Hello dear community,

Today I would like to introduce you to another company from the healthcare sector. Let's stay on European soil and take a look at our neighbors in Belgium.

Today's presentation is all about "Union Chimique Belge" $UCB (+0,2%)

🧬 UCB SA $UCB (+0,2%)

: The resurrected growth machine of global biopharma

UCB (Union Chimique Belge) $UCB (+0,2%) is not a sluggish pharmaceutical giant that only milks old patents. It is one of the best-positioned biotech companies in Europe that has not only survived the painful loss of its billion-dollar blockbuster Vimpat, but has turned it around into an unprecedented phase of operational growth. While two years ago the market was still in doubt about the approval pipeline, UCB $UCB (+0,2%) set the course for a decade of protected growth. Its focus is on highly effective, immunological and neurological niche therapies for serious diseases - far removed from interchangeable mass-produced generics.

1. the business model: the 5-pillar growth rocket 🔬💉📈

UCB $UCB (+0,2%) has radically rejuvenated its entire business model and controls the market for specialty therapies with a state-of-the-art product portfolio:

-The global platform blockbuster (Bimzelx®): As the first dual IL-17A and IL-17F inhibitor, Bimzelx is the competition's technological nightmare. It sets new clinical standards in psoriasis and is aggressively taking market share from top dogs such as AbbVies $ABBV (+0,41%) Skyrizi - freshly underpinned by the latest head-to-head study data (BE BOLD), which prove its clear superiority.

💉Bimzelx® (bimekizumab):

USA: Until 2035 (without optional patent extensions).

Europe: Until 2036.

This means that there is no danger from copycat products (biosimilars) for at least another 10 years.

-The rare neurology double hit (Rystiggo® & Zilbrysq®): In the rare neuromuscular disease myasthenia gravis (gMG), UCB $UCB (+0,2%) strategically occupies the market twice - once with a monoclonal antibody and once with a subcutaneous peptide. This allows them to cover almost all patient needs at the same time.

💉Rystiggo® (rozanolixizumab):

Europe: Until 2034

USA: Until 2035

Japan: By 2037

💉Zilbrysq® (Zilucoplan):

Europe & USA: Until 2035

Japan: Until 2040

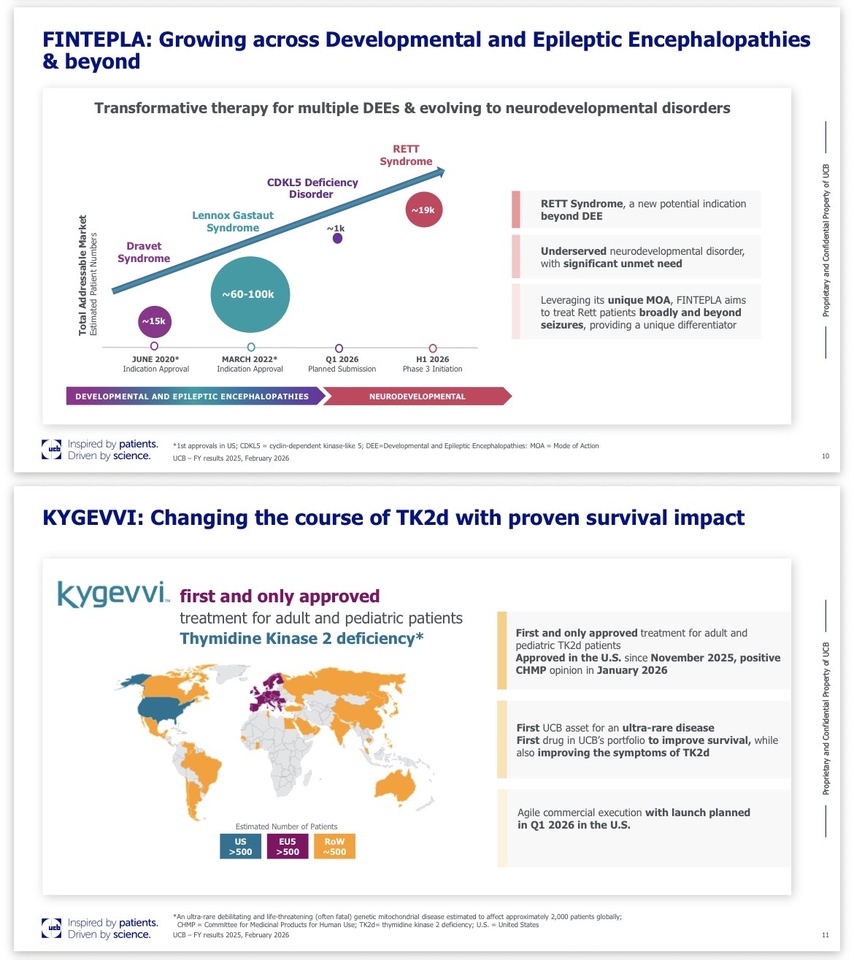

-Orphan Drug Premium Pricing (Fintepla® & Kygevvi™): With Fintepla in rare forms of epilepsy and the brand new 2026 US approval for Kygevvi (therapy for ultra-rare TK2 deficiency), UCB secures exclusive access to high-priced niche markets with enormous pricing power.

💉Fintepla® (fenfluramine):

Europe: Until 2032

USA: Until 2033 (with some downstream formulation patents even extending to 2038).

2. the key figures 📊

Market capitalization: Approx. EUR 47.7 billion (Listed on Euronext Brussels).

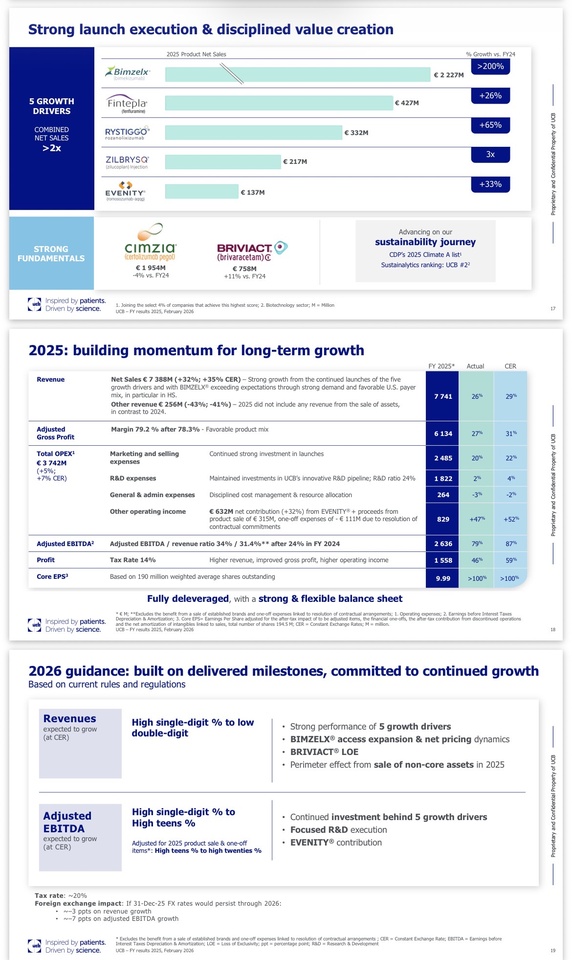

-Sales explosion: In the past financial year, turnover shot up by +26 % (+29 % adjusted for currency effects) to EUR 7.74 billion. The five new growth drivers more than doubled their sales to EUR 3.3 billion!

-EBITDA levers: Adjusted EBITDA exploded by +79 % to EUR 2.64 billion. The margin jumped to 34,0 % - a gigantic proof of the operating leverage (economies of scale of the global drug launches).

-Core EPS: Adjusted earnings per share almost doubled to EUR 9.99.

-Balance sheet restructuring (net cash): Within 12 months, almost EUR 1.5 billion of debt was completely repaid. UCB $UCB (+0,2%) emerged with a clean net cash position into 2026 and is now fully capable of making strategic acquisitions (M&A).

3. why is the share exciting NOW? 🚀

🟢 Decade of patent consolidation: The most important point for pharma investors: the core patents for growth drivers such as Bimzelx do not expire in the USA and Europe until between 2034 and 2037 expire. UCB $UCB (+0,2%) has one of the longest protected portfolios in the entire sector.

🟢US market penetration ignites: For Bimzelx, US commercial insurance coverage for 2026 has been expanded by 36 million patients to over 80%. The real sales tsunami in the USA is only just beginning.

🟢 The pipeline never sleeps: Behind the launches, the next wave is already waiting. The FDA granted fast-track status for the Alzheimer's hopeful Bepranemab at the beginning of 2026.

🟢Commercial excellence beats hype: UCB $UCB (+0,2%) reliably delivers hard numbers. The guidance for 2026 promises another year of high single-digit to low double-digit percentage sales growth despite the upcoming patent expiry of the old epilepsy drug Briviact.

🟢The 5 new hopefuls: They have increased their combined sales in 2025 to more than doubled to over 3.3 billion euros!

4. risks ⚠️

❗️Approval & trial dynamics: Clinical development is expensive. Setbacks in phase 3 trials (such as the upcoming readouts in the second half of 2026) can dampen sentiment in the short term

❗️Copycat erosion (Briviact LOE): Patent protection for the mature epilepsy drug Briviact will expire during 2026 in the US and Europe. This decline in sales must be actively swallowed by Bimzelx & Co.

❗️US regulation & price war: The US biologics market is highly competitive. Rebates to the powerful Pharmacy Benefit Managers (PBMs) could eat into gross margins

❗️Bewertung: With a P/E ratio of over 30, the share is no longer a bargain after the brilliant price rally (close to the 52-week high of ~EUR 290). A lot of growth is already priced in.

5.🚀 Outlook & pipeline catalysts for 2026

The management under CEO Jean-Christophe Tellier and CFO Sandrine Dufour confirmed the guidance for the current year 2026 in the spring:

✅Turnover 2026: Growth in the high single-digit to low double-digit percentage range is expected (in CER).

✅EBITDA 2026: Adjusted EBITDA is expected to increase in the high single-digit to mid teens percentage range.

✅ Pipeline successes: In early 2026, UCB received US FDA approval for Kygevvi™ (therapy for TK2 deficiency, an extremely rare genetic disease). In addition, an important Phase 2b trial with Galvokimig in atopic dermatitis is underway.

🎯 Personal conclusion & Reaper rating 🧐

I personally find UCB $UCB (+0,2%) extremely interesting and is high on my watch list because UCB has achieved the dream turnaround to a compounder and has mastered the tough transition to new products flawlessly. ( which I also think is $NOVO B (-0,23%) hoffe🙇♂️🙄) It is no longer a highly speculative biotech bet, but a highly profitable pharma growth machine with a fortress balance sheet.

Anyone looking for a European alternative to Novo Nordisk $NOVO B (-0,23%) could find the perfect candidate in UCB $UCB (+0,2%) could be the perfect candidate.

BONUS MATERIAL 💀

Jack's mustard: "The story is simply a dream for any quality investor. UCB has managed to do what 80% of pharma companies fail to do: not only have they cushioned the loss of a patent on an old blockbuster, but they have also pushed the successor rocket Bimzelx so brutally into the market that profits are literally exploding. The fact that they are now also completely debt-free takes a massive amount of risk off the table. After the brutal rally since the end of 2023, the stock is currently consolidating healthily around EUR 244 - for me an absolute top entry for the first tranche. If you are patient, you can lay the foundations for a relaxed decade of investment in your portfolio bunker. If the share corrects towards EUR 220, we won't hesitate for long, but will reload!

Rating: 🔥 BUY

Reaper Score:

8,3 / 10 (Based on the spectacular margin expansion, the eliminated debt and the verified sales momentum until the mid-2030s).

@Get_Rich_or_Die_Tryin

@Tenbagger2024

@schlimmschlimm

@Raketentoni and of course all other users ✌️