In today's episode of our series on stocks with 20% CAGR potential, we take a look at a company that is currently suffering badly from the general software sell-off - but wrongly so, in our view: ServiceNow $NOW (-0,54%) as $MSFT (+1,63%) and $CSU (+1,54%)

---

The thesis: Indispensability beats AI fear

The market currently fears that language models such as Claude could replace traditional software solutions. But this view falls far short of the mark.

Why?

1. high barriers to change

ServiceNow's customers are large global corporations. In theory, these companies would have the resources to develop their own solutions - but they consciously decide against it.

ServiceNow offers:

- Standardized processes

- Extremely high reliability

- Deep integration into existing systems

If you run your entire IT service management (ITSM) via ServiceNow, you can't simply replace it with a chatbot.

---

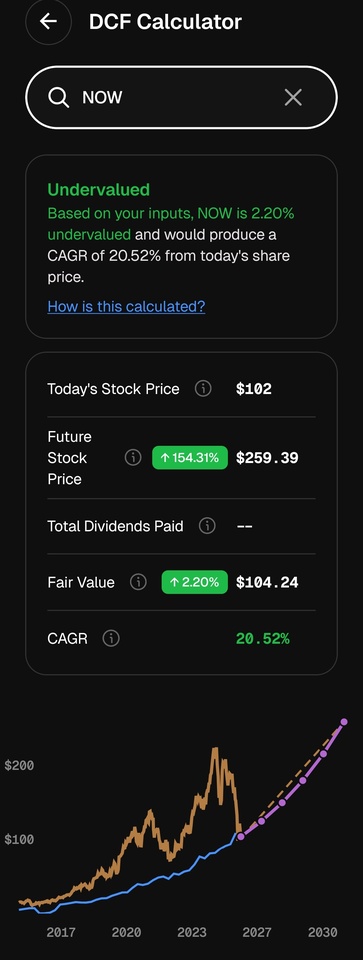

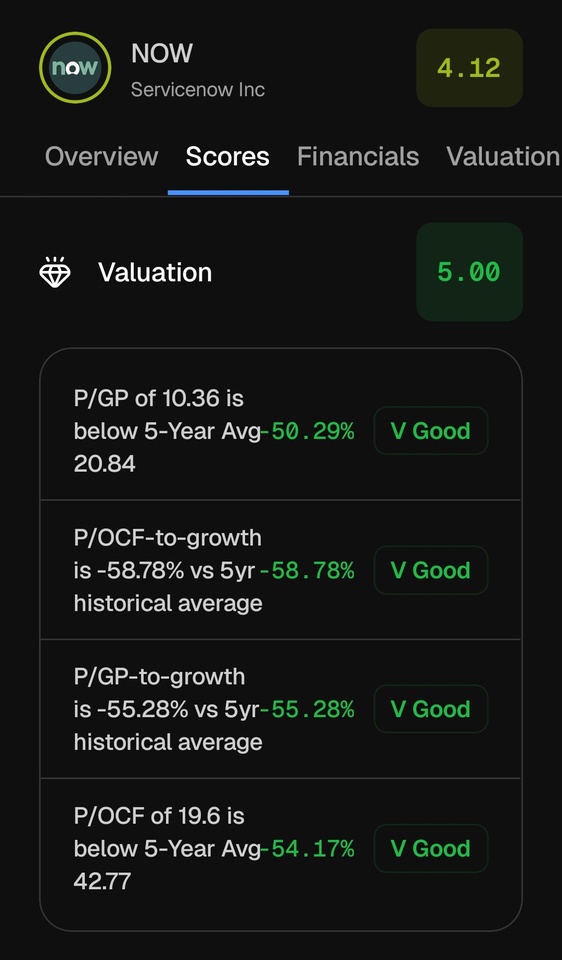

2. historically attractive valuation

- Current P/E: 48

forward 24

- 5-year average: 74.1

- Decline: -35.5

➡️ The share is valued more favorably than it has been for years - despite stable operating performance.

---

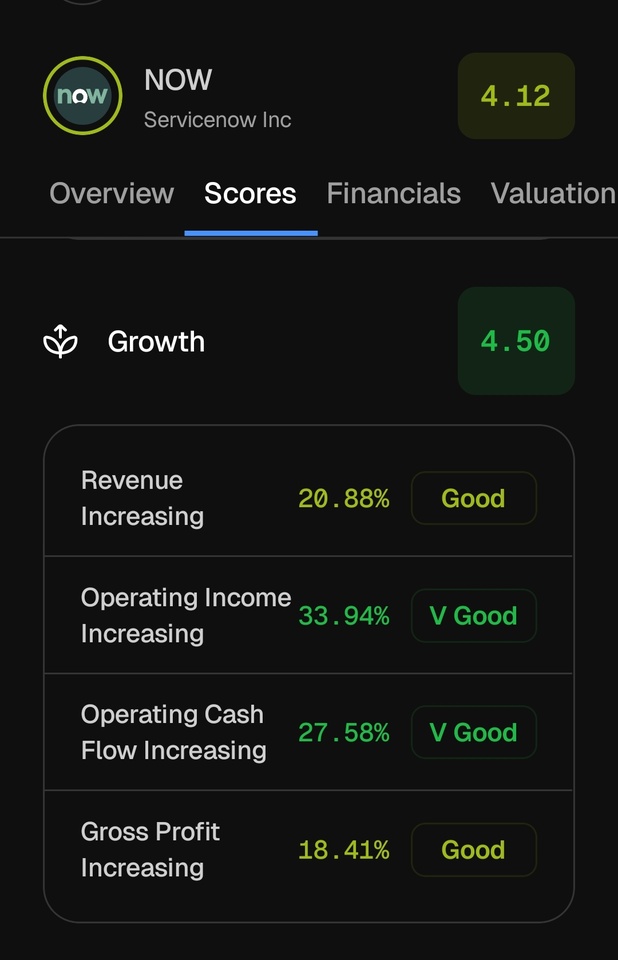

3. strong growth momentum

- Sales growth: ~23.8 %

In combination with the valuation, this results in a:

- PEG ratio of approx. 1

➡️ For a company of this quality in the software sector, this is a clear undervaluation signal.

---

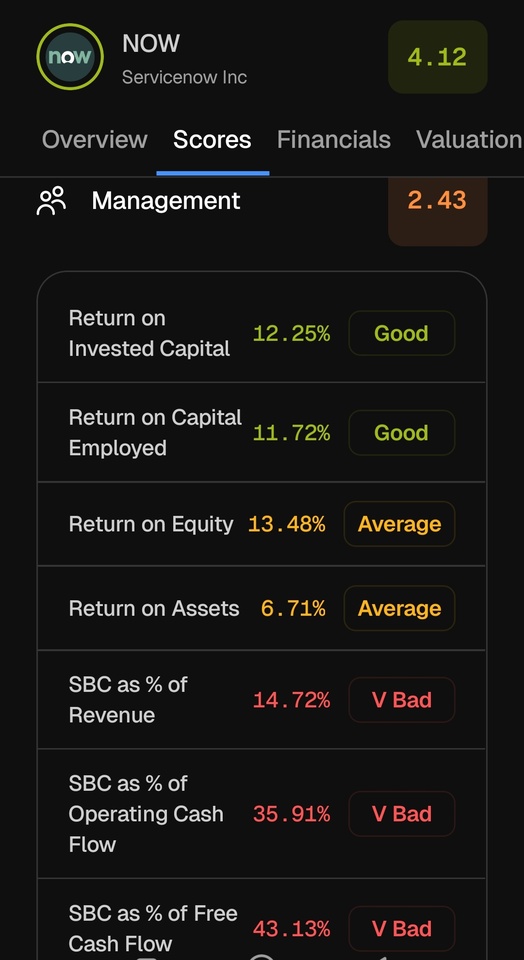

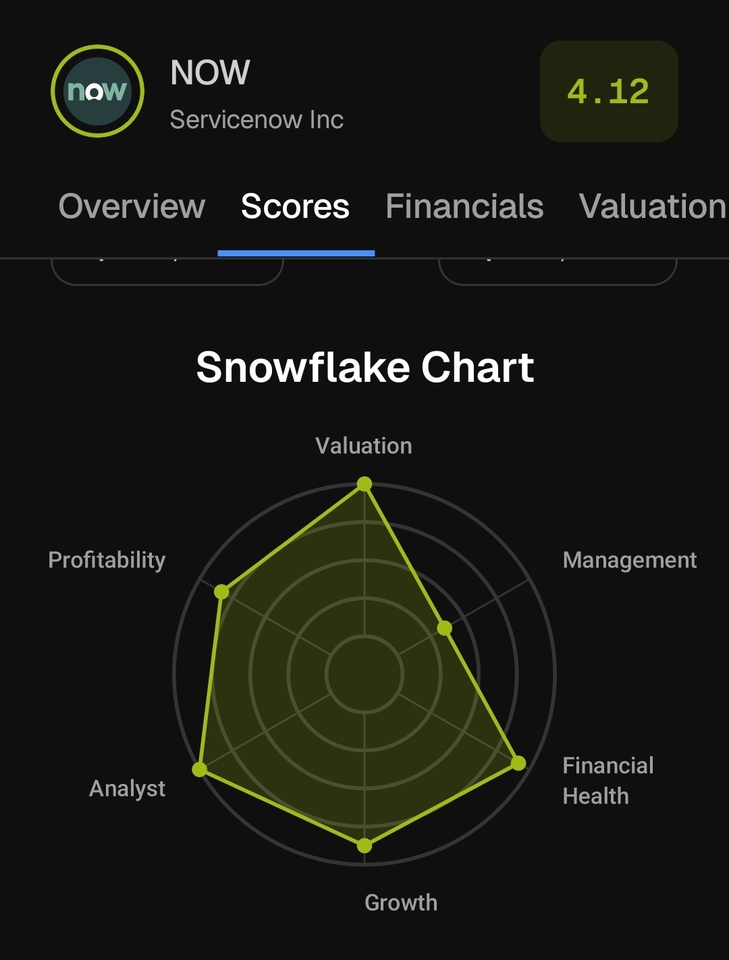

4. excellent operational quality

- Growth score: 4.40

➡️ ServiceNow consistently delivers at a top level - both strategically and operationally.

---

Pros & Cons: ServiceNow (NOW)

Opportunities

AI as an amplifier, not a substitute

ServiceNow actively integrates generative AI into its platform.

➡️ More likely: AI makes ServiceNow more valuable, not superfluous.

Extremely high customer loyalty

- Renewal rate: >97 %

➡️ Predictable, recurring revenue at the highest level

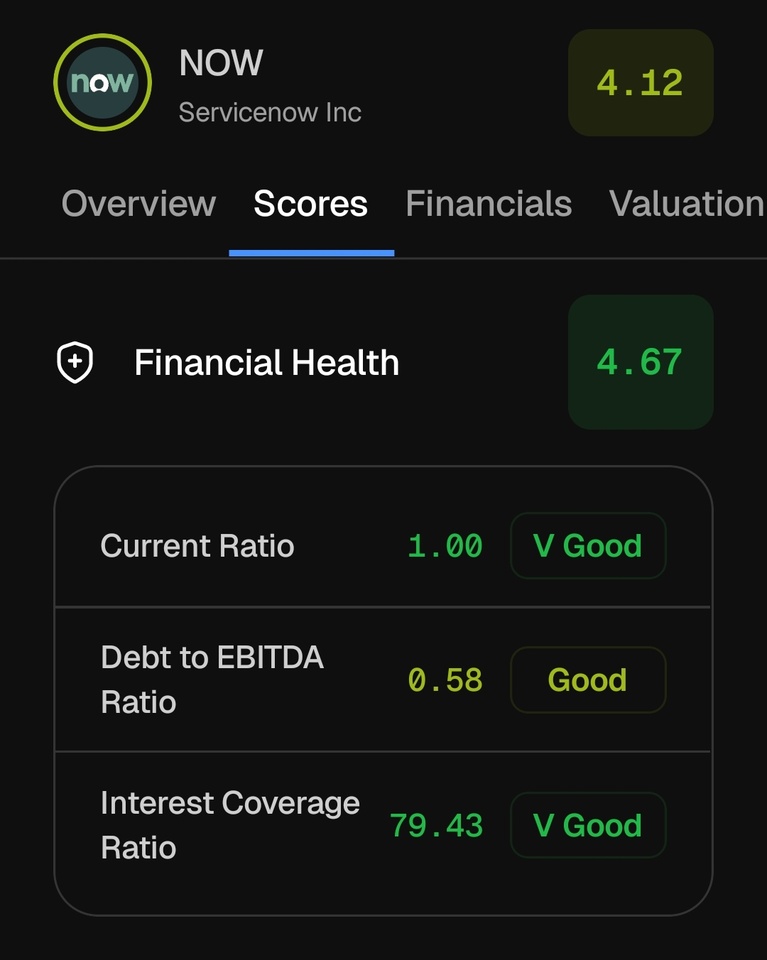

High profitability

- Net margin: ~20 %

- Increasing free cash flow

➡️ Highly scalable, very profitable business model

---

Risks

Negative sentiment in the software sector

➡️ In the short term, strong figures can be ignored by the market

Long sales cycles

➡️ Major projects could be postponed in uncertain times

Valuation remains challenging

➡️ A P/E of ~47 remains high for classic value investors

→ The company must deliver operationally

---

Conclusion: infrastructure instead of hype

ServiceNow is not a short-term AI hype play, but a fundamental infrastructure investment for the digital transformation of global corporations.

The current market anxiety surrounding AI offers a rare opportunity:

- PEG ~1

- Significant discount to historical valuation

- Strong, predictable growth

➡️ A combination that you rarely get with a quality company.

I am not invested.

Closing question

Can an AI really replace the complex workflows of a global corporation - or are we seeing a classic market overreaction here?

https://youtu.be/diVdq9Ss8Mc?is=KAaUEnnMZnsMYaxp

A detailed analysis in English