🔹 Revenue: $3.5B (Est. $3.42B) 🟢 +2% YoY

🔹 EPS: $0.51 (Est. $0.45) 🟢

🔹 Comparable Sales: +2% (Est. +1.6%) 🟢

Tariff Impact:

🔸 Minimal in Q2.

🔸 FY gross impact of $250M–$300M if tariffs stay; after mitigation, net ~$100M–$150M weighted to H2.

FY Outlook

🔹 Revenue: +1% to +2% (vs. $15.1B in FY24)

🔹 Operating Income: +8% to +10% (vs. $1.1B in FY24)

🔹 Net Interest Income: ~$15M

🔹 Effective Tax Rate: ~26%

🔹 CapEx: ~$600M

🔹 Net Store Closures: ~35

Q2 Outlook

🔹 Revenue: Flat YoY

🔹 Gross Margin: Similar to Q1 (41.8%)

🔹 Operating Expense (% of Sales): Slight leverage YoY

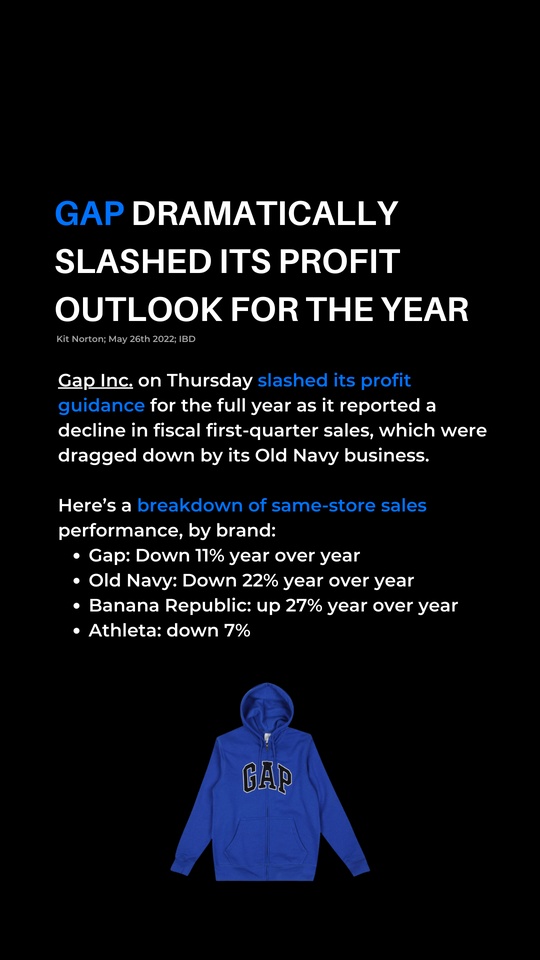

Brand-Level Comparable Sales (Q1 FY25)

🔹 Old Navy: +3% (9th straight quarter of share gains)

🔹 Gap: +5% (6th straight positive comps, 8th quarter share gain)

🔹 Banana Republic: Flat (Net sales -3%)

🔹 Athleta: -8% (Net sales -6%)

Other Q1 Metrics:

🔹 Gross Margin: 41.8% (+60 bps YoY)=

🔹 Online Sales: +6% YoY; 39% of total sales

🔹 Store Sales: Flat YoY; 2,496 company-operated out of ~3,500 total stores=

🔹 Inventory: $2.1B (+7% YoY)

🔹 Cash & Short-Term Investments: $2.2B (+28% YoY)

🔹 Free Cash Flow: -$223M

🔹 Shareholder Return: $131M via dividends and buybacks

🔹 Shares Repurchased: 4M for $70M

🔹 Dividend: $0.165/share approved for Q2

CEO Commentary

🔸 "Exceeded expectations. Positive comps for the 5th straight quarter. Brand reinvigoration is working. Staying focused on controllables for long-term growth." – Richard Dickson, CEO