It's great to see what's happening with the retirement savings scheme. Finally something that really feels like progress and not like the umpteenth half-hearted solution from politicians, even if it comes 10 years too late.

Compared to a normal custody account or simply leaving money in an account, the custody account makes a difference.

In short: This is a state-subsidized custody account in which you invest money (gross), even as a self-employed person, and receive tax benefits in return, which means that you end up with more left over for yourself by investing pre-tax (gross) and receiving a state subsidy!

Subsidies:

- For deposits of up to 360 euros per year, the state subsidy is 50 cents for every euro deposited, i.e. a maximum of 180 euros per year.

- For deposits between €360 and €1,800 per year, the state subsidy is 25 cents for every euro paid in, i.e. a maximum of a further €360 per year.

+Subsidies/supplements for children

Especially if you think about simply putting in €150 a month (maximum subsidy) or filling up the €1,800 once a year (directly in January), you'll add up to a brutal amount over the years.

You have to be honest: you haven't seen anything like this from politicians for a long time.

But as always, in the end it's the costs that decide whether it's really worth it.

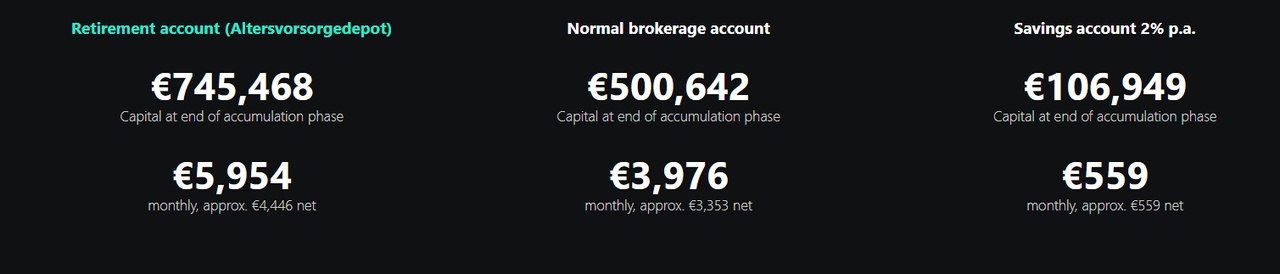

Example result for JG 2003, and 180EUR per month. You can also play around with Scalalbe: https://de.scalable.capital/en/retirement-account?fbclid=PAZXh0bgNhZW0CMTEAc3J0YwZhcHBfaWQPNTY3MDY3MzQzMzUyNDI3AAGnvCANxIg1t8QwbSAfc9Yo0wIDheuewP6nJMOHlivlPOflIBUGUutfGIRrZe4_aem_lrZx8swAdYWSSoJXin_agg

If the framework conditions remain the same, I would take the maximum subsidy, and I assume that the neobrokers will charge very good fees on the market.