Hello everyone!

My trusty AI assistant "Mister Prompt" and I have been virtually exploring the depths of the Scandinavian forests to find great companies and have found an example of Scandinavian investment in Sweden.

My trusty AI assistant "Mister Prompt" introduced me to this absolute gem, which is still completely new here in the forum - there hasn't been a single post about it yet! He made the share so appealing to me that I bought and invested today.

As we often have a strong US bias when it comes to REITs, I would like to introduce you to Cibus Nordic Real Estate

$CIBUS (+1,3%) in detail. A real monthly payer from Scandinavia with a reasonable dividend and a fair price!

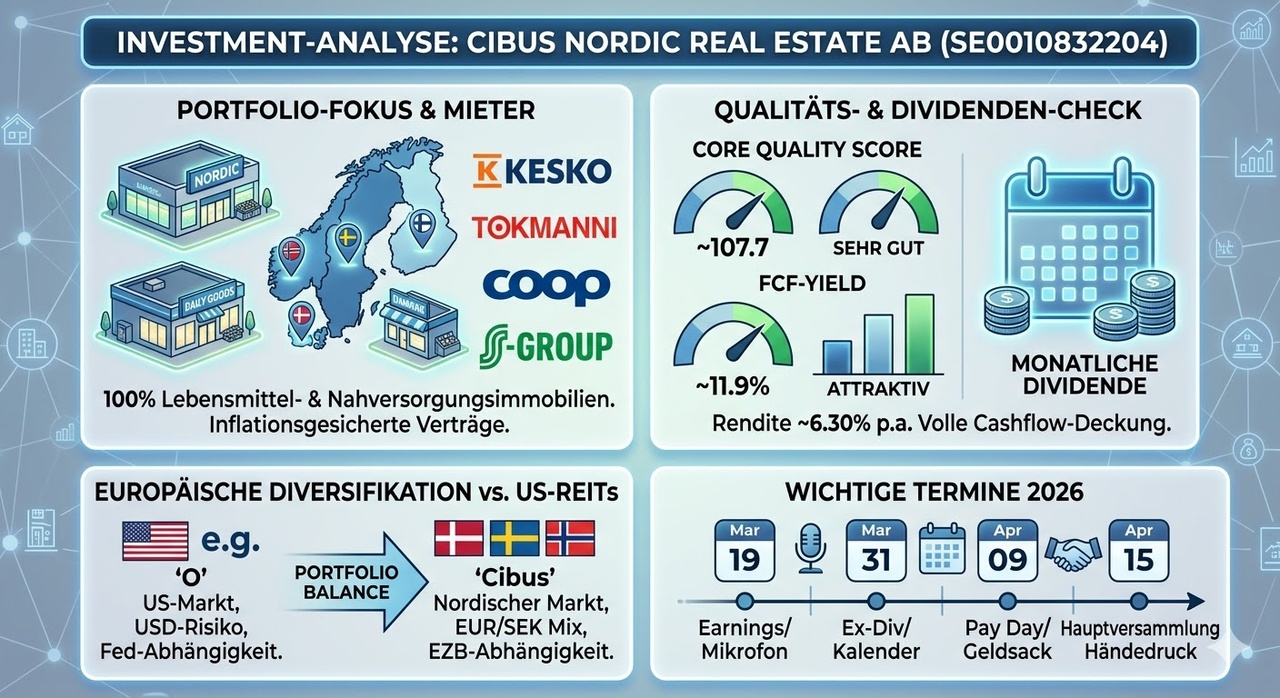

🏢 Who is Cibus Nordic and who are its customers?

Cibus Nordic Real Estate AB is a Swedish real estate holding company that specializes in an absolutely crisis-proof segment: Supermarkets and grocery stores. People always eat!

The properties are located in the Nordic countries (Sweden, Finland, Norway, Denmark). The anchor tenants include the largest and most creditworthy supermarket chains in Scandinavia, including Kesko, Tokmanni, Coop and the S-Group. This means that almost 100 % of rental income comes from the food retail sector. In contrast to vulnerable office or fashion retail properties, this business model is extremely resilient to economic fluctuations.

📊 The valuation dashboard (as at March 13, 2026)

The current share price is approx. 145 SEK with a market capitalization of approx. EUR 1.16 billion. Here is a quick look at the most important metrics for our analysis:

============================================================

📉 CURRENT KEY VALUATION FIGURES

============================================================

▶ P/E ratio (price-earnings ratio) : 12.55

▶ KCV (price-cash flow ratio) : 8.29

▶ P/E ratio (price-sales ratio) : 5.96

▶ P/B ratio (price-book value ratio) : 1.09

▶ Dividend yield : ~ 7 %

============================================================

🔬 The quality and formula check

We run Cibus through our strict quality filters to see whether the foundation is really strong or whether it's just balance sheet cosmetics:

1. core quality formula (sales growth + operating margin = score)

- Growth & Margin: TTM sales growth is a strong 32.9%. The operating margin is gigantic at around 74.8 % (typical for strong real estate owners).

- According to the 2025 annual report, rental income has risen by a fantastic 36 % (to EUR 166.7 million).

- Result: A score of 107,7.

- Conclusion: According to the rule of thumb, anything > 25 is "very good". Cibus is growing enormously in terms of quality and is playing in a league of its own, far removed from insubstantial "story stocks".

[ CORE QUALITY SCORE METER ]

< 15 (Schwach) | 15-25 (Solide) | > 25 (Very good)

---------------------------------------------------

⭐⭐⭐ 107,7 !

2. cash flow quality formula (FCF yield = free cash flow / market cap)

- FCF yield: The free cash flow yield is currently around 11,9 %.

- Conclusion: From 8 % we speak of "very attractive". Cibus is proving to be a real cash machine.

- Cibus has generated around EUR 128.5m in free cash flow in the last 12 months.

3. dividend filter (income core)

- Review: Minimum yield >= 3.5% and full coverage by cash flow (no pseudo dividend on credit).

- Result: With approx. 7 % yield the minimum target is easily achieved. The payout ratio on the cash flow is a conservative ~57 %. The dividend is easily covered by the real cash inflow.

- At today's share price of 145.35 SEK (equivalent to approx. EUR 12.75), this corresponds to a dividend yield of a strong 7.0 % p.a.

- Distribution amount: With around 82 million shares, the EUR 0.90 dividend costs the company around EUR 73.8 million.

Important special feature: Although Cibus is traded on the Swedish stock exchange in SEK, they pay out the dividend in euros (EUR)! This saves currency conversion fees on the distribution.

4. the hard exclusion rule

No stagnating sales, margin is consistently above 5%, dividend is covered by cash flow and the sober figures underpin the business model. The share passes our filtering absolutely flawlessly.

Other facts:

- Occupancy rate (economic occupancy rate): Cibus reports an extremely strong occupancy rate at the end of 2025 of 95,7 %.

- Tenant structure: 95% of the properties have major food retailers as anchor tenants.

- Interest rates: The average interest rate on their debt capital is below 4% (3.9%) following recent refinancings.

🆚 Comparison with US REITs (the realty income effect)

Why buy Cibus if you also have Realty Income (O) or Agree Realty (ADC) in your portfolio?

The answer is: Diversification of dependencies. If you only hold American REITs, you are completely dependent on the interest rate cycle of the US Federal Reserve (Fed), the health of the US commercial real estate market and the US dollar.

Cibus brings the beloved charm of the monthly dividend to our portfolio, but diversifies us into the robust Scandinavian market. You decouple from the US macro cycles and instead focus on the ECB and Riksbank environment. An excellent European satellite for the Income portfolio!

📅 Important upcoming dates

If you want to position yourself directly, you should keep an eye on the dates in the coming weeks:

- March 19, 2026: Publication of the next earnings report.

- March 30/31, 2026: Next ex-dividend day for the upcoming monthly distribution.

- April 09/10, 2026: Payment date (pay date) of the dividend.

- April 15, 2026: The Annual Annual General Meeting (AGM) in Stockholm. Traditionally, the exact distribution plan for the monthly tranches of the coming 12 months is also formally approved here.

⚖️ Opportunities and risks

Opportunities:

- Profiteer from interest rate cuts: Real estate shares have suffered from the interest rate environment in recent years. If interest rates in Europe continue to fall, the intrinsic value of the portfolio (NAV) is likely to continue to develop positively.

- Inflation protection: Contracts with supermarket chains in Scandinavia are usually linked to inflation (CPI). If prices rise, rental income also rises almost mechanically.

Risks:

- Refinancing risk: Like all real estate stocks, Cibus operates with borrowed capital (debt/equity is around 155%). The interest rate environment must always be monitored for future follow-up financing.

- Currency risk: The company primarily reports and quotes in Swedish kronor (SEK). However, some of the properties are located and generate rents in the eurozone (Finland) as well as in Denmark (DKK) and Norway (NOK). This inevitably leads to currency fluctuations in the balance sheet.

My conclusion: A fundamentally strong, rock-solid building block to Europeanize one's monthly cash flow portfolio. At current prices, a wonderful opportunity with substance!

I look forward to hearing your opinions. Has anyone had the share on their watchlist or even in their portfolio for some time?

Best regards and happy investing! 📈

@Dividendenopi

@Tenbagger2024

@Get_Rich_or_Die_Tryin

@Multibagger