Thank you Rocket Lab $RKLB (+9,31%) :)

When I discovered the company two years ago, I was immediately interested. After intensive research, I decided to invest. This conviction has now more than paid off. Back then, everything was just right. Innovative company, technological excellence, moat, regulatory tailwind, megatrend, undervaluation, unknown....

For some time now, however, I have been selling parts of the company, not because I no longer believe in it, but because it is time to make room for potential successors. That doesn't mean that there haven't been many other good investments in the meantime, but I now want to approach things with a little more commitment. I sold about 30% of my RKLB position over the days and about 60% compared to the peak (they still make up 40% of my portfolio lol). With a KUV of 75 for this year, the valuation also seems to be very stretched now.

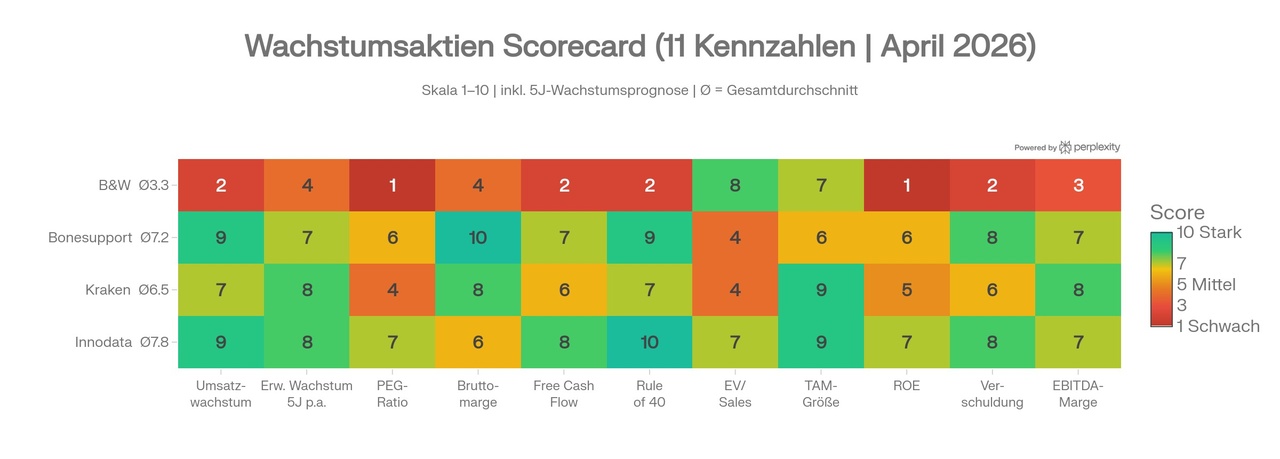

I now have many new candidates from different sectors and countries, but they all have that certain something in my opinion. Of course, you have to be able to withstand the volatility and the general risk, but the usual pessimists (without any detailed knowledge) also said that Rocket Lab would go bankrupt. My new favorites include:

Medley

$4480 (-0,45%) PKSHA $3993 (+3,28%) Kraken Robotics $PNG (+1,04%) Envipco $ENVI (+3,38%) Xvivo Perfusion $XVIVO (+0,91%) Bonesupport $BONEX (+3,53%) SEALSQ $LAES (+6,59%) Astroscale $186A (+6,88%) (Fujifilm $4901 (+2,09%) SoftBank $9984 (+6,42%))

What are your tenbaggers of the future?