📊 MSCI World facing historic reform - What investors need to know now (in my case the $HMWO (+1,5%) HSBC MSCI World ETF )

Many investors invest passively in the MSCI World - often via ETFs such as the HSBC MSCI World UCITS ETF. But what many don't realize:

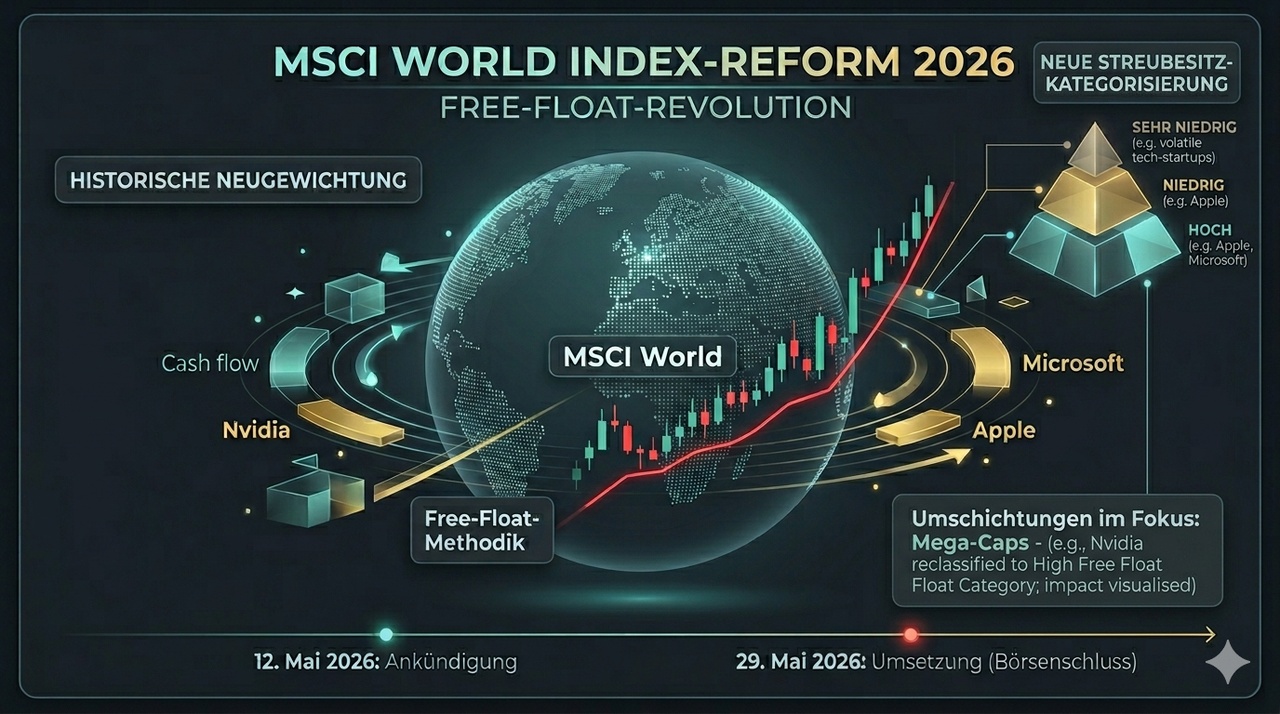

One of the biggest structural changes in the history of this index is due in May 2026.

I have summarized the most important points in an understandable and well-founded way - including a classification of what this means for us in concrete terms.

---

🔧 1. the major reform: change to the free-float methodology

The most important change will come into force on June 1, 2026 (after close of trading on May 29)**. MSCI is reforming the calculation of the so-called *free float*.

👉 Until now:

Rough rounding of freely tradable shares

👉 New:

Three categories for more precise mapping of tradability**

* High: >25 % (rounding to 2.5 %)

* Low: 5-25 % (rounding to 0.5 %)

* Very Low: <5% (rounding to 0.1%)

📌 Objective:

A **more realistic and precise weighting** of companies in the index.

---

⚖️ 2. Impact on the largest companies

The change particularly affects the heavyweights in the index (e.g. large US tech companies).

Why?

👉 Even small changes in the free float can have major effects:

* slight reduction → weight decreases

* slight increase → weight increases

📊 Consequence:

Weightings shift without price movement

Capital is partially redistributed from mega caps to smaller companies

➡️ Result:

slightly **more diversification

slightly less dominance of the largest tech stocks

---

🔄 3. one-off but massive need for reallocation

As a result of the reform, the index (and therefore also ETFs) must be rebalanced.

👉 This means:

Many purchases and sales at the same time

Above-average portfolio turnover

📉 Possible short-term effects:

Higher transaction costs

Slight tracking error

❗ Important:

This is not a permanent disadvantage, but a one-off adjustment effect.

---

📅 4. schedule of the index checks

The reform will be implemented as part of the regular MSCI review process:

May 12, 2026 → Announcement (Semi-Annual Review)

May 29, 2026*l→ Implementation (after close of trading)

Further reviews:

* August 12, 2026 / August 31, 2026

* November 11, 2026 / November 30, 2026

* February 9, 2027 / February 26, 2027

---

🌍 5. further structural changes

🇬🇷 Greece could return

MSCI plans to upgrade Greece from Emerging Market to Developed Market.

👉 Consequence:

Possible inclusion in the MSCI World

however **very low impact (<0.5 %)

---

🌱 ESG model update (5.0)

A new ESG valuation model is introduced.

👉 For classic MSCI World ETFs:

No direct influence on index composition

but:

Better database

Influence on internal ETF optimization

---

₿ Crypto rule deleted

A planned exclusion of companies with a high crypto share has been scrapped.

👉 Result:

affected companies remain in the index

* No structural distortion in this area

---

⚙️ 6. Special feature: Sampling in the ETF

The HSBC ETF does not use a complete replication of the index, but a so-called **optimization process (sampling)**.

👉 Advantage in this phase:

Not every share has to be traded

Rebalancing can be done more efficiently

➡️ This helps to cushion the costs of the reform

---

💰 7 What does this mean in concrete terms for investors?

In the short term (May-June 2026)

Increased trading activity

Slightly higher costs possible

Minimal performance deviations

Medium term

more stable index structure

More precise weighting

Long term

👉 Overall **positive**:

more realistic market mapping

better diversification

structurally robust index

---

🧠 Conclusion

This reform is no trifle - but a **fundamental improvement of the index methodology**.

👉 Important for us:

No need for action

No timing necessary

No ETF switch required

📌 The changes are:

Systematic

Plannable

Beneficial in the long term

---

📚 Sources

MSCI: Index Review Dates

https://www.msci.com/eqb/pressreleases/archive/ir_dates.pdf

https://www.msci.com/eqb/pressreleases/archive/ir_dates.pdf

MSCI GIMI Methodology (February 2026)

https://www.msci.com/eqb/methodology/meth_docs/MSCI_GIMIMethodology_Feb2026.pdf

https://www.msci.com/eqb/methodology/meth_docs/MSCI_GIMIMethodology_Feb2026.pdf

MSCI Index Announcements

https://www.msci.com/indexes/index-resources/index-announcements

https://www.msci.com/indexes/index-resources/index-announcements

MSCI ESG Ratings Model Update 2026

[https://www.msci.com/downloads/web/msci-com/discover-msci/events/event-assets/2026/february/2026%20MSCI%20ESG%20Ratings%20Model%20Updates%20FAQ.pdf]

https://www.msci.com/downloads/web/msci-com/discover-msci/events/event-assets/2026/february/2026%20MSCI%20ESG%20Ratings%20Model%20Updates%20FAQ.pdf

Analysis reports (aktiencheck.de, extraETF, etc.) on the methodology

reform and ETF effects

@DonkeyInvestor removed all **** that chatgpt put in there especially for you. I'll never do it again, it takes far too long 🤣