The good @Tenbagger2024 has in his contribution Das Leben ist wie eine Schachtel Pralinen Man weiß nie was man kriegt a joint dividend carryforward. As this is difficult to implement in practice, I'll start with my figures from March and add a short report on how the first quarter went. This is followed by a few more insights into my investment approach.

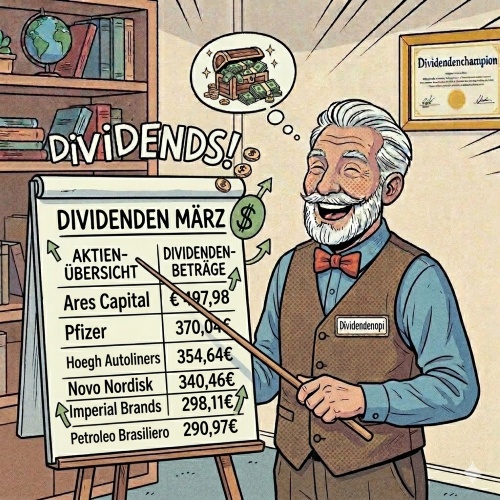

In March, I received a total of € 2,345.17 gross in dividends from 7 distributions. The month is therefore on average for what my pure dividend share portfolio regularly yields. You can find the strongest payers on the table in the picture above, plus my EM dividend ETF also paid out.

According to GQ-Rewind, my time-weighted return in March was minus 0.09%, which is somewhere in the middle of the average. So far so good.

The first quarter was dominated by the war in Iran and had already seen some turbulence before that. From this point of view, I am more than satisfied that my portfolio has gained 9.52% YTD. These YTD figures are up to and including 02.04.2026.

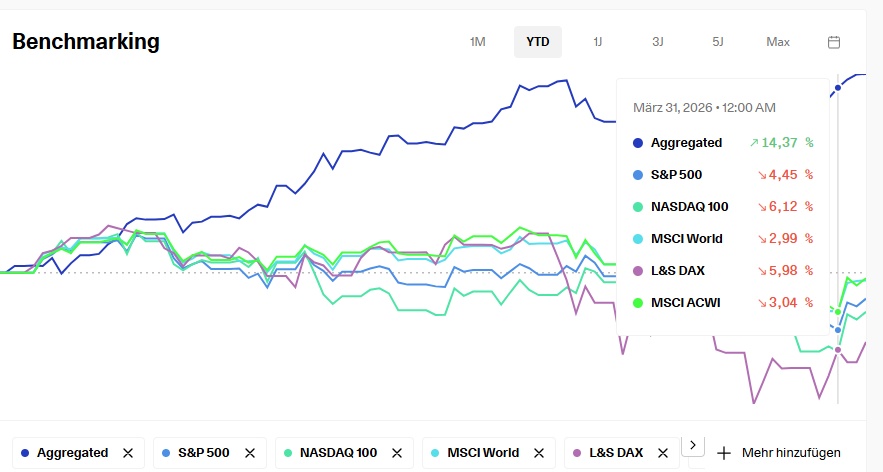

For the overall performance for the benchmark, I took YTD to 31.03.2026, 12:00 noon. And here I am clearly ahead with 14.37% and clearly beat corresponding indices as you can see in the following picture.

This has made it relatively easy for me to deal with the market fluctuations in recent months under the aforementioned circumstances. But I don't have to hide my overall performance in the longer term either. For 1 year and 3 years I am also ahead, only when looking at 5 years do I have to admit defeat to the Nasdaq 100, all others are behind.

And that brings us to the crucial point for me. My investment strategy. I can sleep peacefully in pretty much all market phases without having to get into an operational frenzy, and I have the psychological advantage of the relatively predictable cash flow that comes even when prices fall.

Here I go into more detail on the contribution by @Tenbagger2024

Wer die Wahl hat hat die Qual in more detail.

Lest we misunderstand each other, my approach is certainly not the Holy Grail for relaxed investing, but is purely due to my personal life situation. If you are young and still have an investment horizon of 20 or 30 years, then you have significantly more opportunities for stable wealth accumulation with growth stocks or ETFs. However, you also have to put up with price fluctuations. Perhaps some of you will still find an idea to take some risk out of your portfolio and stay a little calmer in turbulent phases.

How am I currently positioned as at the beginning of 04/2026? My capital is currently 35% in equities, 25% in some bonds and mostly fixed-coupon certificates and 40% in cash.

Cash is quickly described, a quarter in fixed-term deposits, the rest in overnight money hopping with currently 3.25% BBVA, 3.4% Consorsbank and 3.35% Advanziabank, conditions for overnight money fixed until the end of the first half of the year. After that, the search continues. Apart from Consorsbank, the other two pay interest monthly. I also receive the interest on my fixed-term deposit regularly every month via Ford Money. Plannable cash flow month after month at the price of constantly having to open and close accounts. But always better than with most house banks or neo-brokers.

I still have old federal bonds with a coupon of more than 6% and the rest is defined by express certificates with a fixed coupon. The bonds pay out once a year, one at the beginning of January. This has the positive side effect that my tax-free allowance is fully utilized immediately and I no longer have the withholding tax problem with all US dividends. The express certificates all relate to shares that I do not actively hold in my portfolio. As the name suggests, they pay fixed interest. This is paid quarterly and, depending on the certificate, is between 8% and 11.7% p.a. Maturities are usually 18 to 30 months. No matter what the stock markets do or how the individual shares perform, the cash flow comes. Sounds great at first, and it is during the term. The risk lies at the end, on the final valuation date. There, the underlying should not be below the corresponding barrier. This is usually 40 to 50% below the price on the fixing date. Of course, this requires a corresponding valuation and selection of the underlyings. I currently hold certificates on Renk, Hensoldt, Vonovia, BMW, LVMH, Nvidia, Infineon and Heidelberg Materials. New issues that I have subscribed to for the beginning of April are Banco Santander, MTU and Rheinmetall. This is an overview of what I am investing in indirectly.

You can see the current composition of the 25 stocks in my portfolio in my profile. In principle, I invest between 1% and max. 2% of my total capital in the respective shares, and I weight them accordingly via the purchase price. The purchase price also determines my total dividend yield. Measured against my current investments, I achieve a gross return of 8.90% on the capital invested with the dividends already paid and expected in 2026. The different weightings in my portfolio therefore result from the different price gains. My largest position at the moment, $BATS (-0.83%) currently contains over 50% price gains and is fully invested. Dividend yield measured against the buy-in is well over 8% gross p.a. I am currently only fully invested in 2 stocks. I usually buy in 3 or 4 tranches spread over several months in different market phases. Under no circumstances do I select my shares according to a buy and hold forever principle. That's not possible with high yield. I have to keep a close eye on the "narrow" positions at all times. High dividends are not always a good sign and can also be cut quickly. If a negative trend proves to be sustainable, we restructure. The weighting is reduced and another stock from the same sector is added to the portfolio, or the stock is removed completely. My buy and hold a while motto....

My portfolio is significantly overweighted in the EU/UK at around 60%, with 25% in the USA and the rest in Latin America and Asia. Within Europe, the most represented countries besides the UK are D, NO, DK, A, NL, BE and Sweden. Consumer staples - clearly dominated by tobacco - and financial services are the largest sectors, followed by materials, energy, healthcare, communications and industry.

The primary objective is to preserve capital with a corresponding cash flow. For this reason, I am happy about price gains, the distance to the loss zone increases accordingly and I let the shares run without regularly evaluating the value. As long as there are no serious changes in the earnings situation or even a reduction in dividends, these stocks remain on the fringes of the radar. For the rest, or for new stocks, I set a tight SL to be reasonably protected against the risk of losses and monitor developments more closely.

And of course, sometimes my fingers itch. To this end, I have set myself a limited budget of a maximum of 5% of my total capital to realize short-term trades. These are held in a separate portfolio. These are stocks from the biotech, information technology and commodities sectors, which of course do not pay dividends. This prevents me from getting the wrong idea if I invest too much.

I've also been holding some physical gold for a few years to enjoy the shine 😉

As I'm still a bit at war with AI, this is a rustic compilation of my goals and results. Please forgive me for that. If you have any general or in-depth questions about individual points, please feel free to ask in the comments.

I wish us all a successful new trading week!