Opinion on Silicon Valley Bank ($SIVB)

Dear Community, With all the discussion surrounding SVB since last week, we wanted to answer some of the questions/topics that have been heavily discussed in our community 🙂 .

Prior to getquin, I worked as an M&A banker for Deutsche Bank and was heavily involved in the recapitalization of European and American banks. So I would like to use my experience to answer some of these points.

(Disclaimer - this is not investment advice. Everyone is responsible for their own research and investment decisions).

Why was SVB small enough for limited regulation, but systemically important enough for a bailout? How did depositors get their money back? Who pays? They say not the taxpayers - is that true?

In the U.S., banks with less than $250 billion in deposits have lower capital requirements and simpler stress tests (for comparison, Deutsche Bank's private bank ($DBK (-2,66%)) has over USD 300 billion in deposits worldwide. And that is really not little).

The lower testing allowed these banks to offer more attractive products and received a large influx of deposits during Covid and during periods of quantitative easing. The onset of quantitative tightening, i.e., higher interest rates, by the Fed, the availability of better rates elsewhere, and high burn by depositors (i.e., mostly startups) were the main risks that these banks began to face and triggered uncertainty in this area (more details below).

Larger banks, on the other hand, are in a much better liquidity position due to stricter regulations.

Although everyone is talking about a bail-in (i.e. bail-out), technically it is not, since only depositors get their money back, not the bank's equity and bondholders. The latter are wiped out because they took a known risk by owning these securities.

The money for the deposits comes from a fund into which all banks pay, the Deposit Insurance Fund (Deposit Insurance Fund).

Will the new SEC rules be enough to prevent this from happening again? What does better regulation look like? Will we see more bank failures like this one and Signature Bank ($SBNY) ?

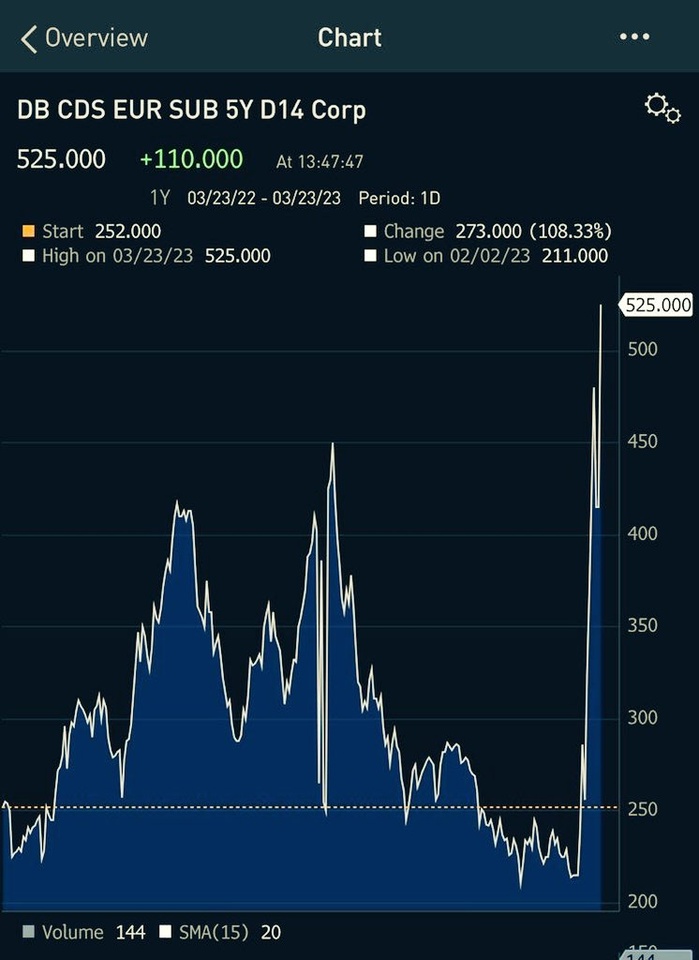

It's always a fine line between regulation and profitability, especially when you're talking about U.S. banks because they tend to be the biggest donors in presidential elections (so a lot of lobbying work goes into that). In Europe, after the 2008 crisis, they decided to be stricter with banks. So the European banking sector has really suffered in terms of shareholder returns. But even with stricter regulation, you are never protected from mismanagement in the banking sector, as we are currently seeing with Credit Suisse ($CSGN). So regulators not only need to implement stricter capital controls, but also stricter rules and management oversight.

On the subject of the massive selling of shares by bank management in recent weeks - why was this not a public issue and why were people not surprised about it at the time?

It is quite common for listed companies to incentivize their executives and the Board of Management not only with high salaries but also with attractive option packages, especially in the USA. The U.S. Securities and Exchange Commission (SEC) does not actually prohibit executives from buying or selling stock before earnings are announced, as long as the company's legally required disclosures are up to date. In practice, this means the following:

- Stock must be held for at least six months before it is sold.

- The person selling the shares must have notified the sale at the latest at the time of the sale (cf. SE Rule 144).

The last point was already amended at the beginning of this year and comes into force on April 1, so that management is required to notify the intention to sell 90 days before the shares are actually sold.

It should be noted that SVB paid bonuses at the beginning of March. So the timing and the large amount of shares sold by management is a concern, and lawmakers will likely address it in the near future.

If high interest rates are the cause of the bank failure, will banks benefit from lower interest rate increases because they would be directly negatively impacted by higher interest rates? Will the Fed therefore slow down to reduce the risks to banks?

A bank's business model is key to answering this question. Banks receive deposits from their customers and in return give them interest on that amount. The bank then takes that money and lends it to individuals or businesses in exchange for interest payments. This difference is called the net interest margin (NIM) and has always been an important indicator of a bank's earnings potential.

Now interest rates have become a variable. When interest rates were zero or even lower, banks had difficulty monetizing their loans well, even when volumes were higher. So they began to use deposits to buy additional securities, which they either sell at a profit in the short term (i.e., that's the job of each bank's trading department) or hold longer to profit from interest payments (i.e., typically corporate bonds, asset-backed securities).

What every bank should do, regardless of its size, is to always lower its potential risk:

- For loans - ensure that they can be repaid, i.e., do not lend to low-quality borrowers.

- For securities - ensure that they do not incur losses.

As interest rates have changed repeatedly in the past, banks have been forced to adjust their income streams. The mistake SVB made was to take mostly deposits from startups (i.e. high monthly consumption and low deposit rate) and invest in long maturity bonds without hedging against higher than expected interest rate increases (they should have bought swaps to hedge, by the way, but that's another discussion!). So when deposits became scarce, the bank had no choice but to sell those long maturity bonds at a huge loss (i.e. bond prices move inversely to interest rates). And suddenly it needed cash to make up for those losses. We have all heard about the rest extensively in the last few days.

Given the current level of inflation, interest rates simply have to be higher (this is not investment advice, but reflects the current consensus of the ECB and leading money managers). The risk of prolonged inflation is worse than the short-term pain of higher interest rates. So we can expect central banks to continue to focus on tightening interest rates in the hope that they can be eased in the near future.

#svb

#fed

#ezb

#zinsen

#bonds

#loans

#inflation

#stocks