Since 2020, I’ve received 55% of my investment back in dividends, plus another 50% in shares of Daimler Truck, its spin-off. The stock is basically at the same price. $MBG (+2,61%)

I was lucky enough to sell just before last week’s sharp declines, but my decision to sell had nothing to do with the market; it’s something I’ve been considering for a while.

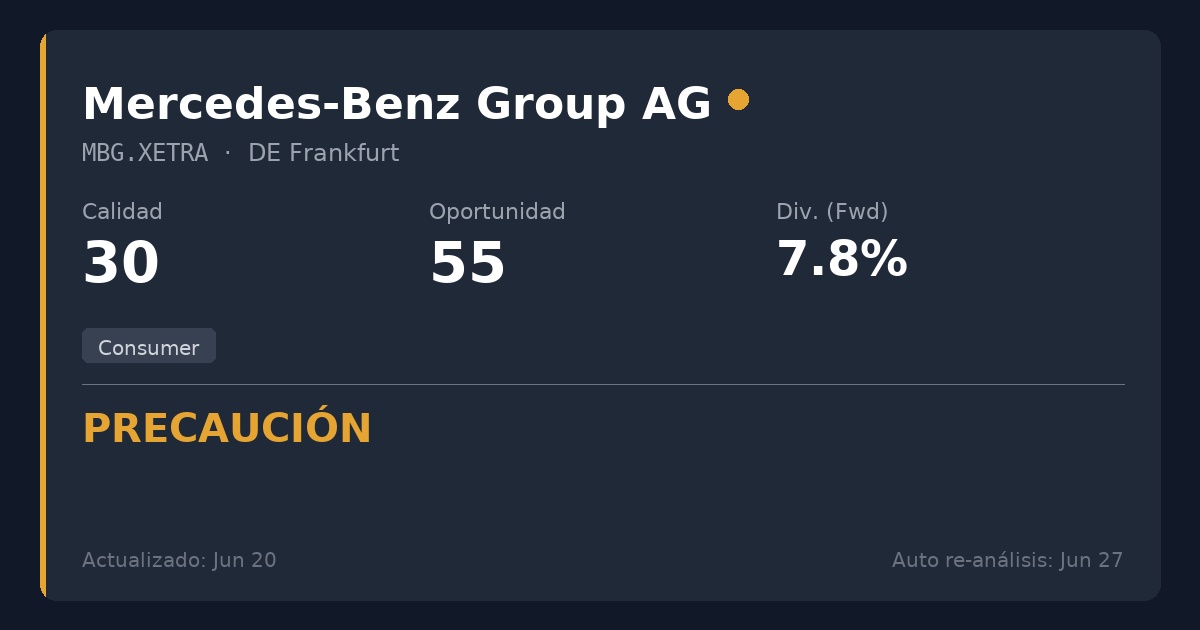

My algorithm places it in the 🟠caution quadrant, disqualifying it from the dividend investment strategy we propose: oligopolies or monopolies in essential services with predictable cash flows that will still be around in 20 years.

Here are the reasons:

📉Very low quality (30/100). The automotive business is ultra-cyclical, capital-intensive, and subject to constant technological obsolescence. It doesn’t fit into a conservative dividend strategy.

📉 Recurring dividend cuts. It cut the dividend in 2025 and is proposing another cut in 2026. A company that cuts dividends two years in a row is not a reliable source of income.

📉 Severe structural deterioration. EPS (earnings per share) has shown negative growth of -24.9% on an annualized basis over the past 5 years. Margins are constantly shrinking.

📉 Very high debt. Net debt to EBITDA stands at 6.22x—well above the 3x limit required by my strategy.