Hello my dears,

On his trip to Asia, Juan visited another company in Japan that we hadn't yet introduced to you.

We would like to make up for this on today's public holiday.

You should sit in the sun, take some time and enjoy Juan's contribution.

If you like, you can also enjoy coffee and cake.

But please don't forget to like and comment.

We are looking forward to it!

Micronics Japan

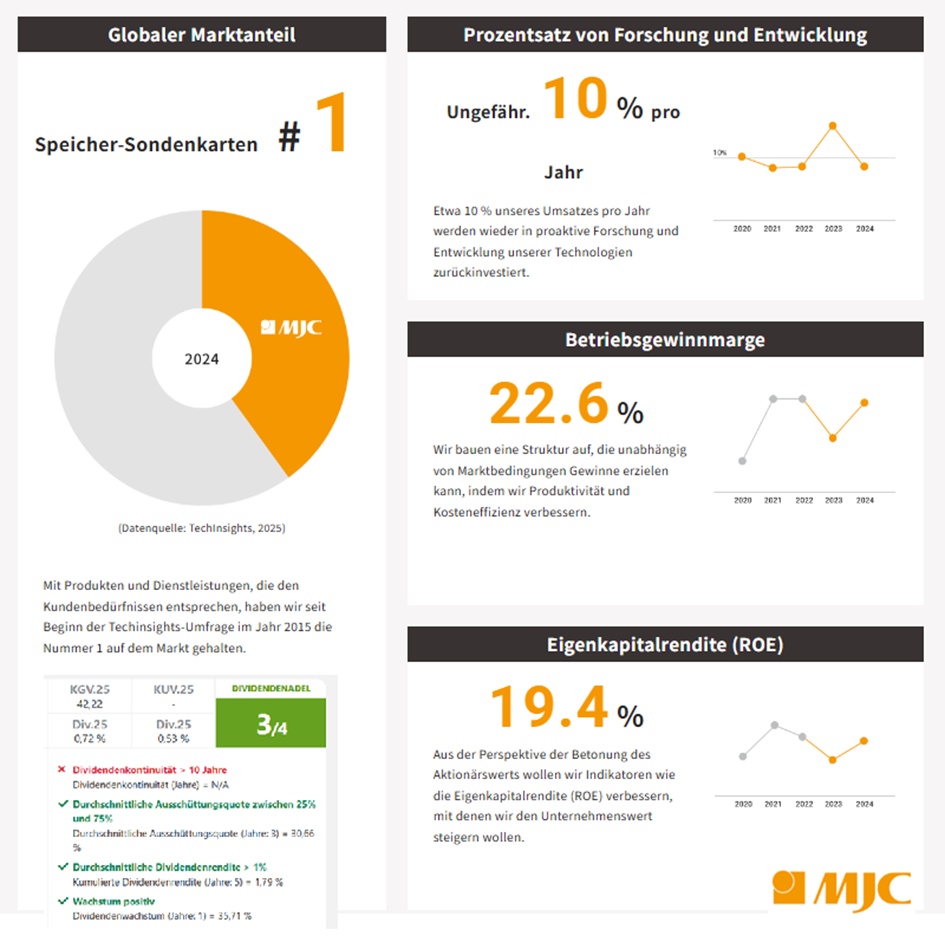

MICRONICS JAPAN CO., LTD. is a Japan-based company mainly engaged in the development, manufacture and sale of semiconductor measuring instruments and semiconductor and liquid crystal display (LCD) test equipment. The company operates in two business segments. The Probe Card segment develops, manufactures and sells semiconductor measurement instruments and offers a corresponding maintenance service. The Test Equipment (TE) segment develops, manufactures and sells LCD test equipment and semiconductor test equipment and offers a corresponding maintenance service.

Number of employees: 1,785

Transkript der Konferenz zu den Ergebnissen für das 4. Quartal des Geschäftsjahres 2025

Distribution of turnover by business division:

2025 (JPY)

Probe Card Business 68.52 billion

TE Business 1.65 billion

Geographical distribution of sales:

2025 (JPY)

South Korea 37.32 bn

Taiwan 21.69 bn

Other Asia 5.28 bn

Japan 5.16 bn

Europe and America 723 million

Number of locations 7 countries11 locations

Percentage of foreign sales Approx. 90%

Juan conclusion on the key financial figures (Micronics Japan 2025-2028)

Micronics Japan delivers a clean, powerful growth profilethat only a few small/mid-caps can achieve in this form. The story is clear: scaling high-margin businessincreasing profitability and a balance sheet that is net-cash-rich every year.

🔹 Growth & profitability

- Turnover grows continuously in double digits, 2028 even again with +20 % - This is a strong signal for an already profitable company.

- EBIT increases faster than sales every year → Operating levers are working perfectly.

- EBIT margin climbs from 23,6 % → 30,4 % - a premium level that demonstrates pricing power and efficiency.

🔹 Net result & cash flow

- Stable double-digit growth in profit, 2028 with +32,8 % particularly strong.

- FCF is negative in 2025, but this is clearly due to investment peaks - from 2026 the picture normalizes.

- FCF margin remains thin, but this is typical for companies with high CAPEX cycle dependency.

🔹 Balance sheet quality

- Net debt is negative and is becoming more negative every year → Micronics is building cash reserves up.

- This is a massive advantage in a volatile market environment.

- Leverage ratio remains consistently not relevant / not a burden.

🔹 Yields

- ROE increases to ~29 % - that is elite level.

- High ROE + rising margins = excellent capital allocation.

🔹 Juan's overall assessment

Micronics Japan looks like a company that is entering a new phase of profitability:

High margins, rising profits, strong balance sheet, operational scaling.

For me, this is a classic quality compounderwhich will continue to grow disproportionately high growth years - especially if the FCF margin follows suit.

Market value 502,384

Number of shares (in thousands) 38,764

Date of publication 13.02.2026

Juan conclusion on the valuation ratios of Micronics Japan

(Data source: your active MarketScreener tab )

Micronics Japan shows a 2026 valuation profile that combines quality + growth without slipping into the extreme valuation zones of many semiconductor stocks. For Juan it looks like this:

🔹 P/E ratio - moderate despite strong price increase

With a P/E ratio of 27.3× Micronics clearly below many high-end peers (ASML 38×, Lam 44×, Lasertec 51×). For a company that double-digit growth and expanding its margins, this is absolutely justifiable.

→ Juan-Take: "Not cheap, but clearly below the sector hype - solid valuation."

🔹 P/B ratio - high, but typical for quality tech

The KBV of 6.24× seems ambitious at first glance, but: Micronics delivers ROE ~29 %i.e. a return on capital that justifies a higher P/B ratio.

→ Juan-Take: "Expensive book value, but neatly covered by high returns."

🔹 PEG - strong signal

The PEG of 0.5× is a real highlight. Anything below 1 is considered undervalued relative to growth.

→ Juan-Take: "PEG is the secret star - growth more favorable than the price suggests."

🔹 Dividend - small but growing

Dividend per share increases from 95 → 136.7 JPY, yield 2026 at 1,04 %. No income play, but steady increase and payout ratio decreases → more leeway.

→ Juan-Take: "Dividend is bonus, not investment case."

🔹 Overall rating

Micronics Japan is not a bargainbut significantly cheaper than many semiconductor highflyerswhile growth, margins and balance sheet quality above average are above average.

Juan's overall assessment:

"Valuation fair to attractive - especially due to PEG and growth. A quality stock that is not yet fully priced in."

Interpretation (compact & clear)

- Micronics Japan has a P/E ratio well below the sector average → green.

- Dividend yield is mediocrebut stable → yellow.

- ASE Technology is the only real "double green" stock (cheap + high dividend).

- Most US stocks (Lam, Entegris, Onto) are expensive expensive and hardly pay any dividends → red.

(P/E ratio Not cheap, but below sector average)

Juan's total score: 89 / 120 → 🟩 Tenbagger zone

Juan's conclusion:

Micronics Japan is a high-quality growth compounder with a strong balance sheet, rising margins and a PEG that almost screams "undervalued". The only real drag is the still unsettled FCFbut this is typical for CAPEX-intensive semiconductor equipment suppliers.

For Juan, Micronics is clearly a tenbagger candidate for the next 5-7 years.

Performance

1 week +5.38 %

1 month +37.00 %

6 months +50.88 %

1 year +274.32 %

3 years +750.93 %

5 years +435.16 %

7 years +888.36 %

PRICE: € 71.00 (01.05.2026 at 12:00 noon) @PikaPika0105

@Simpson