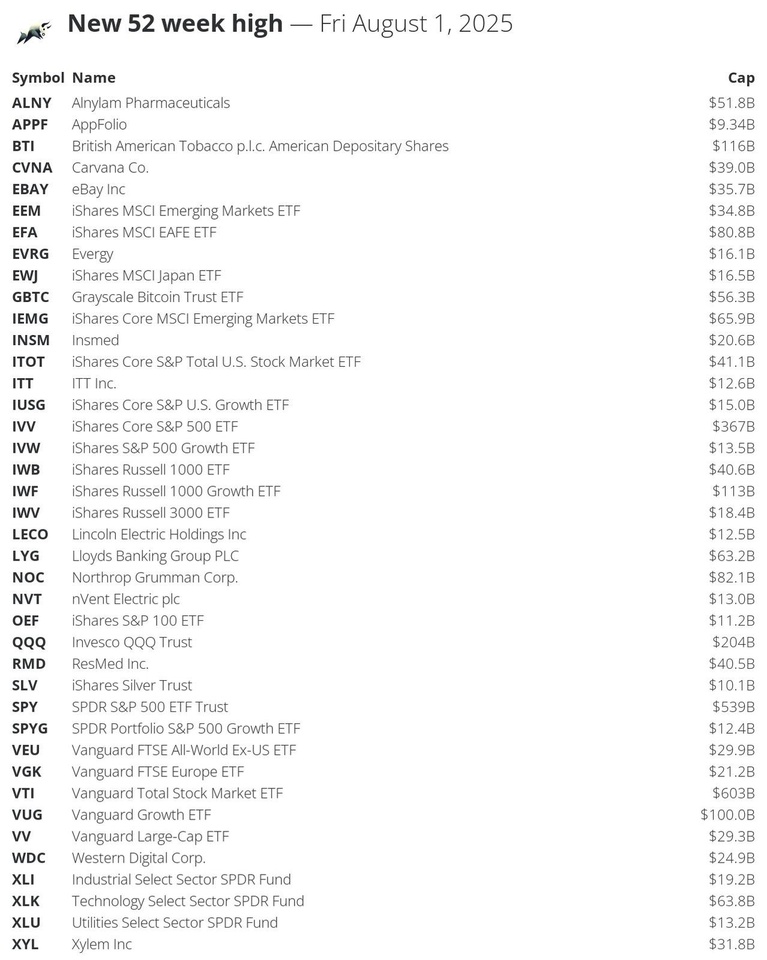

🔝 Stocks that made a new 52-week high today: $VTI (-3,04%)

$SPY (-3,04%)

$IVV (-3,07%)

$QQQ

$BTI (-0,68%)

$IWF (-3,54%)

$VUG (-3,63%)

$NOC (-2,31%)

$EFA

$IEMG (-4,05%)

$XLK

$LYG

$GBTC

$ALNY (+0,18%)

$ITOT (-3,12%)

$IWB (-3,05%)

$RMD (-2,58%)

$CVNA (-9,59%)

$EBAY (-2,91%)

$EEM

$XYL (-2,22%)

$VEU (-2,8%)

$VV (-3,05%)

$WDC (-5,61%)

$VGK (-1,57%)

$INSM (-1,41%)

$XLI

$IWV (-3,08%)

$EWJ (-4,38%)

$EVRG (+0,54%)

$IUSG

$IVW

$XLU

$NVT

$ITT (-1,67%)

$LECO (-3,2%)

$SPYG

$OEF (-3,15%)

$SLV

$APPF (-3,13%)

#52weekHigh

Discussione su EBAY

Messaggi

312Mes·

Market News

33

5Mes·

08.05.2025

The US Federal Reserve leaves key interest rates unchanged + Online company Amazon invests in logistics + Alphabet slumps - Apple tests AI search in its browser + Paypal further expands its market leadership in German e-commerce + Disney benefits from theme parks and streaming

The US Federal Reserve leaves key interest rates unchanged

- but points to increased risks of both higher inflation and rising unemployment.

- According to the FOMC, the economy continues to expand at a solid pace, with the decline in production in the first quarter attributable to record imports.

- It reports that the economy is growing at a solid pace.

- The Fed reports that employment is stable and the labor market remains solid.

- It sees increased risks of higher unemployment and inflation.

- This assessment could have an impact on future monetary policy.

- The latest interest rate decision was taken unanimously.

- It was noted that uncertainty about the economic outlook has increased further.

- Investors should pay attention to possible effects on future monetary policy decisions.

- The US Federal Reserve is holding the key interest rate at 4.25 to 4.50 %, which is in line with forecasts.

The online company Amazon $AMZN (-5,92%)invests in logistics

- so that it can deliver to its customers even more frequently on the day they order.

- This was announced by Rocco Bräuniger, Vice President responsible for Amazon's German-speaking regions, among other things.

- "We are working on further expanding same-day delivery and extending order acceptance times," said Bräuninger at Amazon's innovation presentation "Delivering the Future".

- The intention is for customers to be able to order later in the day and still receive their items on the same day.

- Amazon then plans to introduce same-day delivery at 20 new locations in Europe over the next twelve months, including Augsburg, Metz and Bergamo, for groceries and cosmetics, but also for many other everyday items.

- (Handelsblatt)

Alphabet $GOOGL (-3,4%)slump - Apple $AAPL (-4,63%)tests AI search in its browser

- Alphabet's A-share price fell sharply in response to the news that Apple is testing an artificial intelligence (AI)-based search function in its internet browser.

- The shares of Google's parent company were recently trading 5.8 percent lower at USD 153.71.

- Apple's shares also fell sharply in response to the news, losing 2.1 percent to 194.32 dollars.

- The slide of the two heavyweights also caused the technology-heavy Nasdaq 100 index to slide into negative territory on Wednesday, having previously posted a moderate gain.

- Apple is "actively" looking into transforming the Safari web browser on its devices into an AI-powered search engine, said Eddy Cue, senior vice president of services at the technology company.

- He made this statement during his testimony in the US Department of Justice trial against Alphabet.

- At the center of the dispute is the agreement between Apple and Google, worth an estimated 20 billion dollars per year, which makes Google the default offering for search queries in Apple's integrated browser.

Paypal $PYPL (-9,04%)further expands its market leadership in German e-commerce

- This was announced by the EHI Institute on Wednesday on the occasion of its Payment Congress in Bonn.

- According to the report, the proportion of online purchases paid for via PayPal rose by 0.8 percentage points to 28.5% compared to 2023.

- Paypal has a strong market position in Germany, particularly thanks to its cooperation with the online auction house Ebay $EBAY (-2,91%)a strong market position.

- Unlike in other European markets, the local banks and savings banks did not succeed in launching their own payment system for paying for online purchases at an early stage.

- "Paypal's market share would be significantly higher if market leader Amazon offered this payment method," states payment expert Horst Rüter from EHI.

- (Börsen-Zeitung)

Disney $DIS (-2,19%)profits from theme parks and streaming

- Thanks to its theme park and streaming business, entertainment giant Disney is defying the uncertainty following Donald Trump's tariff crackdown.

- While many US companies are withdrawing their forecasts for this year, Disney exceeded analysts' expectations with its outlook.

- The share price rose by more than five percent at times in pre-market US trading.

- Contrary to the company's own expectations, the number of subscriptions to the Disney+ streaming service grew by 1.4 million to 126 million within three months.

- The business, which has long been loss-making in recent years, generated an operating profit of 336 million dollars.

- In theme parks and cruises, the operating result rose by nine percent year-on-year to just under 2.5 billion dollars.

- Disney remains optimistic for the rest of the financial year, emphasized CEO Bob Iger.

- Disney now expects adjusted earnings per share to increase by 16 percent to 5.75 dollars for the year to the end of September.

- Analysts had expected an average forecast of 5.44 dollars.

- In the last quarter, Disney sales rose by seven percent year-on-year to 23.6 billion dollars.

- The bottom line was a profit of just under 3.28 billion dollars after a loss of 20 million dollars a year earlier.

Thursday: Stock market dates, economic data, quarterly figures

- ex-dividend of individual stocks

- Vonovia EUR 0.90

- Mercedes-Benz Group EUR 5.30

- GRENKE 0.40 EUR

- Wacker Chemie EUR 2.50

- Hannover Rueck EUR 7.20

- Rational 13.50 EUR

- Schoeller-Bleckmann Oilfield EUR 1.75

- Renault EUR 2.20

- FUCHS EUR 1.11

- H & M SEK 3.40

- Quarterly figures / company dates USA / Asia

- 06:45 Toyota quarterly figures

- 08:30 Nintendo annual results

- 13:00 Conocophillips quarterly figures

- 14:00 UPS AGM

- 14:30 Ford AGM

- 17:00 Kraft Heinz AGM

- 22:00 Expedia | News Corp | Pinterest | Lyft | Quarterly figures

- 23:30 Alcoa AGM

- Quarterly figures / Company dates Europe

- 06:45 Zurich Insurance | Basler quarterly figures

- 07:00 Anheuser-Busch | Aurubis | Hella | Knorr-Bremse quarterly figures

- 07:00 Heidelberg Materials Trading Update 1Q

- 07:00 Lanxess | Siemens Energy | Ströer | Hamborner Reit | SMA Solar

- 07:00 Wacker Neuson quarterly figures

- 07:30 Gea | Henkel | Infineon | Rheinmetall | Elringklinger | Fielmann

- 07:30 GFT Technologies | SGL Carbon | SAF-Holland quarterly figures

- 07:50 Suss Microtec quarterly figures

- 08:00 Puma | Deutsche Beteiligungs | A.P. Moeller-Maersk Quarterly Figures | Infineon PK

- 09:00 Hella | Henkel Analyst Conference | Ströer Analyst and Press Conference

- 09:30 Deutz AGM | Infineon Analysts' Conference

- 10:00 Sto SE quarterly figures | Allianz | EnBW | MTU Aero Engines | Qiagen

- 10:00 KSB | Uniper AGM | Lanxess | Qiagen PK

- 10:30 Talanx AGM | Siemens Energy Analyst Conference | Henkel PK

- 11:00 Jost Werke AGM | Hamborner Reit Analyst and Press Conference

- 13:00 Zurich Insurance | Lanxess Analyst Conference

- 14:00 Baywa quarterly figures | Basler | Heidelberg Materials | Gea

- 14:00 Rheinmetall Analyst Conference

- 15:00 Elringklinger Earnings Call | Puma | Qiagen Analyst Conference

- 17:00 DocMorris AGM

- 18:00 Enel | Leonardo Quarterly figures

- Economic data

08:00 DE: Trade balance March trade balance calendar and seasonally adjusted FORECAST: n.a. previous: +17.7 bn Euro Exports FORECAST: +1.0% yoy previous: +1.8% yoy Imports FORECAST: +0.5% yoy previous: +0.7% yoy

08:00 DE: Production in the manufacturing sector March seasonally adjusted PROGNOSE: +0.8% yoy previous: -1.3% yoy

09:30 SE: Sveriges Riksbank, outcome of the Monetary Policy Council meeting FORECAST: 2.25% previously: 2.25%

10:00 NO: Norges Bank, outcome of the Monetary Policy Council meeting FORECAST: 4.50% previously: 4.50%

13:00 UK: BoE, outcome and minutes of the Monetary Policy Council meeting Bank Rate PROGNOSE: 4.25% previously: 4.50%

14:30 US: Initial jobless claims (week) Forecast: 230,000 Previous: 241,000

14:30 US: Productivity ex Agriculture (1st release) 1Q annualized PROGNOSE: -0.7% yoy 4th quarter: +1.5% yoy Unit labor costs PROGNOSE: +5.1% yoy 4th quarter: +2.2% yoy

16:00 US: Wholesale inventories 3/25 (final)

2020

5Mes·

EBAY Q1'25 Earnings Highlights

🔹 Revenue: $2.59B (Est. $2.55B) 🟢; UP +1.1% YoY

🔹 Adj EPS: $1.38 (Est. $1.34) 🟢; UP from $1.25 YoY

🔹 FCF: $644M (Est. $492.4M) 🟢; UP +36% YoY

Operating Metrics

🔹 GMV: $18.75B (Est. $18.52B) 🟢; UP +0.7% YoY

🔹 U.S. GMV: $9.07B (Est. $8.92B) 🟢; UP +1% YoY

🔹 International GMV: $9.69B (Est. $9.58B) 🟢; UP +0.4% YoY

🔹 Active Buyers: 134M (Est. 134.17M) 🟡; UP +1.5% YoY

Q2'25 Guidance

🔹 Net Revenue: $2.59B–$2.66B (Est. $2.6B) 🟡

33

7Mes·

27.02.2025

Nvidia quarterly figures + Salesforce revenue misses expectations and outlook disappoints + Cryptocurrency threatens to slide into a bear market + Amazon launches "Alexa+" with advanced AI features + Snowflake beats estimates + C3.ai loss narrows and revenue rises + EBay forecasts quarterly revenue

Nvidia $NVDA (-6,14%)quarterly figures

- NVIDIA Corp. fourth quarter earnings per share of $0.89 beat analyst estimates of $0.84.

- Revenue of USD 39.3 billion exceeds expectations of USD 38.02 billion.

- Sales increase of 78 percent in the past quarter

- Nvidia forecasts sales of USD 43 billion (plus/minus 2%) for the first quarter, exceeding market expectations of USD 41.78 billion, as the company expects continued strong demand for its AI chips.

- Gross margin is expected to fall to 71% due to start-up costs for the new Blackwell AI chips, below the 72.2% expected by Wall Street.

Salesforce revenue $CRM (-2,41%)misses expectations and outlook disappoints

- Salesforce reported fourth-quarter revenue late Wednesday that fell short of Wall Street estimates, while earnings from its customer relationship management platform came in higher than expected.

- Revenue rose 8% year-over-year to $9.99 billion for the three months ended Jan. 31, but fell short of the $10.04 billion consensus estimate compiled by FactSet.

- Adjusted earnings per share rose from $2.29 to $2.78, above market expectations of $2.61.

- Shares fell 5.6% in after-hours trading.

- Subscription and support revenue rose 8% to $9.45 billion, while professional services and other increased from $539 million to $542 million.

- Salesforce expects fiscal 2026 adjusted earnings per share of $11.09 to $11.17, which would be an increase from the $10.20 reported in January but below the consensus estimate of $11.20.

- Revenue is expected to increase 7% to 8% to $40.5 billion to $40.9 billion, a slowdown from the 9% growth in fiscal 2025 and below market expectations of $41.37 billion for fiscal 2026.

- For the current quarter, Salesforce expects adjusted earnings per share of $2.53 to $2.55 on revenue of between $9.71 billion and $9.76 billion, which would represent year-over-year growth of 6% to 7%.

- The Street is expecting $2.62 billion and $9.91 billion respectively.

Cryptocurrency $BTC (-0,33%)threatens slide into a bear market

- Bitcoin's price slide accelerated in the meantime on Wednesday afternoon.

- However, the oldest and best-known digital currency stabilized again recently.

- Bitcoin briefly slipped to 85,341 dollars on the Bitstamp trading platform, its lowest level since mid-November last year.

- Most recently, Bitcoin was trading at almost 87,900 dollars and thus back at the level of Tuesday evening.

- Since reaching a record high of more than 109,000 dollars in January, Bitcoin has lost around a fifth at its peak.

- From a market perspective, the cryptocurrency is in a "bear market" at this level.

- This means that prices are set to fall over a longer period of time.

- Bitcoin's most recent slide accelerated on Tuesday after the price fell below 90,000 dollars.

- This caught those investors on the wrong foot who had bet on rising prices with leveraged products.

- These investors now had to close their positions, which intensified the selling pressure in the short term.

- "Bitcoin and Co. are still in the grip of trade disputes," wrote expert Timo Emden from Emden Research.

- Investors fear further punitive tariffs by US President Donald Trump in particular, which is detrimental to general risk appetite.

- At the same time, disappointment over the lack of concrete steps to introduce strategic Bitcoin reserves in the US is likely to resonate.

- In addition, the developments of the past weekend could continue to weigh on sentiment for cryptocurrencies, Emden continued.

- A cyber attack on the service provider Bybit had caused a furor.

Amazon $AMZN (-5,92%)introduces "Alexa+" with enhanced AI functions

- With the new functions, it can converse with users and is available free of charge for Prime customers

- The new version is initially launching in the USA.

- The platform will be rolled out gradually in all countries where Alexa is currently available, enabling more natural control of smart home devices and connection to security cameras.

Snowflake $SNOW (-4,44%)exceeds estimates in the 4th quarter

- Snowflake on Wednesday reported fourth-quarter non-GAAP diluted earnings of $0.30 per share, up from $0.35 a year earlier.

- Analysts polled by FactSet had expected $0.18.

- Revenue for the quarter ended Jan. 31 was $986.8 million, up from $774.7 million a year earlier.

- Analysts polled by FactSet had expected $956.9 million.

- The company said it expects product revenue of $955 million to $960 million for the first quarter and $4.28 billion for fiscal 2026.

- Analysts were expecting $961 million for the quarter and $4.23 billion for the year.

- The stock rose more than 9% in extended trading.

C3.ai $AI (-7,18%)Q3 loss narrows and revenue increases

- C3.ai on Wednesday reported a non-GAAP diluted loss of $0.12 per share for the third quarter, down from a loss of $0.13 a year earlier.

- Analysts polled by FactSet had expected a loss of $0.25.

- Revenue for the quarter ended Jan. 31 was $98.8 million, up from $78.4 million a year earlier.

- Analysts polled by FactSet had expected $98.1 million.

- The company expects fourth-quarter revenue of $103.6 million to $113.6 million and 2025 revenue of $383.9 million to $393.9 million.

- Analysts polled by FactSet expect $108.6 million for the quarter and $388.3 million for the year.

EBay $EBAY (-2,91%)forecasts quarterly revenue

- E-commerce company eBay on Wednesday forecast first-quarter revenue below Wall Street estimates, pointing to weak demand for products such as collectibles and refurbished goods.

- Shares of eBay fell about 7% in extended trading.

- High interest rates and persistent inflation have held back consumer spending in the U.S. for two years, leading to sluggish demand for non-essential items such as collectibles and luxury accessories.

- EBay has been pressured by slowing advertising revenue.

- The company expects revenue for the quarter to be between $2.52 billion and $2.56 billion, compared with analysts' average estimate of $2.59 billion, according to data compiled by LSEG.

- The company expects first-quarter adjusted earnings between $1.32 and $1.36 per share, with the midpoint above estimates of $1.33.

Thursday: Stock market dates, economic data, quarterly figures

- ex-dividend of individual stocks

- Unilever GBP 0.38

- Diageo 0.41 GBP

- Barclays final 0.06 GBP

- Quarterly figures / company dates USA / Asia

- 22:30 HP Inc Quarterly figures

- No time specified: Edison International | The Mosaic | Dell | Autodesk quarterly figures | GE Healthcare Technologies Investor Day

- Quarterly figures / Company dates Europe

- 06:00 Adtran Networks preliminary annual results

- 07:00 Hella | Kion | Nordex | Deutsche Pfandbriefbank | Axa | ABB | Swiss Re annual results

- 07:30 Baader Bank | Befesa | Sixt | Aixtron | Hensoldt | Scout24 | Telefonica SA annual results

- 07:45 Eni SpA, Strategic Plan 2025 - 2028 | Engie SA Annual Results

- 08:00 Beiersdorf | Haleon | London Stock Exchange | Rolls-Royce Annual Results

- 09:00 Iberdrola Annual Results | Kion Analyst and Press Conference | Befesa Analyst Conference | Beiersdorf Analyst and Press Conference

- 09:30 Deutsche Pfandbriefbank BI-PK

- 10:00 Hella Analyst Conference | Scout24 PK

- 12:00 Intesa Sanpaolo detailed annual results and annual report

- 13:00 SAP Annual Report

- 14:00 Eni SpA analyst and press conference

- 15:00 Scout24 Analyst Conference

- 18:05 Saint-Gobain annual results

- Without time information: ACS | Endesa | Valeo | EDP Annual figures

- Economic data

09:00 CH: GDP 4Q FORECAST: +0.2% yoy/+1.6% yoy previous: +0.4% yoy/+2.0% yoy

09:00 ES: HICP and consumer prices (preliminary) February HICP PROGNOSE: +2.9% yoy previously: +2.9% yoy

10:00 EU: ECB, M3 money supply and lending January M3 money supply FORECAST: +3.8% yoy previously: +3.5% yoy

11:00 EU: Economic Sentiment Index February Eurozone Economic Sentiment PROGNOSE: 96.0 PREV: 95.2 Industrial confidence Eurozone PROGNOSE: -12.0 PREV: -12.9 Consumer confidence Eurozone PROGNOSE: -13.6 PREV: -13.6 PREV: -14.2

11:00 EU: Eurozone Business Climate Index February

11:30 BE: Consumer Prices February

13:30 EU: ECB, minutes of the Governing Council meeting of January 29/30

13:30 US: Richmond Fed President Barkin, speech at Fayetteville Cumberland Economic Development

14:30 US: GDP (2nd release) 4Q annualized PROGNOSE: +2.3% yoy 1st release: +2.3% yoy 3rd quarter: +3.1% yoy GDP deflator PROGNOSE: +2.2% yoy 1st release: +2.2% yoy 3rd quarter: +1.9% yoy

14:30 US: Initial jobless claims (week) FORECAST: 225,000 Previous: 219,000

14:30 US: New orders for durable goods January FORECAST: +2.0% yoy previous: -2.2% yoy

17:45 US: Fed Governor Bowman to speak at Fort Hays State University Robbins Banking Institute event

2121

1 Commento

Heinrich@KnusperKnabe91

7Mes

••

7Mes·

eBay Q4'24 Earnings Highlights

🔹 Adj. EPS: $1.25 (Est. $1.20) 🟢

🔹 Revenue: $2.6B (Est. $2.58B) 🟢; UP +1% YoY

🔹 GMV: $19.32B (Est. $19.07B) 🟢; UP +4% YoY

Q1'25 Guidance

🔹 Revenue: $2.52B-$2.56B (Est. $2.6B) 🔴

🔹 GMV: $18.3B-$18.6B; FX-Neutral Growth: 0% to +1%

🔹 Adj. EPS: $1.32-$1.36

Segment Performance

🔹 Non-GAAP Operating Margin: 27.0% (Prev. 26.7%) 🟡

🔹 Free Cash Flow: $560M

🔹 Operating Cash Flow: $677M

Capital Returns & Financial Position

🔹 Stock Buybacks: $900M (14M shares repurchased)

🔹 Dividends Paid: $128M

🔹 Cash & Equivalents: $7.2B

Business Highlights

🔸 eBay expanded AI-powered bulk listing tools across all U.S. categories

🔸 Introduced Klarna 'Buy Now, Pay Later' in multiple European markets

🔸 Ad Revenue: $445M; First-party ads: $434M (+18% YoY)

🔸 Eliminated fees for U.K. C2C sellers across all categories (excl. vehicles)

Strategic & ESG Updates

🔸 Sourced 100% renewable energy for offices & data centers in 2024

🔸 Set 2045 net-zero carbon target, validated by SBTi

🔸 Raised $192M through eBay for Charity, UP +18% YoY

CEO Jamie Iannone Commentary

🔸 "eBay achieved three consecutive quarters of GMV growth, reinforcing our vision to reinvent the future of e-commerce for enthusiasts."

CFO Steve Priest Commentary

🔸 "We met or exceeded expectations across key financial metrics and have a strong foundation for sustainable, long-term growth."

33

9Mes·

$JMIA (-9,4%) - Company presentation (difficult market/great potential):

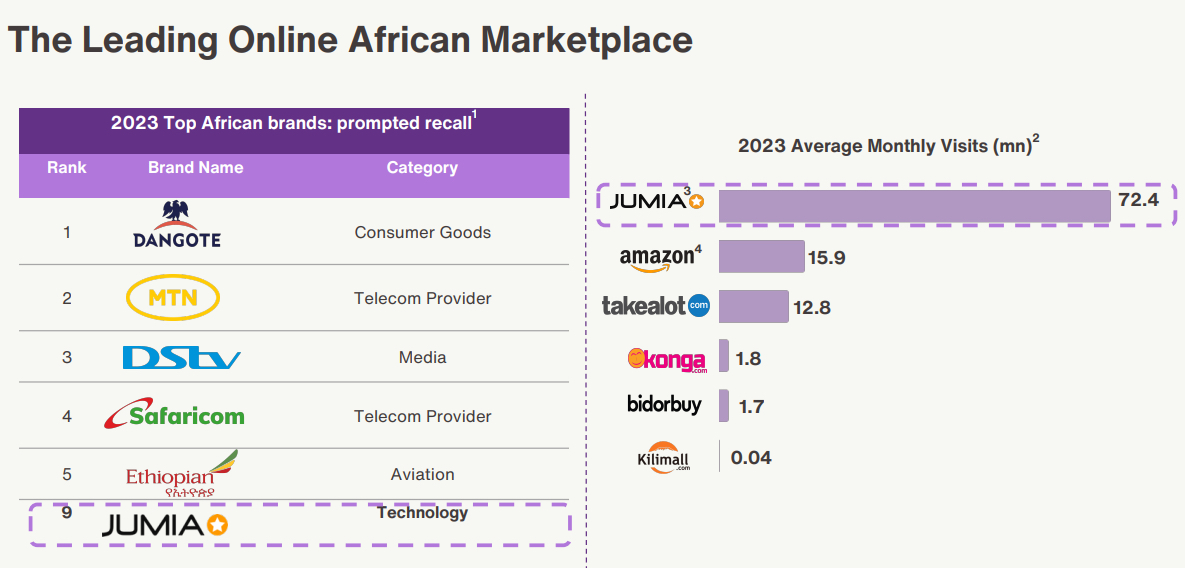

$JMIA (-9,4%) is an online trading company operating in Africa. The company offers a wide range of products such as electronic goods and fashion.

It offers payment, food delivery, credit and flight booking services.

They stand out in the African e-commerce landscape. Their innovative platform is revolutionizing traditional retail by offering a diverse range of products and services online that are tailored to the specific needs of the African market. The company's integrated payment system, JumiaPay, enhances the customer experience through a seamless, secure transaction process. Jumia's logistics network, designed to overcome regional challenges, ensures efficient delivery, strengthening the company's position as a leader in African e-commerce.

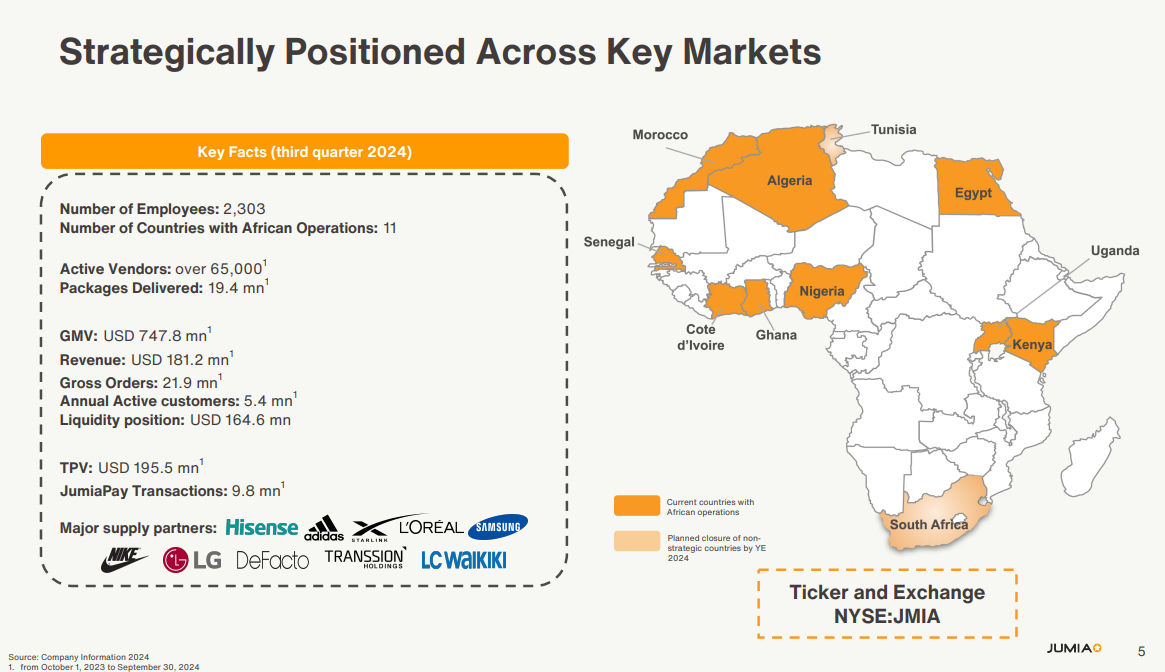

$JMIA (-9,4%) was founded in Lagos Nigeria in 2012 by two former management consultants Jeremy Hodara and Sacha Poignonnec.

$JMIA (-9,4%) is active in 11 African countries: Nigeria, Egypt, Morocco, Kenya, Ivory Coast, South Africa, Tunisia, Algeria, Ghana, Senegal, Uganda

$JMIA (-9,4%) Logistics enables the convenient and reliable delivery of goods. It consists of a large network of rented warehouses, pick-up stations for consumers and drop-off points for sellers, as well as more than 400 local external logistics service providers. Their logistics partners and facilities are seamlessly integrated and managed through their proprietary technology, data and processes.

$JMIA (-9,4%) is taxable in Berlin, the development team is based in Portugal and the actual headquarters are in Dublin .

For this reason, and because the nationality of the two CEOs is French, there are various doubts that $JMIA (-9,4%) is an African company, as is claimed in the self-promotion.

- In March 2016, the company managed to raise 50 million euros in venture capital

- As Africa's first "unicorn", the technology start-up reached a valuation of over 1 billion US dollars

- In April 2019, the company made its stock market debut on the New York Stock Exchange, raising capital of USD 196 million

- Jumia's share price initially tripled within the first three days of trading before settling back around the initial price a month later

- Among other things, the share price was negatively affected by the allegation made by the US portal Citron Research that Jumia had reported false key figures prior to the IPO.

Arguments for $JMIA (potential/giant market opportunities):

- Africa's e-commerce penetration is only ~5%, compared to over 20% globally, suggesting huge upside potential

- Africa's population is projected to account for 25% of the world's population by 2050 (a huge untapped consumer base)

- With an average age of 19.7 years - a young, digitally savvy consumer base.

- Internet penetration is growing rapidly and is expected to reach 65% by 2030, driven by affordable smartphones and growing infrastructure.

- $JMIA (-9,4%) is active in 11 major African markets and covers over 70% of the continent's GDP and internet users.

- Market leader in logistics: $JMIA (-9,4%) Processed 5.6 million parcels on Black Friday and has a delivery infrastructure that covers urban and rural areas

- Fintech expansion: JumiaPay increased transactions by 40% year-on-year, creating opportunities in Africa's underserved regions with banking services

- Financial upside and synergies: Jumia's market capitalization is USD 554 million, the company trades at only about double its revenue

- 1.7 billion Africans will join the consumer economy by 2030, driving demand for e-commerce

- Strong growth figures: GMV (Gross Merchandise Volume) +33% YoY (currency adjusted) showing robust demand.

- Orders +18 % YoY, driven by the success of Black Friday.

- Growth in the interior of Nigeria: +44 % YoY,

- Solid financial position: USD 164.6m in cash reserves - ample liquidity for future investments. Operating losses are falling every quarter, demonstrating cost discipline and efficiency gains.

- Attractive valuation: Trades at ~2x sales and 1.7x EV/sales, well below peers in high-growth markets. Market capitalization of USD 554m positions Jumia as a small-cap with significant upside potential.

- Strategic implementation: Focus on domestic expansion, procurement efficiency and adaptation to local markets. Utilization of logistical capacities: 5.6 million parcels were handled during the Black Friday season (+24% year-on-year).

- Long-term potential: Positioned as Africa's leading e-commerce platform. Benefits from improved infrastructure, increasing internet penetration and growing consumer acceptance.

- The African e-commerce market is expected to grow exponentially from USD 30 billion in 2024 to over USD 75 billion in 2030.

The anxiety around Jumia often revolves around a single question: what happens when giants like $AMZN (-5,92%) , $BABA (-8,67%) or $PDD (-6,86%) decide to enter the African market?

At first glance, this is a legitimate concern. But this perspective overlooks the essence of e-commerce success in Africa. It's not about flashy apps or sprawling warehouses in cities - it's about solving the logistical puzzle. And that's where Jumia's advantage lies. Africa's logistical challenges are unprecedented. In many regions, physical addresses are not a given, but a rarity, making deliveries difficult and turning traditional e-commerce models on their head.

$JMIA (-9,4%) operates in an environment where customers often live miles away from hubs and there are no traditional delivery points. This is where Jumia has built its moat. It's more than an e-commerce platform, it's a logistics powerhouse designed to tackle the complexities of the continent. It's not just about delivering parcels. Jumia's network connects remote and rural regions that global competitors may not be able to serve. Take Nigeria, for example. With a population of over 200 million, the consumer base extends far beyond the urban centers of Lagos. Selling products is one thing, reaching underserved regions with sparse infrastructure is another and this is where $JMIA (-9,4%) strength.

The logistics system is not easily replicated and is a barrier to entry that global giants must reckon with. International players eyeing Africa have a difficult choice: invest billions in building a comparable infrastructure or partner with $JMIA (-9,4%) whose network has already proven itself in markets such as Ghana, Kenya and the Ivory Coast. In either case $JMIA (-9,4%) benefit from this. The company is the natural ally - or rival - for any e-commerce player trying to gain a foothold in Africa. And $JMIA (-9,4%) is constantly improving its market position and is not satisfied. Operational improvements are further consolidating its position. Consolidating smaller warehouses into larger, technology-enabled facilities and optimizing fulfillment centers in core markets such as Nigeria and Ghana reduces $JMIA (-9,4%) inefficiencies. These changes not only reduce costs, but also create scalability, allowing the company to expand deeper into untapped regions where there is little competition.

Of course, the macroeconomic backdrop is tough. Currency devaluations and volatile markets weigh heavily on $JMIA (-9,4%) 's operating environment. But its logistics network remains an irreplaceable asset that global competitors struggle to replicate, even with significant investment. A current outstanding key figure underlines this: Over 50% of orders from $JMIA (-9,4%) now come from outside the major cities, a testament to its reach and resilience.

Western companies often dream of penetrating African markets, but constantly fail. Deciphering the African logistics code has proved too complex, and currency risks are driving many to retreat. Meanwhile $JMIA (-9,4%) is flourishing. It is adapting to challenges that others consider insurmountable and consolidating its leadership position.

Can competitors catch up? A question that is often asked ?

At the moment, they can't really. Jumia's logistics network is more than an operational tool, it's a fortress. This system, built to withstand Africa's unique challenges, is the foundation of its success. It is also the core of its strategy, the playbook of $AMZN (-5,92%) , $MELI (-6,22%) , $BABA (-8,67%) to follow.

Building a strong logistics network to create lasting barriers to market entry. The latest Black Friday results (as briefly outlined above) underline this potential. Orders increased by 18 % year-on-year, while GMV (Gross Merchandise Volume) grew by an impressive 33 % in constant currency.

However, significant currency devaluations in key markets such as Nigeria and Egypt dampened reported GMV growth to just 2%. Despite these headwinds, Jumia's underlying business demonstrates its ability to weather macroeconomic storms. The customer retention metrics speak for themselves. The total number of customers rose by 9% and orders increased by 18%.

A 44% increase in physical goods orders from regions outside Nigeria's major cities. This expansion into the interior of the country underlines the untapped potential that Jumia is beginning to develop.

The switch to an asset-light model is also paying off. Jumia Logistics recorded a 24% increase in parcel volumes, underlining the efficiency of its operations. On the supply side, international procurement is booming. The number of items from global sellers has risen by 31 %.

This diversifies the platform's offering to meet growing consumer demand. This diversification is critical to cementing Jumia's role in Africa's dynamic e-commerce landscape. And yet the market has not caught up. Despite this progress, Jumia's valuation is still not dependent on the dynamics of its core business.

Continued improvements in logistics, geographic expansion and customer acquisition could provide the basis for significant upside potential

However, the way forward will not be easy. Currency fluctuations in key markets and dependence on cash reserves pose risks. But Jumia offers a rare opportunity to enter one of the fastest growing e-commerce markets in the world. $JMIA (-9,4%) is far from over - it is just beginning.

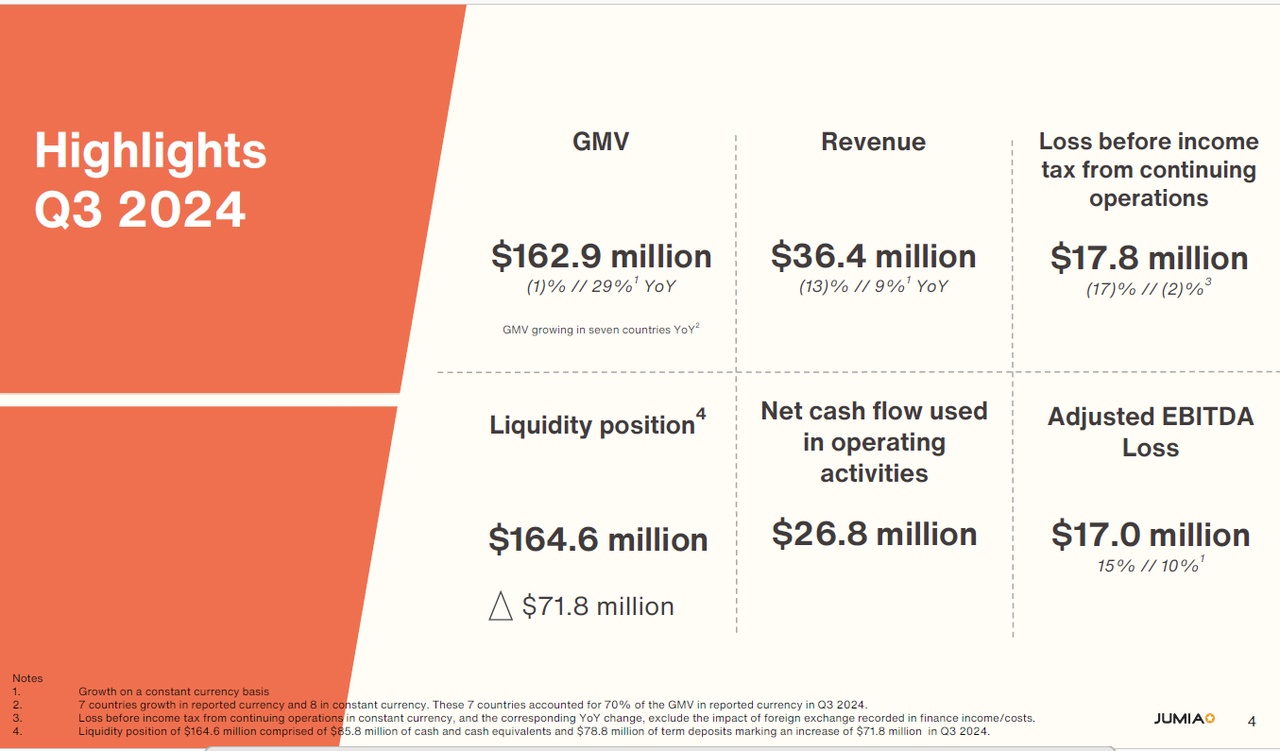

Earnings highlights for the third quarter of 2024:

- Revenue of $36.4 million, down 13% YoY, or up 9% in constant currency

- GMV of $162.9 million, down 1% YoY, or up 29% in constant currency

- Operating loss of $20.1 million compared to $18.3 million in the third quarter of 2023, up 10% YoY, and up 6% in constant currency

- Adjusted EBITDA loss of $17.0 million compared to $14.8 million in the third quarter of 2023, up 15% YoY, and up 10% in constant currency

- Loss before income tax from continuing operations of $17.8 million in the third quarter of 2024, down 17% YoY or down 2% in constant currency

- Liquidity position of $164.6 million, an increase of $71.8 million in the third quarter of 2024, that includes the net proceeds from the August 2024 At-the-Market (ATM) offering, compared to a decrease of $19.0 million in the third quarter of 2023

- Net cash flows used in operating activities of $26.8 million compared to $24.0 million in the third quarter of 2023

- Summary and personal opinion: $JMIA (-9,4%) Blend of market leadership, operational improvements and growth in untapped regions, positions the company for exponential growth. At current levels, it could be a rewarding, very long-term investment in one of the most promising markets in the world, even if the environment is very challenging and the investment naturally carries a lot of risk. A takeover by a major player such as $AMZN (-5,92%) , $MELI (-6,22%) , $BABA (-8,67%) could also be possible, as setting up your own logistics is very difficult and costly. ✌️

$AMZN (-5,92%) , $MELI (-6,22%)

$BABA (-8,67%) , $SE (-4,15%) , $PDD (-6,86%) , $JD (-6,72%) , $9618 (-5,5%) , $9988 (-8,32%) , $CPNG (-4,08%) , $EBAY (-2,91%)

+ 1

1414

19 Commenti

quite exciting, is just rather higher risk

•

22

•11Mes·

Analyst updates, 05.11.

⬆️⬆️⬆️

- ODDO BHF raises the price target for BIONTECH from USD 110 to USD 130. Outperform. $BNTX (-2,88%)

- BARCLAYS raises the price target for AIRBUS from EUR 161 to EUR 165. Overweight. $AIR (-2,1%)

- CITIGROUP raises the price target for SCOUT24 from EUR 91 to EUR 94.50. Buy. $G24 (-1,82%)

- WARBURG RESEARCH raises the price target for REDCARE PHARMACY from EUR 174 to EUR 176. Buy. $RDC (-0,72%)

- DEUTSCHE BANK RESEARCH raises the price target for RYANAIR from EUR 17 to EUR 17.50. Hold. $RYA (-1,89%)

- BERNSTEIN rates EBAY from Market-Perform to Outperform. Target price USD 70. $EBAY (-2,91%)

- ODDO BHF raises the price target for SALZGITTER from EUR 14 to EUR 15.50. Underperform. $SZG (-6,41%)

- BARCLAYS raises the target price for COMMERZBANK from EUR 16 to EUR 17. Equal-Weight. $CBK (-0,56%)

- BARCLAYS raises the target price for MTU from EUR 295 to EUR 340. Equal-Weight. $MTX (-2,98%)

- MORGAN STANLEY rates LUFTHANSA to Equal-Weight. Target price EUR 7. $LHA (-2,02%)

- BERENBERG raises the price target for DEUTSCHE KONSUM REIT from EUR 3.50 to EUR 5. Hold.

⬇️⬇️⬇️

- GOLDMAN lowers the price target for MERCEDES-BENZ from EUR 65 to EUR 63. Buy. $MBG (-1%)

- UBS lowers target price for 1&1 from EUR 21.60 to EUR 21. Buy.

- WARBURG RESEARCH lowers the price target for GFT TECHNOLOGIES from EUR 40 to EUR 37.50. Buy. $GFT (-3,69%)

- HAUCK AUFHÄUSER IB lowers the price target for ECKERT & ZIEGLER from EUR 63.50 to EUR 55. Buy. $EUZ (-2,45%)

- BARCLAYS lowers the price target for BNP PARIBAS from EUR 90 to EUR 85. Overweight. $BNP (-1,68%)

- BERENBERG downgrades SCHNEIDER ELECTRIC from Buy to Hold and lowers price target from EUR 261 to EUR 255. $SU (-2,76%)

- BERENBERG lowers the price target for BEFESA from EUR 41 to EUR 31. Buy. $BFSA (-3,14%)

77

11Mes·

Aftermarket after quarterly figures

+21% Carvana $CVNA (-9,59%)

+11% Twilio $TWLO (-6,43%)

+9% Sprouts Farmers Market $SFM (-2,76%)

+7% Booking $BKNG (+0,36%)

+7% Paycom Software

+5% Allstate

+4% Transocean

+3% Clorox $CLX (+0%)

+2% KLA $KLAC (-5,88%)

+1% Starbucks $SBUX (-2,43%)

+1% Omega Healthcare

+0% Microsoft $MSFT (-3,3%)

-1% Amgen

-1% DoorDash $DASH (-5,35%)

-1% AFLAC

-1% Public Storage

-2% Equinix

-3% Meta $META (-5,02%)

-4% MicroStrategy $MSTR (-7,17%)

-4% Coinbase $COIN (-9,55%)

-6% MetLife

-6% MGM Resorts

-6% Riot Platforms $RIOT (-7,91%)

-7% eBay $EBAY (-2,91%)

-7% Ventas

-9% Robinhood Markets $HOOD (-9,88%)

-10% Roku

-11% Monolithic Power Systems

-13% Aurora Innovation

1616

3 Commenti

all figures wrong but also of course if these also change

•

22

•11Mes·

Update analyst assessments:

$TSLA (-6,86%) | RBC raises target price for TESLA from USD 236 to USD 249. Outperform.

$KO (+0,18%) | JPMORGAN lowers the price target for COCA-COLA from USD 78 to USD 75. Overweight.

$TMUS (+0,17%) | UBS raises the price target for T-MOBILE US from USD 210 to USD 255. Buy.

$T (-1,52%) | UBS raises the price target for AT&T from USD 24 to USD 25. Buy.

$AOF (-5,6%) | WARBURG RESEARCH raises the price target for ATOSS SOFTWARE from EUR 142 to EUR 144. Buy.

$UA (-3,19%) | UBS raises the price target for UNDER ARMOUR from USD 11 to USD 12. Buy.

$JST (-3,56%) | WARBURG RESEARCH raises the price target for JOST WERKE from EUR 62 to EUR 77. Buy

$IBM (-4,51%) | UBS raises the price target for IBM from USD 145 to USD 150. Sell.

$FTK (-2,36%) | HAUCK AUFHÄUSER IB downgrades FLATEXDEGIRO from Buy to Hold and lowers target price from EUR 16 to EUR 15.

$ROG (-0,98%) | DEUTSCHE BANK RESEARCH raises the price target for ROCHE from CHF 235 to CHF 250. Sell.

$EBAY (-2,91%) | UBS raises the price target for EBAY from USD 59 to USD 72. Neutral.

$KER (-1,58%) | RBC lowers the price target for KERING from EUR 280 to EUR 230. Sector-Perform.

99

1Anno·

📣All these stocks hit new 52 WEEK HIGHS at some point today

📣All these stocks hit new 52 WEEK HIGHS at some point today

Alcon $ALC (-4,15%)

Applovin $APP (-6,13%)

Beigene $BGNE (-4,83%)

Boston Scientific $BSX (-2,02%)

British American Tobacco $BTI (-0,68%)

Carrier $CARR

Fair Isaac $FICO (-2,99%)

NextEra $NEE (-1,61%)

ServiceNow $NOW

Natera $NTRA

Public Service $PEG (-0%)

Insulet $PODD (-2,26%)

Sharkninja $SN

Squarespace $SQSP

Stryker $SYK (-2,46%)

66

Titoli di tendenza

I migliori creatori della settimana

<contenitore>Dati LSX</contenitore> · Dati finanziari di FactSet