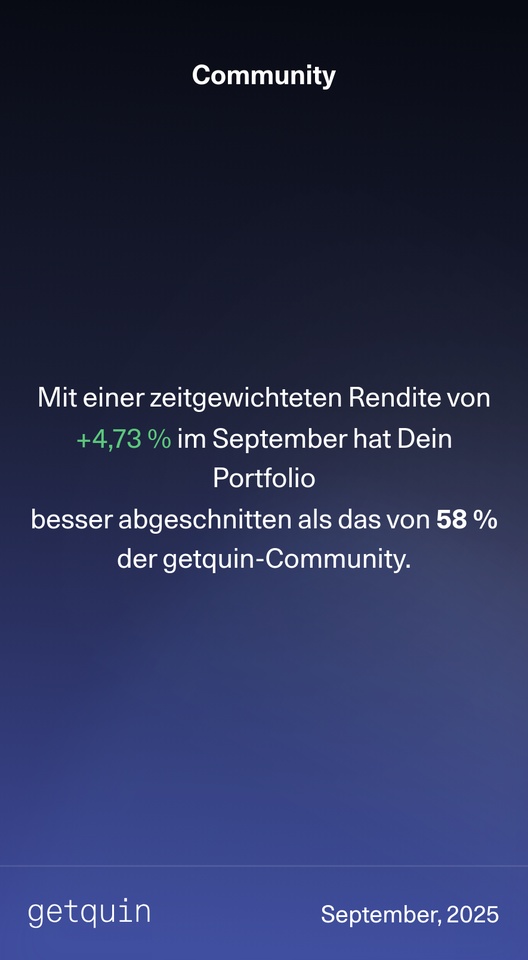

When I look back on the last 9 months today, I am truly grateful.

@Shiya I had been introduced to an incredibly detailed company presentation on Rocket Lab ($RKLB (-6,93%)

) with an incredibly detailed company presentation.

I was super intrigued, did some more research myself and then jumped on the bandwagon - and with increasing conviction I added more with every dip.

My average entry level went up as a result, but it was worth it:

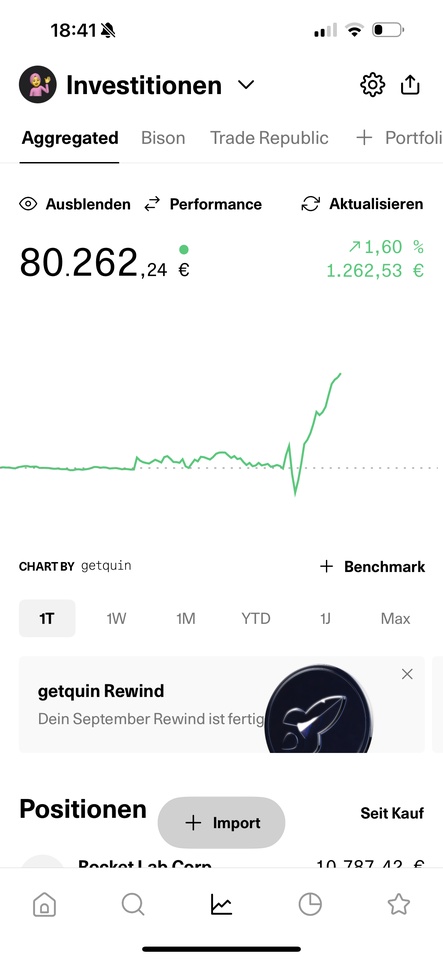

+116 % with currently 390 shares (until today, my target would actually have been 500 shares, but I also had to put something into one or two ETFs to spread my risk and also buy two medical stocks to limit my losses 😅) - but now: My first real "hundred-bagger moment" 🚀.

We want to do our garden in the spring 🌿 - without this tip (and my stamina during the sometimes violent setbacks 😜) we would probably need a loan.

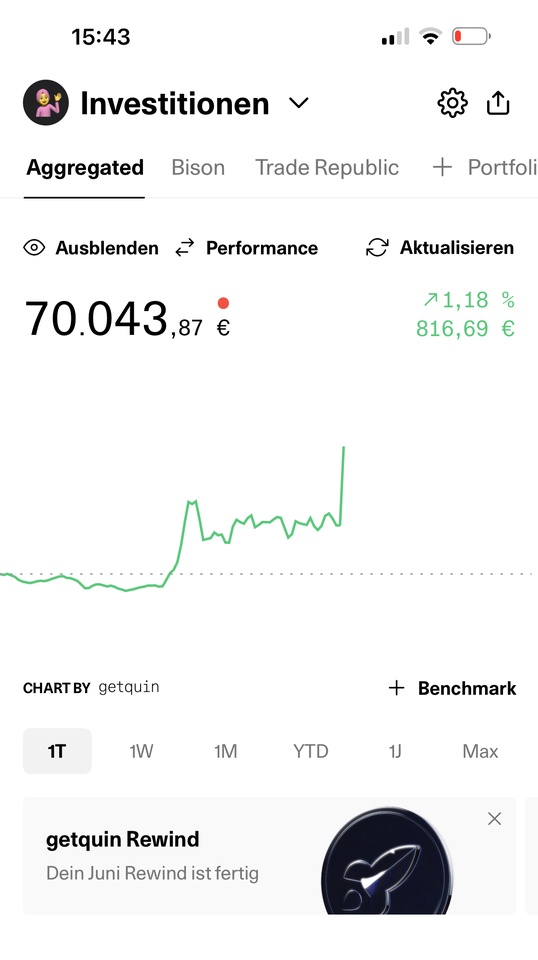

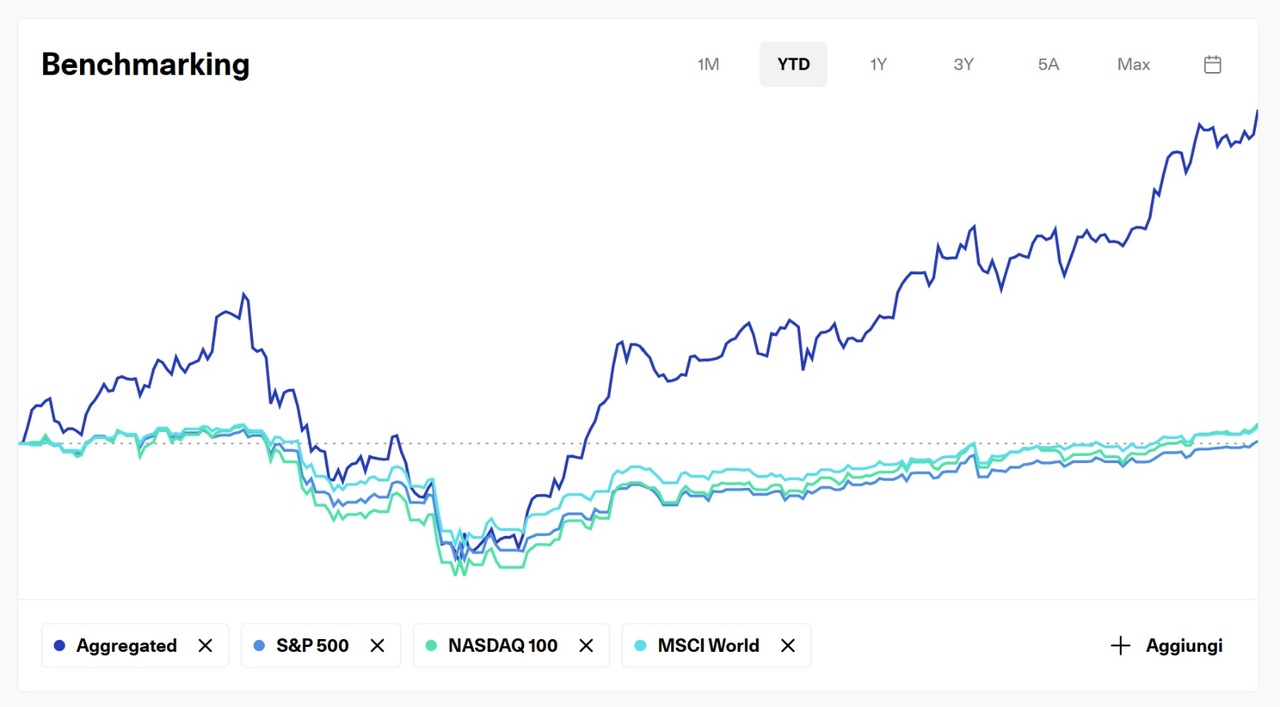

After an exciting phase with a lot of movement in the share price Rocket Labseems to have stabilized - and at an impressively high level.

Despite the capital increase and insider selling, the upward trend remains fully intact.

- Breakout above 54 $ confirmed - accompanied by conspicuous dark pool purchases with a volume of over 500 m $.

- Capital increase? Long since digested by the market.

- Insider selling? More normal profit-taking than a signal of no confidence.

Fundamentally, things are going well:

- The HASTE mission (Hypersonic Accelerator Suborbital Test Electron) was successful - an important contract for the US Department of Defense.

- Neutron remains on schedule - engine tests completed, Launch window open until the end of the year.

- The Veeco deal doubles solar cell production - next step towards vertical integration.

- New: 10 additional start-ups with Synspective (Japan) - so now 21 planned missionsa strong signal of confidence from international customers.

The entire Space & Defense sector is showing momentum - ETFs such as $UFO or $ITA are also breaking out bullishly.

👉 Conclusion: Healthy volatility, strong order books and a clear technical trend - everything continues to point to strength.

I remain invested and plan to sell the first only if Neutron really takes off by the end of the year (so much for the theory, let's see if I can hold out 😂

Perhaps a little emotional - but patience has not been a bad strategy here so far.

I think: Rocket Lab remains one of the most exciting space titles of the next few years.

The Sky is (still) the Limit. 🌌