Dear colleagues,

I have now got over myself to make a stock presentation. Specifically, it is about $1347 (+0,47%) which I discovered through @Multibagger and which I find very exciting due to the national circumstances.

My investment theses are very much based on the Scuttlebutt method described below. This in turn stems from the investment legend Philipp A. Fisher and his son of the same name. I read the book "Common Stocks and Uncommon Profits". I have developed a Gemini Gem from the method described therein and would like to share it with you using $1347 (+0,47%) share it with you:

A. The company in simple words: The workbench of the Chinese electronics revolution

Hua Hong Semiconductor Limited acts as a specialized contract manufacturer within the global semiconductor value chain, a so-called pure-play foundry. While industry giants such as Intel and Samsung design their own chips, this company manufactures exclusively on behalf of external customers who do not have their own production facilities. In the world of semiconductors, however, the company has not dedicated itself to the risky and extremely costly race for the smallest structure widths for high-end processors, but rather occupies a strategically highly relevant niche: specialty technologies.

The business model is based on processing silicon wafers with specific physical properties that are crucial for applications beyond pure computing power. These include in particular power electronics (power discretes), which control the flow of electricity in electric vehicles, as well as embedded non-volatile memories (eNVM), analog and power management chips and radio frequency (RF) solutions for wireless communication. The company is the second largest foundry in mainland China and the seventh largest in the world, and is a global leader especially in 8-inch wafer platforms. With the massive expansion into the 12-inch area at the Wuxi site and the planned full integration of its subsidiary Shanghai Huali (HLMC), the company is currently transforming itself from a pure specialist for mature nodes to a diversified supplier that also covers more advanced manufacturing processes down to 28nm and - as recent reports suggest - potentially 7nm.

I. Market potential for significant revenue growth over several years

The market potential must be analyzed in the context of China's global semiconductor self-sufficiency efforts and the transformative trends in the automotive and industrial sectors. The company addresses markets that are not only growing cyclically, but are also experiencing a structural surge in demand. In comparison to historical examples such as the Aluminum Company of America (Alcoa) or Du Pont, which dominated their industries through technological standardization and scaling, the company now acts as the infrastructural foundation for the Chinese transition to electromobility (EV) and the Industrial Internet of Things (IoT).

The core segment of power semiconductors is benefiting directly from the massive expansion of the EV market. In terms of value, a modern electric vehicle requires significantly more power electronics than a vehicle with an internal combustion engine in order to efficiently manage the battery currents and control the electric motors. As China is the world's largest market and producer of electric vehicles, the company is at the source of this demand. Beijing's strategic goal of increasing the domestic semiconductor self-sufficiency rate from around $18.3\%$ in 2022 to an estimated $26.6\%$ by 2027 acts as an artificial catalyst. This trend towards localization is further exacerbated by US export restrictions as Chinese design houses are forced to shift their production from foreign foundries such as TSMC or UMC to local suppliers.

The company's capacity expansions reflect this potential. With the completion of the first phase of Fab 9 in Wuxi ahead of schedule and the continuously high capacity utilization of $106.1\%$ in 2025, it shows that the market potential is currently limited by supply rather than demand. The integration of Shanghai Huali will open up additional sales potential of an estimated $680 million USD per year and provide access to high-end MCUs and analog mixed-signal products that penetrate deeper into the automotive supply chain.

Personal Positioning: The market potential is undoubtedly there and almost guaranteed by political mandates. Nevertheless, it must be critically noted that this potential is strongly focused on the Chinese domestic market. The dependence on government support programs and local EV demand creates a cluster risk. While Alcoa and Du Pont have conquered global markets, this growth is more a result of geopolitical isolation.

Rating: 5 / 5

II Management's commitment to continuous product development

The management demonstrates a clear determination to grow beyond the limits of the currently profitable 8-inch technologies. The strategic direction "8-inch + 12-inch" and "Advanced Specialty IC + Power Discrete" is not just a marketing slogan, but is underpinned by massive investments. The acquisition of Shanghai Huali (Fab 5) illustrates this commitment to technological evolution. With this step, the company has secured capacities in the 28nm to 55nm range, which are essential for modern embedded systems and complex analog chips.

The management's attitude towards consolidating the Chinese foundry landscape is particularly noteworthy. Instead of getting lost in destructive price competition for standard logic chips, the management is focusing on scaling existing specialty platforms to more modern wafer diameters. This minimizes the risk of a technological dead end. Once the growth potential for pure discrete components on 8-inch wafers has been exhausted, the company can offer its customers already validated 12-inch counterparts, which massively increases customer loyalty (lock-in effect).

However, a critical aspect of the management approach is the tendency towards prestigious projects under government pressure. The reported foray into 7nm production, which is being driven primarily by the subsidiary Huali and in cooperation with Huawei, is technologically impressive, but could strain economic rationality. Nevertheless, it shows that the management is willing to operate at the technological frontier in order to secure the long-term relevance of the company.

Personal positioning: The determination is palpable, but often seems politically driven rather than purely market-driven. The strategy of transferring mature processes into new applications (automotive, IoT) is classic Fisher and reduces the risk of technological obsolescence. The integration of Huali is the decisive test for the implementation of this vision.

Rating: 4 / 5

III Effectiveness of research and development efforts (R&D)

The effectiveness of R&D efforts can be seen from the speed with which new platforms are brought to market. Over the last ten years, the company has undergone a remarkable transformation. While 8-inch wafers were historically the backbone, by 2024 they contributed exactly $50.0\%$ of sales, meaning that 12-inch research has generated half of the business within a few years. R&D spending increased significantly in 2025, contributing to a $17.9\%$ increase in operating costs.

A "crash program" appears to be superficially present in 7nm development, as this technology was developed under high time pressure and technological sanctions. However, this development is based on the principles of multi-patterning using existing DUV lithography equipment, which is a direct continuation of proven physical techniques. This is in line with Fisher's ideal that R&D projects should learn economically applicable principles from existing lines.

However, the financial yield of the R&D organization is mixed. Despite rising sales ($2.4 billion USD in 2025), net profits have fallen to $54.9 million USD due to the high research intensity and associated upfront costs. This indicates that while R&D effectiveness is high in terms of technological output, economic monetization is delayed by the high fixed costs of new factories.

Key financial figures for R&D activities

FY 2024

FY 2025

Change in

Turnover (USD million)

$2.004,0$

$2.402,1$

$+19,9\%$

Operating costs (incl. R&D) (USD million)

$361,0$

$425,6$

$+17,9\%$

Gross margin (%)

$10,2\%$

$11,8\%$

$+1.6\%$ PP

Capacity utilization (%)

$n/a$

$106,1\%$

Excellent

Personal positioning: The R&D department delivers technological breakthroughs non-stop (see 12-inch ramp and 7nm piloting). But efficiency in Fisher's sense - i.e. the contribution to net profit - is currently masked by the sheer capital intensity of the projects. It's a race against time and depreciation. The 7nm effort is a technological must, but potentially an economic grave if yields don't rise quickly.

Rating: 3 / 5

IV. Quality of the sales organization

In a foundry, the sales organization is not a pure marketing team, but a group of technical application engineers (FAE). The company attaches great importance to the technical background of its sales staff. Recruitment profiles for sales positions often require a master's degree in microelectronics or electrical engineering, which ensures that salespeople understand the complex design challenges of their customers (e.g. Biren or Huawei).

Training is analogous to core production staff. There are structured programs for new recruits that teach both general and highly specialized technical skills. This depth in the sales process is critical to achieving "design wins" where a customer optimizes their chip architecture to the company's specific manufacturing parameters. Once won, such a customer is often tied up for years due to the high switching costs (re-design costs).

The effectiveness is reflected in the capacity utilization of over $100\%$ in 2025. An above-average sales organization manages to keep the fabs full even in phases of global uncertainty by deepening strategic partnerships with national champions such as Huawei and at the same time opening up new markets in the automotive industry.

Personal positioning: The sales organization is one of the strongest pillars. It benefits massively from the "Buy Chinese" sentiment. The technical expertise of the sales team minimizes friction losses between design and production. This is a clear competitive advantage over smaller competitors.

Rating: 4 / 5

V. Profitability and profit margin

The company's current profit margin is the most critical point of the analysis from Fisher's point of view. With a gross margin of only $11.8\%$ in the full year 2025 and a net margin in the low single digits, the company is far behind global competitors such as TSMC or specialized foundries such as Tower Semiconductor.

However, the age and current life cycle of the new factories must be taken into account. The company is in a phase of massive reinvestment. Much of the potential profits are being eroded by astronomical depreciation on the new 12-inch equipment. Although the gross margin increased from $10.2\%$ in 2024 to $11.8\%$ in 2025, it remains fragile.

The question is whether this low margin will be invested in the future. The data confirms this: The company reported Q4 2025 cash flow from operating activities of $246$ million USD, while capital expenditure (CapEx) was a massive $633.5$ million USD. The company is therefore "burning" operating cash flow in order to build up capacity for the coming years.

Personal positioning: Margins are currently "brutally" bad. A classic value investor would immediately wave goodbye here. But for a Fisher investor, the decisive factor is that the margin is not being squeezed by inefficiency, but by a deliberate expansion strategy. Nevertheless, the margin of safety here is extremely low. Any delay in the ramp-up of Fab 9 or the integration of Huali could push the company into the red.

Rating: 2 / 5

VI Measures to maintain or improve profit margins

The management is aware of the margin problem and is using several levers. One central point is product engineering. By shifting the mix towards more complex specialty platforms (such as 12-inch eNVM and automotive-grade Discretes), the company is trying to escape the commodity trap.

Another lever is pricing power in niche markets. In Q4 2025, the company was able to push through price increases for certain logic chips, as the global shortage of memory chips is tying up capacity and tightening supply for other mature nodes. In addition, the acquisition of Shanghai Huali aims to leverage sourcing synergies and spread fixed costs over a larger base. Huali is described as already profitable, which could help consolidated margins in the short term.

Finally, the company is optimizing its cost structure by integrating local equipment suppliers. Increasing the proportion of domestic machines in Fab 9B should not only increase sanction security, but also reduce maintenance and acquisition costs in the long term.

Personal positioning: The efforts are conclusive, but the headwinds from depreciation and labor costs are formidable. Improving margins to $13\% - 15\%$ (guidance for Q1 2026) is a first step, but far from outstanding profitability. The company needs to prove that it can maintain Specialty premiums even in an environment of increasing global capacity.

Rating: 3 / 5

VII Labor relations and personnel policy

The company's image as an employer is characterized by its role as a national beacon of hope. In Shanghai and Wuxi, the company is regarded as a prestigious employer that offers stability in a volatile sector. The company invests in comprehensive training programs and offers dual career paths, which promotes employee retention.

However, there are critical undertones. Labor costs increased significantly in 2025, indicating a fierce "war for talent" in the Chinese semiconductor industry. The management stated that operating costs were burdened by higher personnel expenses, among other things. In addition, the work culture in the industry (often referred to as "996" - 9am to 9pm, 6 days a week) is a burden on long-term staff satisfaction.

Nevertheless, staff turnover appears to be moderate compared to aggressive start-ups. The average management tenure of over seven years suggests that the company culture can retain experienced staff.

Personal positioning: Labor relations appear stable but are increasingly costly. The company must continually offer more to defend talent against competitors such as SMIC or government-sponsored start-ups. I don't see an "outstanding" relationship in Fisher's sense, rather a market necessity.

Rating: 3 / 5

VIII. Relationships with management (executive relations)

The management climate in the company appears professional and disciplined. A positive point in Fisher's view is the moderate remuneration structure of the top management. CEO Bai Peng's total remuneration of around $790,000 USD is almost modest compared to US peers or even other large Hong Kong companies. This speaks against a self-service mentality and in favor of a focus on long-term corporate goals.

However, there was a significant concentration of power at the end of 2025. Following the resignation of Tang Junjun, Bai Peng also took on the role of Chairman. While this may speed up decision-making, it reduces internal control (checks and balances). The integration of Shanghai Huali will show whether the executive team is able to bring together different corporate cultures and complex operational structures efficiently.

Personal positioning: The moderate pay is a very good sign. However, the concentration of power at the end of 2025 needs to be monitored. In a state-dominated environment like this, there is always a risk that political devotion will take precedence over operational criticism.

Rating: 4 / 5

IX. Depth of management and delegation of authority

The company has an experienced management team with an average tenure of $7.3$ years. This indicates solid succession planning and a good knowledge base in second and third level management. The existence of multiple executive vice presidents for different departments (e.g. Weiping Zhou, Guangping Hua) indicates a functional delegation of authority.

An important aspect at Fisher is the reaction to criticism. In recent earnings calls, management has been transparent about margin problems and the impact of write-downs. However, there is little evidence of how openly criticism from lower levels is actually communicated upwards. In the hierarchical Chinese corporate culture, this is often a weak point.

The development of leadership talent appears to be structurally embedded through the dual career paths (management vs. technical expert). This prevents capable engineers from being pushed into management roles for which they are not suited and at the same time keeps technical expertise within the company.

Personal positioning: The depth is there, but flexibility may be limited by government oversight. Delegation works well at the operational level, but strategic decisions often feel centralized.

Rating: 3 / 5

X. Cost analysis and invoice control

The company's cost control faces enormous challenges. The integration of 12-inch production and the associated complex supply chains require precise cost analysis. In 2025, the company reported significant asset impairments of over $800 million CNY, raising questions about the original valuation or the efficiency of certain investments.

In addition, there was regulatory guidance from the Securities and Futures Commission (SFC) in Hong Kong requiring a tightening of internal controls at listed companies, particularly with regard to the change of auditors and the handling of irregularities. Although this appears to be an industry-wide problem in Hong Kong, it must be viewed critically in the context of the company's complex shareholding structure.

On the positive side, the detailed reporting on capacity utilization and the impact of depreciation cycles on gross margin is positive. This enables investors to at least partially assess operating efficiency.

Personal positioning: The accounting looks solid on the outside, but the high impairments are a warning signal. In a company that benefits massively from government subsidies and tax breaks (which are often booked under "Other Income"), true operating efficiency is difficult to isolate.

Rating: 3 / 5

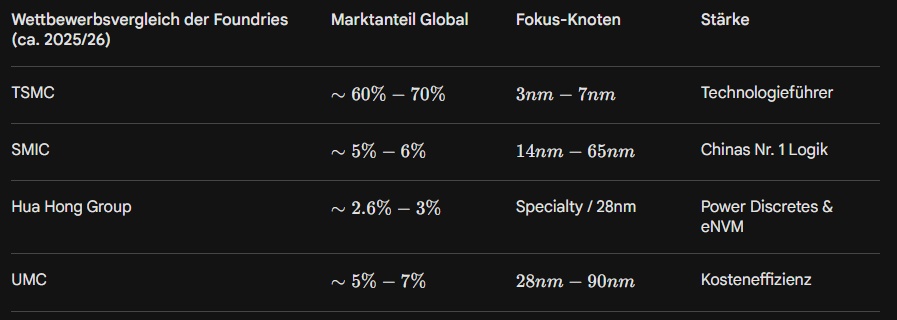

XI. Sector-specific characteristics and competitive advantages

The company's key competitive advantage lies in its role as a "safe haven" for mature and specialized semiconductor nodes in China. While global players such as TSMC focus on $<5$nm, this company occupies the 28nm to 180nm market, which is the volume backbone for automotive and industrial electronics.

Another feature is the access to the "Big Fund" and the close cooperation with national champions such as Huawei. These relationships not only guarantee capital, but also a stable pipeline of orders that foreign foundries lose due to political risks. The ability to pilot 7nm chips for AI applications (such as for Biren Technology) despite Western sanctions gives the company a special technological position within China.

Personal positioning: The company is a "national champion". Its greatest advantage is not a technical secret, but political protection and guaranteed market access in China. This is a formidable moat against Western competition, but at the same time makes the company hostage to geopolitics.

Rating: 5 / 5

XII Short-term or long-term profit orientation

The management consistently pursues a long-term strategy. The decision to invest massively in 12-inch capacity, even though this puts massive pressure on short-term profits and margins, is the best proof of this. The aim is to secure China's technological sovereignty and create a scalable platform for the next two decades.

The communication to investors repeatedly emphasizes the importance of the capacity expansion (Fab 9) and the technological upgrade through the Huali acquisition. Short-term quarterly results are often commented on in the context of these long-term investment cycles.

Personal positioning: The company acts on Fisher's ideal of long-term value creation. Today's dividend and margin are sacrificed for tomorrow's market dominance. For a short-term speculator this is frustrating, but for a long-term investor it is exactly the right thing to do.

Rating: 5 / 5

XIII Necessity of future equity financing

This is the "brutally honest" weak point for existing shareholders. Growth is bought at a high price through dilution. The company has raised massive amounts of equity several times in the past, most recently through the listing on the STAR Market in Shanghai.

The current acquisition of Shanghai Huali is being financed through the issue of $190.7 million new shares. In parallel, a further non-public issuance of RMB shares is planned to raise up to $7.55 billion CNY in support funds. This continuous increase in outstanding shares neutralizes a significant portion of the absolute earnings per share (EPS) growth. The number of shares could increase by up to $30\%$ after completion of the transactions.

Personal positioning: Growth eats its children. While the company grows massively in absolute terms, there is often little left over from EPS growth for the existing shareholder. This is a considerable risk for the long-term total return.

Rating: 1 / 5

XIV Transparency in times of crisis (Investor Relations)

Management communicates openly about successes (record sales in Q4 2025), but becomes more vague when it comes to setbacks. One example is the communication surrounding the 7nm development. While the success was celebrated, there were hardly any concrete details on yield rates or actual production costs under sanction conditions.

Even when it comes to US sanctions and inclusion on the Pentagon's "Military Company List", management usually limits itself to terse denials or references to the legal review. In phases of share price declines, such as those that occurred in May 2025 following disappointing guidance data, proactive communication was limited.

Personal positioning: IR work is professional, but politically filtered. You hear what the government and the stock market want to hear. Genuine operational problems are often hidden behind the veil of "strategic expansion" or "geopolitical uncertainty".

Rating: 2 / 5

XV. Management integrity

There is no evidence of unethical behavior or personal enrichment. The moderate remuneration of the management indicates a high level of integrity towards the shareholders. However, integrity must be defined in the Chinese context. The management is primarily loyal to the Chinese state and its strategic goals.

There is a potential conflict of interest in the "whitewash waiver" application for the Huali acquisition, which allows the major state shareholders to increase their stake without having to make a mandatory offer to all shareholders. This is legal, but shows that the interests of minority shareholders take second place to the Group's consolidation objectives.

Personal positioning: The management has integrity within the system in which it operates. But as a Western investor, you have to be aware that you are not the top priority. Being categorized as "military-related" by the Pentagon is a serious reputational and compliance risk.

Rating: 2 / 5

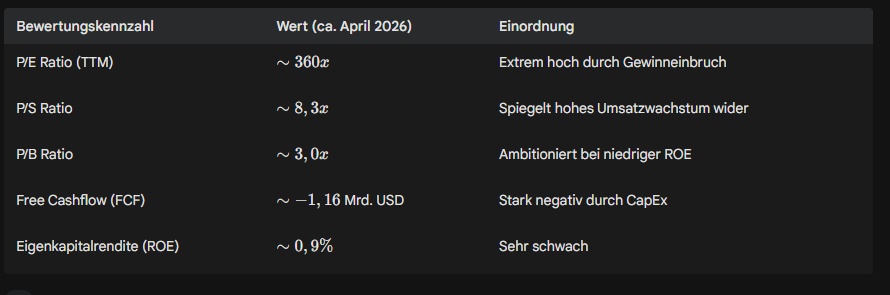

XVI Current rating and metrics

The valuation of the company is currently extremely distorted by the low profits and high investments. At first glance, the share looks absurdly expensive.

Personal positioning: Anyone buying here based on classic value metrics is making a mistake. The company must be viewed as a "growth turnaround". The high P/E ratio will only fall when the new fabs reach the profit zone and depreciation decreases. The negative FCF of over USD 1 billion is a warning signal for liquidity and makes further capital increases likely.

XVII. hype share?

The company was the subject of massive hype in March 2026 when rumors of 7nm manufacturing caused the share price in Hong Kong to rise by over $12\%$ in one day. The stock often serves as a proxy for the success of the Chinese semiconductor industry.

Nevertheless, it is not a pure "meme stock". The volatility is driven by real geopolitical events and fundamental news. The hype is real, but it is based on a strategic reality (self-sufficiency), not just hot air. The risk is to enter at the peak of a "national pride rally".

XVIII. Monopoly position and environment

The company does not enjoy a global monopoly, but a regional "protected oligopoly". Together with SMIC, it controls access to domestic contract manufacturing in China. In specific niches, such as power electronics on 8-inch wafers, the company is almost unrivaled within China in terms of capacity.

However, the environment is characterized by intense competition for standard chips. Chinese competitors such as Nexchip or Silan Microelectronics are also expanding, which can lead to price pressure on mature nodes. Government protection is the strongest environmental factor.

Summary report: Investment judgment Hua Hong Semiconductor

The company is a classic example of a strategic bet on China's technological sovereignty. From the perspective of a Fisher investor, the picture is ambivalent.

The critical points (brutally honest)

The biggest risk is ongoing dilution. The management uses the shareholder base as a cash machine for the national mission. If you buy today, you have to expect new shares to dilute your stake tomorrow. Profit margins are currently subterranean and offer no cushion for mistakes. The geopolitical exposure is extreme; a tightening of US sanctions (e.g. maintenance freeze for DUV systems) could paralyze the company operationally. Finally, the ROE of less than $1\%$ is a sign that capital is currently being deployed extremely inefficiently - at least from a purely business perspective.

The positive aspects (the opportunity)

The company operates in a market with almost unlimited demand (EV, IoT, Chinese self-sufficiency). The technological development is impressive; the piloting of 7nm shows that the company has not lost touch with the world leaders. The management has a long-term focus and does not pay excessive salaries. The capacity utilization of over $100\%$ proves that the company's products are in high demand on the market.

Overall verdict: The company is an excellent satellite investment for investors who believe in China's success in the semiconductor sector. However, it is not a "core pick" according to Fisher, as shareholder interests often take a back seat to national objectives. A buy is only recommended on significant setbacks when the valuation (P/B below 2x) better reflects the high cash burn. The 7nm news is a catalyst, but not yet a guarantee of earnings.

Analyst's position: Hold with focus on the Huali integration. A top-up should only be made when gross margins rise sustainably above $15\%$ and the wave of dilution subsides.