The tech sector is currently down quite a bit, which of course also offers opportunities for me as a buy and hold (and check) investor. In addition to the software sector due to AI fears, Nintendo, for example, has also $7974 (+2,5%) in the console market, for example, as they are currently struggling with various difficulties. I see this as a good opportunity and have further increased my position 😎✌🏻.

Nintendo

Azione

Azione

ISIN: JP3756600007

Ticker: 7974

JP3756600007

7974

Price

Discussione su 7974

Messaggi

72

4Mes·

Review February 2026

This time, a little earlier than in February, here is my review of February.

A good development but unfortunately also a premature sale.

📈 Performance:

S&P500: -0.36%

MSCI World: +1.05%

DAX: +3.04%

Dividend portfolio: +5.41%

My high and low performers in February were (top/flop 3):

🟢 ($8058 (-1,87%) ) Mitsubishi +29.13%

🟢 ($2768 (+0,12%) ) Sojitz +25.00%

🟢 ($HSY (+1,09%) ) Hershey +22.03%

🔴 ($D05 (-0,58%) ) DBS Group -5.56%

🔴 ($MSFT (+2,1%) ) Microsoft -7.95%

🔴 ($HTGC (+1,58%) ) Hercules Capital -16.33%

Dividends:

February 2026: €93.32

February 2025: € 137.56

Change: -32.16%

This change is partly due to the fact that Realty Income reclassified the 2024 dividend last year in February, resulting in a higher amount in February.

I also divested Medical Properties, which is why this dividend is of course no longer paid.

Sales:

🟥 United Health ($UNH (+2,01%) )

🟥 Lockheed Martin ($LMT (-0,51%) )

🟥 3M ($MMM (+3,27%) )

🟥 Tesla ($TSLA (-1,16%) )

🟥 Nintendo ($7974 (+2,5%) )

Purchases:

🟩 United Health ($UNH (+2,01%) )

🟩 Cisco Systems ($CSCO (+1,24%) )

🟩 VICI ($VICI (+0,85%) )

🟩 American Tower ($AMT (+4,91%) )

Savings plans:

($CTAS (+2,27%) ) Cintas (50€)

($MC (+2,21%) ) LVMH (50€)

($MSFT (+2,1%) ) Microsoft (25€)

As part of a smaller clean-up operation, I got rid of a few stocks that were really only a very small position in my portfolio. These include

- the remainder of Nintendo (only the profit was still running)

- 3M: Small position and dividend also too low

- Tesla: My foray into the tech world is over

I also sold Lockheed Martin. I thought it was a good time. The stock was doing well, but I think it will now gradually cool off. In addition, other defense companies are becoming more active and there will be more distribution here.

Unfortunately, I was wrong about that. In fact, I didn't believe that Iran would actually be attacked to this extent. I have therefore lost another 10% so far. Overall, however, this is not so tragic. I sold with a 30% gain and thus tidied up my portfolio further.

Last but not least, I sold United Health at around -30% to fill my loss pot and make the other sales tax-free. I then bought United Health again, together with an increase in VICI, American Tower and Cisco Systems.

What else has happened?

February was generally rather quiet, apart from the political tensions in the Middle East. These escalated towards the end of the month. We can expect an exciting March. In terms of performance, I am definitely satisfied. For the year as a whole, I am currently up 7.8%. The DAX is the closest pursuer with +3.2%.

I am still building up my nest egg. I didn't make any purchases in January and have only done the reallocations in February. This means I can definitely complete the build-up in April and invest a little more again from then on, although I am more likely to be building up cash at the moment.

At the end of the month I realized that my Payback had been hacked (or whatever) and 13,000 points were stolen or redeemed. Annoying... That's what happens when you don't have 2FA activated. But Payback still doesn't seem quite so secure to me. Incidentally, you don't need to expect help from customer service. They generally just refer you to the police. Of course, there's no refund either.

Edit: Today, 03.03. the payback points are back. No idea why. I didn't get a message or anything but DM canceled it. So apparently customer service did react or DM noticed the fraud. No idea. Anyway, I paid out the points straight away 😅😂

🥅 Goals 2026:

I'm trying to reach €85,000 in my dividend portfolio this year. This is to be achieved through dividends, deposits and, of course, share price increases. Let's see what it looks like at the end of the year, as the start is rather sluggish. I'll have to make up for that over the course of the year.

Anyone who liked the report and would like to read more is welcome to follow me,

If you're not interested, you can keep scrolling or use the block function.

5Mes·

Trade Republic - Exemption order exhausted? Incorrect

I'm a bit confused right now.

At the beginning of the year, my €1000 exemption order was reset to €0 (as usual). So far everything is normal.

So far this year I have:

- a larger partial sale → $SHOP (+3,96%) with a profit of around €350

- a few dividends → under €150 in total

- I have even sold 4 positions in the red $MCD (+0,71%) & $7974 (+2,5%) & $LOTB (+0,93%) & $QDV5 (+0,75%) (about 150€ minus)

Means: I should be somewhere around ~350-400 € usage.

Nevertheless, Trade Republic shows me that my exemption order has already been exhausted.

In addition, I notice:

➡️ For about two weeks now, capital gains tax has been withheld on all dividends, as if the exemption amount had been completely used up.

This cannot be mathematically correct.

Have you ever experienced this?

- Display bug?

- Advance flat rate? I don't even see it yet

- Delay in the internal calculation?

- Or a known problem at Trade Republic?

Before I contact support, I wanted to hear whether this has already happened to you.

Thank you 🙏

64Posizioni

250.309,38 €

7,16%

33

9 Commenti

My guess is the upfront fee. They are now better hidden at TR, but I know that they have already done this for some ETFs from my own portfolio.

•

66

•

6Mes·

Sale MongoDB

At some point, it's time to call it a day and take the profits. Besides, I wanted to reduce my tech share anyway.

Profit flows into $7974 (+2,5%) and pharma top-ups $SDZ (+2,24%) & $SFZN. (+2,36%)

6Mes·

Nintendo bought!

Nintendo $7974 (+2,5%) has made it into my portfolio for several reasons. For decades, the company has been able to appeal to new generations of young gamers and at the same time build up an exceptionally high level of brand loyalty. The Switch console is currently still very popular and shows that Nintendo can be successful even without high-end hardware. A major advantage over competitors such as Xbox or PlayStation is that Nintendo is more profitable both in the console itself and in the accessories business.

Its own brands such as Mario, Pokémon and Zelda, which are known worldwide and regularly achieve high sales figures, are also particularly strong. In addition, Nintendo benefits from every game sale on the Switch platform, including third-party titles, which further strengthens the business model. This is complemented by growing online services with recurring revenues. In my view, the recent price setback offered an attractive entry point.

6Mes·

Review of December 2025

Here is my review of December 2025. I will probably also write a review of the year, where I will also go into more detail about the dividends. But that will probably take a few more days.

📈 Performance:

S&P500: -0.33%

MSCI World: +0.32%

DAX: +2.74%

Dividend portfolio: -1.55%

My high and low performers in November were (top/flop 3):

🟢 ($2318 (+0,63%) ) Ping An +15.65%

🟢 ($RIO (-0,73%) ) Rio Tinto +11.61%

🟢 ($2768 (+0,12%) ) Sojitz +7.15%

🔴 ($MMM (+3,27%) ) 3M -6,81%%

🔴 ($TSCO (-0,59%) ) Tractor Supply -8.45%

🔴 ($7974 (+2,5%) ) Nintendo -21.09%

Dividends:

December 2025: € 208.88

December 2024: € 185.64

Change: +12.52%

Sales:

🟥 ($MICC (+2,55%) ) The Magnum Ice Cream Company

Purchases:

🟩 ($HD (+2,4%) ) Home Depot (2 pcs.)

Savings plans:

($CTAS (+2,27%) ) Cintas (50€)

($MC (+2,21%) ) LVMH (50€)

($MSFT (+2,1%) ) Microsoft (25€)

What else has happened?

As is often the case in December, there are those who rush from one Christmas party to the next, constantly have appointments and can't find any peace and quiet even at Christmas.

Then there are those who take December very easy, have relaxed TV evenings, make the most of the nice weather during the day (if possible) and at least try to keep things quiet at Christmas. I belong to the latter and only belong to the former at Christmas. As a result, my December was pretty quiet except for the Christmas rush, where you're rushing from one meal to the next and from one relative to the next. With various birthdays around Christmas and between the years, the stress continues. Fortunately, I've been reserving Boxing Day for me and my wife for a few years now. We don't visit anyone there and don't want anyone with us. We just spend the whole day doing whatever we feel like doing. Apart from that, we have a quiet New Year's Eve and that's it for 2025.

🥅 Goals for 2025:

Deposit of €10,000 and thus a custody account volume in the share portfolio of ~€73,000

Target achievement at the end of October 2025: 91.56%

So I actually didn't quite reach my target, although the total investment I was aiming for (incl. pension portfolio & Oskar) of €20,000 was achieved.

Overall, I am quite satisfied with the year. In the annual review, as mentioned above, I will go into more detail about the dividends and the overall performance.

Anyone who enjoyed the report and would like to read more is welcome to follow me,

If you are not interested, you are welcome to scroll on or use the block function.

3131

43 Commenti

6Mes

First of all, all the best and priceless wishes for 2026 🤝

Even if the goals were just missed, you have achieved so much more in the meantime that you can look back on 2025 with pride and satisfaction 😉

So off to 2026, spit in your hands and on you go 👋🏻

Even if the goals were just missed, you have achieved so much more in the meantime that you can look back on 2025 with pride and satisfaction 😉

So off to 2026, spit in your hands and on you go 👋🏻

•

55

•

7Mes·

First purchase Nintendo

Margin pressure and a weak yen are currently putting pressure on Nintendo. First tranche (1/3 of target size) placed and savings plan set up. $CMG (+0%) Had to be removed from the portfolio earlier than planned after a strong rebound.

1717

8Mes·

Nintendo: From playground to blockbuster giant

$7974 (+2,5%) -President Shuntaro Furukawa explains that Nintendo is actively building a framework to regularly release films based on its brands in the future. Nintendo is not just a licensor, but is "deeply involved from planning to production".

Three confirmed films are mentioned - including The Super Mario Bros. Movie (2023), The Super Mario Galaxy Movie (2026) and The Legend of Zelda (2027) - with more projects in the pipeline.

55

8Mes·

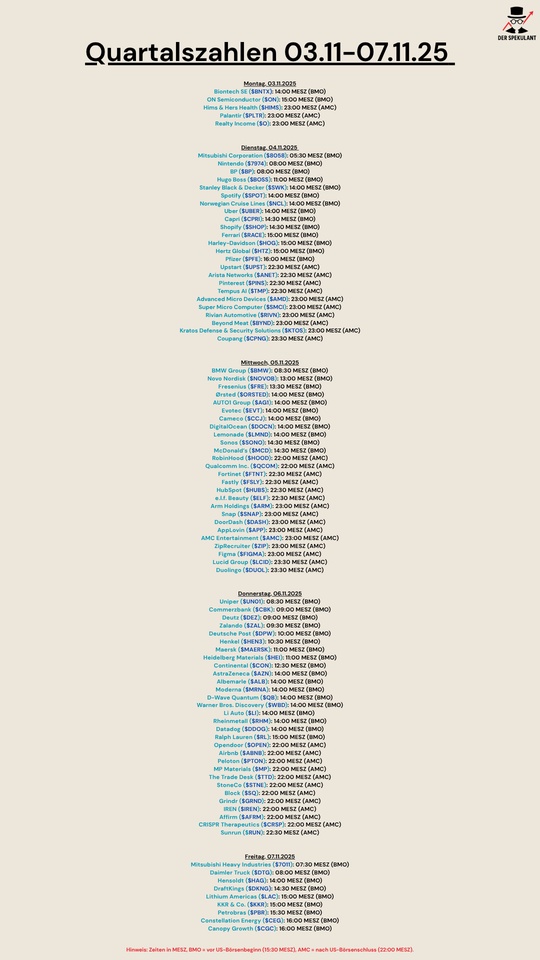

Quartalszahlen 03.11.25-07.11.15

$BNTX (+0,31%)

$ON (-4,82%)

$HIMS (-5,03%)

$PLTR (-5,92%)

$O (+0,09%)

$8058 (-1,87%)

$7974 (+2,5%)

$BP. (-1,71%)

$BOSS (+0,97%)

$SWK (+0,54%)

$SPOT (+2,87%)

$N1CL34

$UBER (+1,68%)

$CPRI (+3,27%)

$SHOP (+3,96%)

$RACE (+2,65%)

$HOG (+1,67%)

$HTZ (-7,55%)

$PFIZER

$UPST (-1,01%)

$ANET (-2,81%)

$PINS (+2,9%)

$TEM (-2,17%)

$AMD (-7,27%)

$SMCI (-5,5%)

$RIVN (-1,45%)

$BYND (-3,78%)

$KTOS (-3,22%)

$CPNG (-3,17%)

$BMW (+3,37%)

$NOVO B (+2,38%)

$FRE (+0,16%)

$ORSTED (-2,6%)

$AG1 (-2,88%)

$EVT (+1,53%)

$CCO (-3,6%)

$DOCN (-7,29%)

$LMND (+0,85%)

$SONO (+1,72%)

$MCD (+0,71%)

$HOOD (-3,29%)

$QCOM (-3,42%)

$FTNT (-0,52%)

$FSLY (+3,76%)

$HUBS (+5,73%)

$ELF (-0,54%)

$ARM (-8,02%)

$SNAP (+4,27%)

$DASH (+4,26%)

$APP (+0,29%)

$AMC (+3%)

$ZIP (+4,68%)

$FIG (+3,85%)

$LCID (+0%)

$DUOL

$UN0 (-2,18%)

$CBK (+0,04%)

$DEZ (-1,32%)

$ZAL (+3,44%)

$HEN (+2,05%)

$MAERSK A (+2,59%)

$HEI (-0,89%)

$CON (+1,61%)

$AZN (+0,95%)

$ALB (-2,79%)

$MRNA (-1,51%)

$QBTS (-8,48%)

$WBD (+0,74%)

$LI (+7,34%)

$RHM (+2,73%)

$DDOG (-1,34%)

$RL (+0,61%)

$OPEN (-0,21%)

$ABNB (+3,28%)

$PTON (+3,67%)

$MP (-5,17%)

$TTD (+4,89%)

$STNE (+1,76%)

$SQ (+1,58%)

$GRND (+5,13%)

$IREN (-7,18%)

$AFRM

$CRISP (-0,02%)

$RUN (-4,52%)

$7011 (-2,47%)

$DTG (+3,66%)

$HAG (+1,59%)

$DKNG (+0,47%)

$LAC (-3,52%)

$KKR (+0,25%)

$PETR3 (+0,37%)

$CEG

$WEED (-1,67%)

88