA, EMEA, India

- Expansion of production capacities

- AI-supported facility planning

This is a direct lever for the semiconductor supercycle.

🧠 Why water is not "gold" - but more important

Gold is:

- rare

- storable

- speculative

- not essential for life

Water is:

- essential for life

- not replaceable

- locally limited

- politically sensitive

- industrially indispensable

- expensive to transport

- extremely regulated

Water is therefore more strategic than gold.

🏁 Conclusion: Yes - water is the new gold. And Kurita is one of the best picks for it.

Why?

- Water is becoming scarcer → value is rising

- Industries need more water → Demand is rising

- Regulation forces recycling → Kurita benefits

- Semiconductor boom → Kurita benefits massively

- AI optimization → Margins increase

- New business areas (PFAS, lithium, space) → Future security

Kurita is not a "water play". Kurita is a water infrastructure champion.

Kurita Water Industries Ltd. is a Japan-based company mainly engaged in the provision of water treatment products, technologies and maintenance services. The company operates in two business segments. The Water Treatment Chemicals segment is engaged in the manufacture and sale of water treatment-related chemicals and related equipment, as well as the provision of maintenance services. The Water Treatment Plants segment is engaged in the manufacture and sale of water treatment plants and equipment, the provision of ultra-pure water, the provision of dry cleaning and precision cleaning services, the cleaning of soil and groundwater and the provision of maintenance services such as the operation and maintenance of water treatment plants.

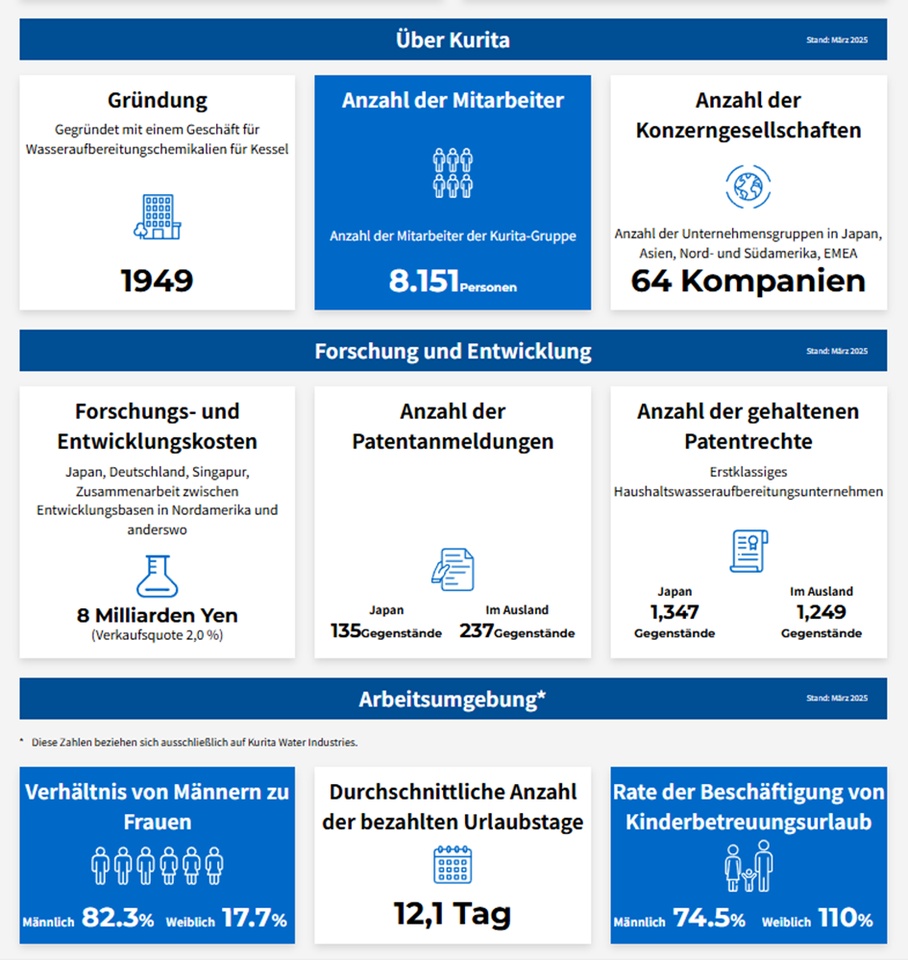

Number of employees: 8,151

Kurita will start operating a local company for the sale of water treatment chemicals in Mexico

March 16, 2026

https://www.kurita-water.com/en/news/20260316-01/

- Geschäft

- Dienstleistungen

- Industrien

- Fallstudien

- Innovation

- Investor Relations

- Managementpolitik

- IR-Bibliothek

- Corporate Governance

- Finanzdaten

- Aktionärsinformationen

- Aktien- und Anleiheinformationen

- Dienstleistungen

- Produkt-/Dienstleistungsindex

- Wasseraufbereitungschemikalien

- Wasseraufbereitungssysteme

- Instandhaltung

- Ultrareine Wasserversorgung

- Technische Reinigung

- Präzisionswerkzeugreinigung

- Betrieb und Wartung

- Boden- und Grundwassersanierung

- Analyse und Tests

- Gewerbliche und Haushaltsprodukte

- Industrien

- Industrieindex

- Elektronik *

- Zellstoff und Papier

- Ölraffination und petrochemische Technik

- Eisen und Stahl

- Automobil

- Essen und Getränke

- Büros und Geschäftsräume

- Macht Power/Industry

- Fallstudien

- Fallstudien-Index

- Kühlturm-Blowdown-Rückgewinnungszystem | China

- CORR-System™ | Japan

- Feiner Dampf | Brasilien

- Wärmepumpe | Japan

- OSCAR | Europa

- S.sensing CS | Japan

- Innovation

- Innovationsindex

- Nachricht vom CTO

- Innovationsgeschichten

- Kurita Innovation Hub

- Basistechnologie

- Aktivitäten im Bereich geistigen Eigentums

- Initiativen für Innovation

*

Kurita Group solutions for the electronics industry

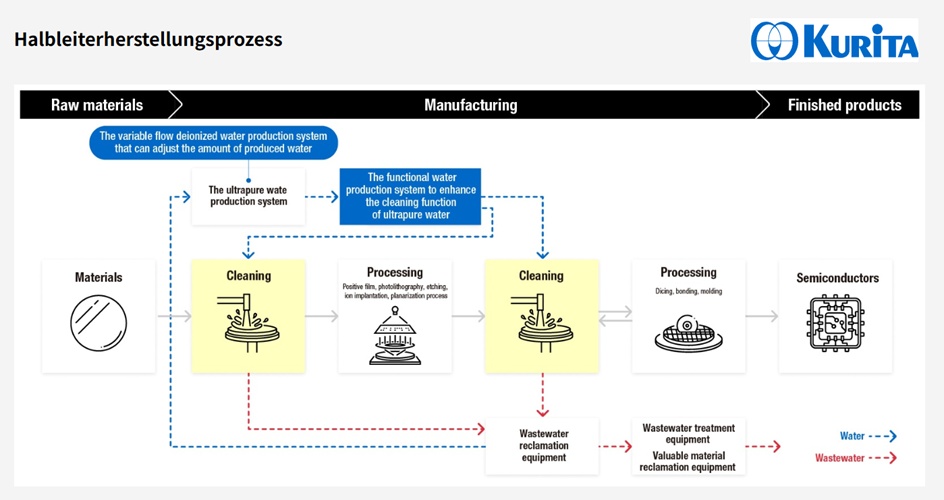

In the production of silicon wafers, semiconductors and various electronic components in precision devices, chemical substances and foreign matter can affect product yield. Therefore, a purification process is essential to remove chemical substances and foreign matter, using ultra-pure water that is as close as possible to pure H₂O, or functional water in which chemicals or gases are dissolved. Kurita Group provides an ultra-pure water production system and a functional water production system that combines pretreatment equipment (such as filters), deionized water production system (such as reverse osmosis (RO) membranes and ion exchange resin towers), and subsystems (such as UV sterilization equipment and UF membranes). In addition, the Kurita Group offers treatment plants for the treatment of organic and inorganic wastewater, wastewater treatment plants for the recovery and collection of water, and equipment for the recovery and reuse of phosphoric acid, hydrofluoric acid and other substances in wastewater.

Segment strategies

📡 Electronics industry

- Expansion of global engineering and production capacities

- M&A to strengthen value creation

- AI-supported design and process optimization

🏭 General industry

- Focus on emerging markets (India, Africa, Middle East, Latin America)

- CSV share of sales to be increased to ~30% increase

Presentation of Shareholder Relations Meeting for the Fiscal Year Ending March 31, 2026

Vision & sustainability focus

- Vision 2030: "Pioneering new value for water" - Sustainable water management, decarbonization, circular economy.

- Materiality focus areas:

- Securing water resources

- decarbonization

- circular economy

- Innovation, human resources, quality & compliance

🔑 Strategic pillars

- Global expansion of the service business (primarily electronics industry)

- CSV business expansion (Shared Value)

- New business areas:

- PFAS removal

- Direct Lithium Extraction (DLE)

- Water recycling for space applications

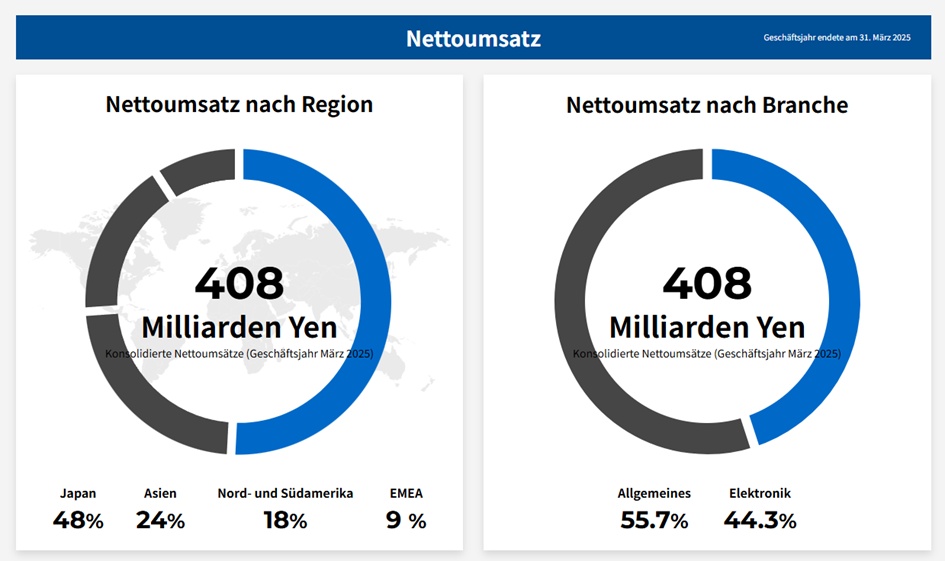

Sales distribution by business segment:

(2025 JPY)

General Water Treatment Market 228 billion

Electronic Market 181 billion

Geographical distribution of sales:

(2025 JPY)

Japan 197 bn

Asia 99.64 bn

North and South America 74.13 bn

Europe, The Middle East, and The Africa 38.49 bn.

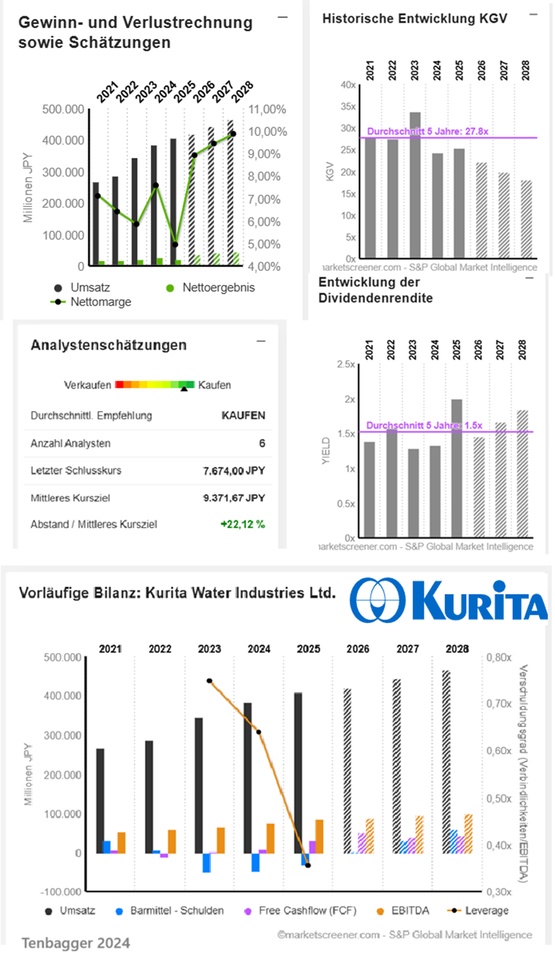

JPY in millions

Estimates

Year Turnover Change

2025 408.888 6,25 %

2026 420.033 2,73 %

2027 444.450 5,81 %

2028 466.167 4,89 %

Year EBIT Change

2025 31.275 -24,15 %

2026 54.660 74,77 %

2027 61.080 11,75 %

2028 66.900 9,53 %

Year Net result Change

2025 20.305 -30,44 %

2026 37.547 84,92 %

2027 41.979 11,8 %

2028 45.977 9,53 %

Year Net debt CAPEX

2025 30.519 56.150

2026 -1.250 22.467

2027 -30.600 32.500

2028 -58.350 36.667

Year EBIT margin ROE

2025 7,65 % 6,1 %

2026 13,01 % 10,98 %

2027 13,74 % 11,64 %

2028 14,35 % 11,81 %

Year Earnings per share Change

2025 180,7 -30,44 %

2026 343,4 90,1 %

2027 385,1 12,12 %

2028 423 9,85 %

Year Dividend p share Return

2025 92 2 %

2026 112 1,46 %

2027 128,2 1,67 %

2028 140,8 1,84 %

Year FCF Yield

2025 5,78 %

2026 5,9 %

2027 5 %

2028 5,58 %

Year P/E ratio PEG

2025 25.4x 1.53x -0.8x

2026 22.3x 2.39x 0.2x

2027 19.9x 2.21x 1.6x

2028 18.1x 2.05x 1.84x

Market value 839,743

Number of shares (in thousands) 109,427

Date of publication 08.05.2025

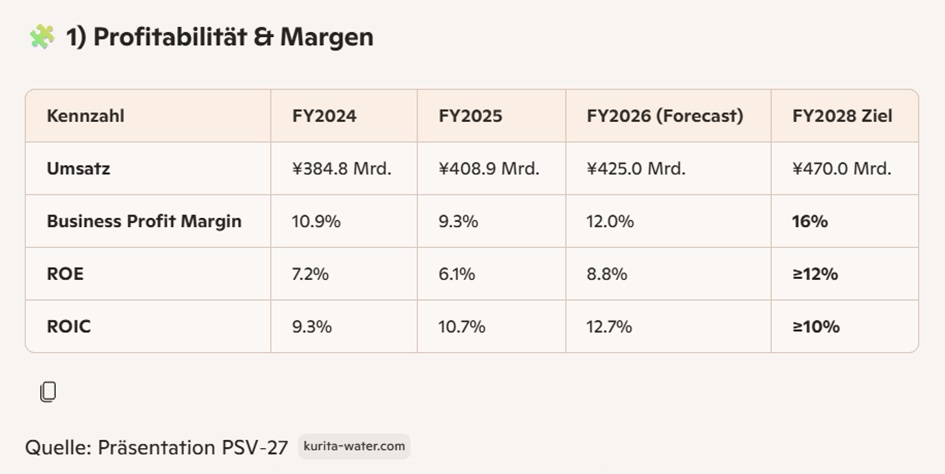

Interpretation:

- Margins rise significantly again FY2026.

- ROIC already above target → capital allocation efficient.

- ROE still low, but expected to rise sharply.

Segment targets:

- Electronics: 230 bn sales, 18% margin

- General Industry240 billion sales, 14% margin

- CSV share increases to ~30% by FY2028

Source: Segment strategy & big picture PSV-27

🎯 Financial targets until FY2028

- Sales: ¥470 bn.

- Business profit margin: 16%

- ROE: ≥12%

- ROIC: ≥10%

Financial strategy & shareholder returns

- ROIC-based capital allocation

- Combination of organic growth, M&A and technology acquisitions

- Dividend increase for 22 years in a row

- Flexible share buybacks (FY2026: 2.79 million shares)