9% per year since purchase, driven largely by dividends

🚗🚗🚗

Messaggi

18🚗💨 🚗💨 🚗💨

In my opinion, Sixt is currently a perfect investment that will bear fruit in the long term, but as a German mid-cap it is currently still flying under the radar of major American investors.

Around a third of the European population lives in large cities. Urban mobility is changing in such a way that many city dwellers no longer own a car, but do not want to do without the advantages of a car in some situations, despite cycling and public transport.

You can see it every day on the streets - at least here in Munich: there is a MILES, ShareNow or Sixt Share vehicle on every corner. In recent months, Sixt has significantly increased its fleet and you now see almost more SIXTs than MILES. At the latest since Sixt cars can no longer be booked via the Miles app (and vice versa), there is now real competition and SIXT has the much better cards.

As a start-up, MILES is dependent on investor funds and, unlike a car rental company with decades of tradition and large cash reserves, has significantly worse conditions when purchasing vehicles, no well-established maintenance processes, no experience on the used car market and significantly less willingness to take risks.

In addition, Sixt can deploy its fleet much more flexibly. Depending on the situation, cars from Car-Sharing can also be quickly transferred to the classic rental business or to business customers, as Sixt is only developing Car-Sharing as a new line of business, while the existing business has long been tried and tested and runs like Swiss clockwork.

The fact that a large proportion of the shares are family-owned and that this family has often made forward-looking, intelligent decisions in recent decades also speaks in the company's favor. Innovations have not been overlooked. The spirit of the times was recognized early on: for example, Sixt tapped into the Internet back in the 90s.

One last, subjective point, which comes from the customer's point of view and should therefore not be underestimated: SIXT in Munich is currently cheaper than MILES (billing per minute vs. per kilometer), provided you are not stuck in a traffic jam. However, Sixt cars are usually in much better condition. A reversing camera is actually included in all of them. MILES is too stingy for such (comparatively inexpensive) special equipment; I have never experienced reversing cameras in the S and M segments. It seems to be just a small detail, but for me personally it makes parking a lot easier, and if I have to pay more for not having it, why should I? Competitor FreeNow, on the other hand, only offers Stellantis cars, so also operates far from what you could call premium. So Sixt has the better prices in spite of premium cars - and probably also has the better margins.

In a nutshell: In the long term, I see only one winner in car sharing in Germany, and that winner is Sixt. The car sharing market as a whole is likely to grow strongly in the coming years, even outside Germany. Sixt has long been active in all European countries with its classic car rental business, so it will be much easier for Sixt to expand car sharing than Miles; after all, the entire infrastructure for fleet maintenance, the development of local laws, etc. does not have to be built from scratch.

And even if the car-sharing bet should not work out for some reason: Sixt has an extremely solid foundation both in the B2B fleet business and as a traditional car rental company.

According to Warren Buffet, you should only invest in a business that you understand. And if I use a product myself regularly and am happy with it, and if it is a fairly new product that can appeal to significantly more people than before over the years, then I see it as a real gem, especially when it is still valued so low.

This is not an investment for short-term speculation, but I am firmly convinced that Sixt will provide a lot of pleasure in the coming years.

Do you think I'm looking at this all too much through rose-colored glasses, or do you agree with my assessment?

Stellantis, because it's mentioned in the text: $STLAM (-2,35%)

Source: Abilitato.de

Sixt is an established quality company that is expanding in the US - a clear growth driver. And yet the Sixt share appears undervalued: Trading only slightly above its value equity, with a P/E ratio of 8 and a dividend yield of 6%. A rare opportunity?

Buy a premium company. Pay economy.

Operational development

Sixt is an excellently managed and positioned quality company.

Thanks to its premium strategy, which sets it apart from the competition, the Group is able to shield itself from tough competition, enabling it to generate a return on equity of 16%.

Sixt continues to have ample opportunities for expansion, which means that there are also above-average prospects for value growth in the future.

In 2024, the car rental company had to contend with an adverse industry environment - in addition to a difficult economic situation and higher interest rates, a significant drop in residual vehicle values had a particularly noticeable impact on profitability (lower profits).

The problem has now been solved, meaning that particularly high earnings growth could be achieved in the next three years (analyst consensus until 2027: 19% annual EPS growth).

Valuation assessment

Despite the good growth prospects, the structurally high profitability and the princely balance sheet, the Sixt share is trading at a very low valuation:

Due to the cyclical business development, however, investors should also be prepared for increased price fluctuations and changing dividend payments in the future.

It is important to distinguish between temporary price movements and the risk of a permanent loss of capital (e.g. due to insolvency).

This risk appears to be very low, as Sixt is structurally profitable and has an extremely solid balance sheet that serves as a buffer.

Nevertheless, it is important to be sufficiently compensated for taking on the increased volatility - which is why the Sixt share should only be bought or increased if there is an attractive valuation.

The security is only suitable for investors who can deal with these fluctuations and even see an opportunity in them (from time to time there is an opportunity to top up at a reasonable price).

In principle, the Sixt share appears to be suitable for a buy-and-hold strategy, although in the past it has paid off to sell the shares again at a valuation of more than three times book value.

complete article:

We decided to go with the car rental company Sixt.

There were recently some unscheduled write-downs here. We think these are one-off effects and have therefore seen them as an exciting buying opportunity.

Sixt is a fairly reliable dividend payer and at the same time the family-run company is being continuously expanded. Sometimes with very cheeky but successful advertising campaigns. Subscription models in particular could ensure further growth in the future. Sixt manages to operate more profitably than traditional car manufacturers.

CAR RENTALS $SIX2 (+0,14%)

Sixt posts record sales

FY 2023 should end better than expected for car rental company Sixt.

At the beginning of the month, the Pullach-based company already specified its guidance for record revenue of EUR 3.6 billion (previously: "significant increase") and EBT of EUR 460 to 500 million (previously: EUR 430 to 550 million). In the previous year, the Group achieved around EUR 3.1 billion or EUR 386 million. The figures were well received on the stock market and the MDAX share (EUR 91.95; DE0007231326) has since risen by 8%.

After benefiting from a shortage of vehicles on the market in the previous year, Sixt has expanded its own fleet to a record 168,300 vehicles (+23%). This made it possible to better serve the high demand in the main vacation season. Although fleet costs, depreciation and interest expenses are rising due to the expansion of the vehicle fleet and rental prices are falling slightly, Sixt will be able to compensate for this thanks to generally high demand and impressive US growth (Q3: +13% revenue). The expansion in the USA is being accelerated by partnerships with the Los Angeles Lakers and the Chicago Bulls, among others.

The shareholder tariff of Sixt

Dear friends of non-cash dividends,

for more than 7 years I have been a very satisfied customer at the well known car rental company Sixt. As a result, I have been a (preferred) shareholder at Sixt for a good 5 years - a big argument for me was the shareholder rate that Sixt offers from the first share.

How much money I have saved so far I don't know, but probably significantly more than I have received in dividends over the last few years.

What is the Sixt shareholder rate?

I have already answered the question above:

To get this rate, you have to own at least one Sixt share, whether common or preferred.

In addition, you need a customer account with your own customer number, on which the tariff is deposited.

Finally, all you have to do is send a copy of the securities statement to the customer service department by e-mail (direct messaging via social media platforms is also possible), stating the customer number.

Thereupon, your booking profile will be set to "SHAREHOLDER Sixt AG" and you will receive up to 20% discount on your future bookings.

Sixt is not only cheeky in advertising

Sixt is known for its funny and sometimes very cheeky advertising, an example see here: Sixt kürt Claus Weselsky zum Mitarbeiter des Monats

But Sixt can also be cheeky in other ways.

To say it right away: Of course, the discount is, as always, the "up to" is to be considered. So it is not guaranteed that you always get 20% discount, I used to be mostly so between 10% and 15%.

I also think that if you have a special rate and you get it for free because you are a shareholder, you don't have the right to complain if you don't get a discount.

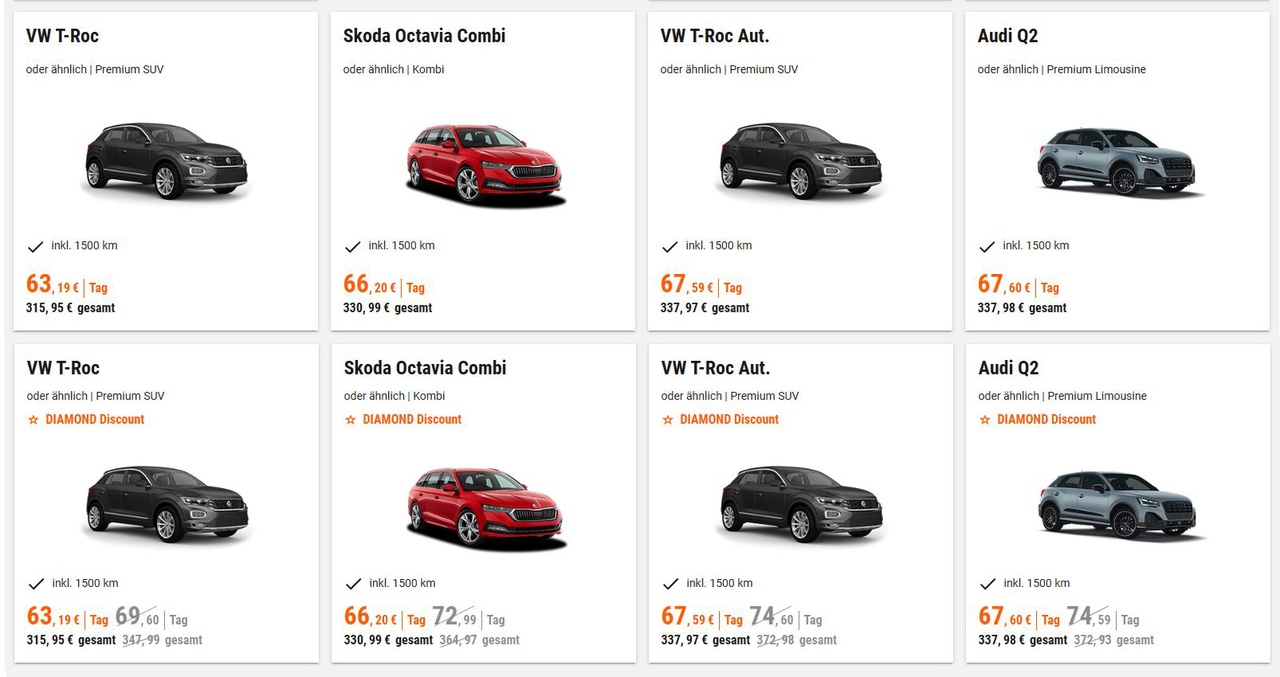

But: What I find incredibly brazen is what you see in the screenshot below.

The top row is the search when unannounced at the Sixt station in my city looking for rental cars over Christmas.

The bottom row shows the exact same search, just logged in as a shareholder.

These offers are exemplary, the same applies to all 28 search results.

As I said not giving a discount is fine in my opinion, but pretending to get a discount by showing a fictitious higher price crossed out is different cheeky. 😂😂😂