Hello everyone!

After my AI assistant "Mister Prompt" and I dug up a solid REIT in the Swedish forests the day before yesterday, we set off on another search today. This post is a little special dedication to our @Tenbagger2024 - You had asked for a real "racehorse" where dividends don't matter and pure, explosive growth is the priority!

But also for everyone else who wants to add some rapid momentum to their portfolio: Buckle up. Here is a stock that is currently benefiting massively from global megatrends and for which there is not yet a single post here in the forum: $IVSO (+0,58%)

INVISIO AB.

A little hint, I'm not invested yet, but from Monday I'll be on the speculative side of my dumbbell strategy.

🚁 Who is INVISIO and who are the customers?

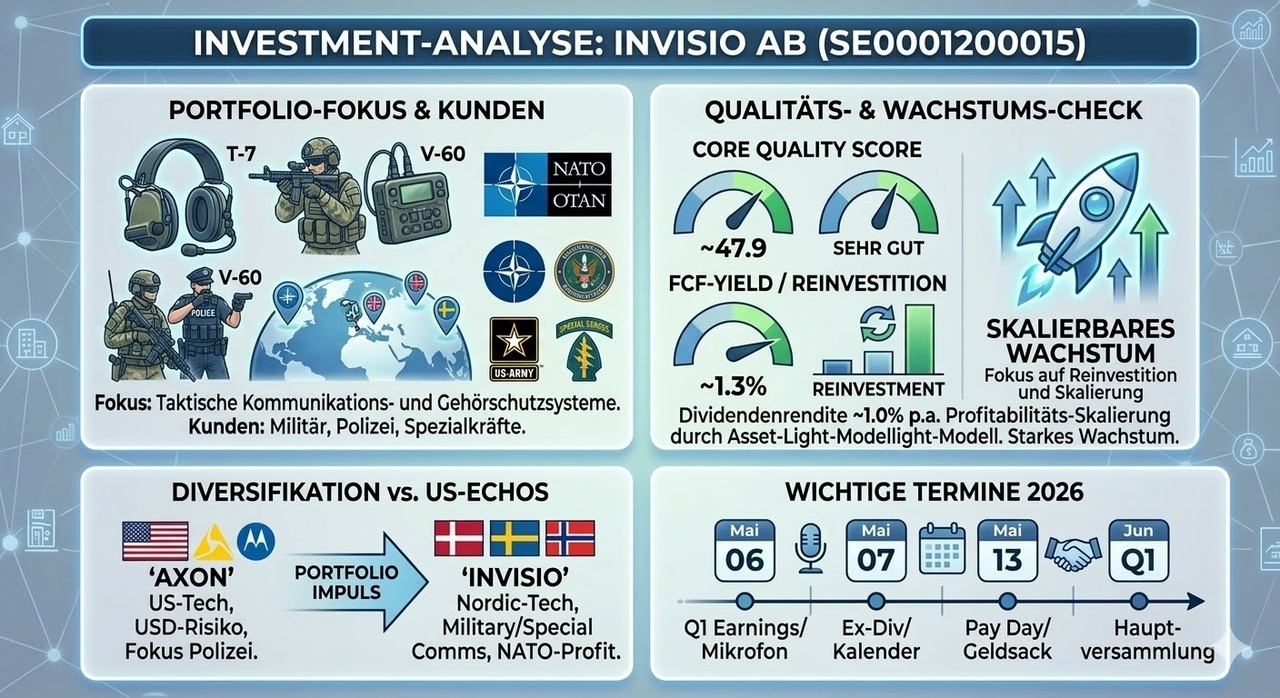

INVISIO (based in Copenhagen, listed in Stockholm) develops state-of-the-art tactical communication systems and high-tech hearing protection for special forces, the military and police forces worldwide.

This is not a classic headset business, but vital equipment: the systems allow emergency forces to communicate with each other in deafening noise (helicopters, gunfire, explosions) at room volume and at the same time protect their hearing from trauma. Customers include Western governments and the NATO armed forces. An absolute beneficiary of the current massive increase in global defense budgets!

📊 The evaluation dashboard (as of March 13, 2026)

The current share price is approx. 304.50 SEK (approx. 28.60 EUR) with a market capitalization of approx. SEK 14 billion (approx. EUR 1.3 billion). The valuation is - fittingly for a racehorse - extremely sporty:

============================================================

📉 CURRENT KEY VALUATION FIGURES (TTM)

============================================================

▶ P/E ratio (price-earnings ratio): ~ 64.4

▶ KCV (price-cash flow ratio) : ~ 77.2

▶ KUV (price-sales ratio) : ~ 8.2

▶ P/B ratio (price-book value ratio) : ~ 12.1

▶ Dividend yield : ~ 1.0 %

============================================================

🔬 The quality and formula check

A P/E ratio of over 60? We have to apply our strict filters to see whether this is insubstantial storytelling or qualitative growth:

1. core quality formula (sales growth + operating margin = score)

- Growth & Margin: Q4 sales growth was a very strong 15.1% (in a record quarter with SEK 684m sales). As INVISIO works extremely "asset-light" (research in-house, production externally), the profit scales immediately: the operating margin (EBIT) was recently at a fantastic 32,8 %.

- Result: 15,1 + 32,8 = Score 47.9.

- Conclusion: Our rule of thumb says: > 25 = "very good". With almost 48 points, INVISIO pulverizes this mark. Extremely strong, profitable growth!

[ CORE QUALITY SCORE METER ]

< 15 (Schwach) | 15-25 (Solide) | > 25 (very good)

---------------------------------------------------

⭐⭐⭐ 47,9 !

2. cash flow quality formula (FCF yield = free cash flow / market cap)

- Evaluation: The FCF yield is only around 1,3 %. This would be a knock-out criterion for our income portfolio. But: Our filter exception rule states: "Low or negative is only permitted with clear growth". INVISIO immediately reinvests every available cent in scaling, which is exactly what management should do with a 32.8% margin!

3. dividend filter (income core)

- Result: The proposed dividend for 2025 is SEK 3.00 (yielding just under 1.0%). This naturally falls well short of our 3.5% minimum. But our exception rule also applies here: the balance sheet is incredibly strong (more cash than debt!) and growth is extremely high. The dividend is just nice pocket money for us shareholders.

4. the hard exclusion rule

Growth is positive, the margin is sustainable and well above 5%, the business model is backed up by hard figures (record order backlog of over SEK 854 million). Despite the high valuation: check passed!

🆚 Comparison with US stocks (The Axon / Motorola effect)

Why INVISIO when you can also buy Axon Enterprise or Motorola Solutions from the USA in the tech security sector?

- The niche: Axon focuses primarily on police (tasers, bodycams). INVISIO is the undisputed top dog in the field of tactical military communication in Europe.

- Diversification: We escape the constant tech focus of Wall Street and participate directly in the massive European and NATO internal armament cycle without having to buy direct defense companies (like Rheinmetall) if you don't want to for ethical reasons. INVISIO is "only" communication and protection!

📅 Important upcoming dates

For the watchlist or direct entry:

- May 06, 2026: Publication of the Q1 2026 earnings report (This will show how the order books continue to fill up).

- May 07, 2026: Expected ex-dividend day.

- May 13, 2026: Planned payment date (pay date) of the dividend.

⚖️ Opportunities and risks

Opportunities:

- Scalability: The asset-light model means that every additional million-euro order directly catapults earnings per share upwards with extremely little additional cost.

- Moat: The certification and procurement processes in the military often take 3-5 years. Once you are in the system as a standard supplier (like INVISIO for many NATO countries), you will not be replaced so quickly.

Risks:

- Valuation risk: A P/E ratio of over 60 does not forgive operational mistakes. If a major government contract fails to materialize or is delayed in parliament, the share price will plummet.

- Lumpy revenues risk: The business is dependent on a few, but huge, major contracts from governments. This often leads to very volatile quarterly results.

My conclusion: An absolute monster in a fast-growing niche. Not for the faint-hearted and not for the pure dividend hunter, but as a growth satellite in the portfolio a first-class choice from Sweden!

@Tenbagger2024 Is this risky enough for you? 😉

Looking forward to your opinions! Who already had INVISIO on their radar?

Maybe also something for the others like:

@Multibagger

@Get_Rich_or_Die_Tryin

@Klein-Anleger

@schlimmschlimm

@Derspekulant1

@SAUgut777

@Keineui