So today I jumped in with my first batch $HACK (+0,6 %) . May the stock market gods be with us... 😂😇

HAC

Hacksaw AB

Action

Action

ISIN: SE0025138357

Ticker: HACK

SE0025138357

HACK

Price

Discussion sur HACK

Postes

61H·

Actions speak louder than words

3J·

"Growth engine with increasing dividend power."

To give you a good start to the trading week, there will be a second company presentation this evening.

Dynamic sales and profit growth meets an annually growing dividend - a rare combination of scaling and shareholder return.

Hello my dears,

Yesterday dear @Dividendenopi promised me a jar of homemade jam. That's why I went looking for another dividend stock.

The stock I found in Sweden surprised me.

And here I ask myself, is this the Juan's conclusion once again too euphoric.

Is there a fly in the ointment here that we have overlooked, or have investors simply been blind so far?

Many people often accuse Juan of being too young and optimistic in his valuations.

That's why I'm looking forward to your comments all the more.

I am urgently awaiting comments from.

@Dividendenopi , @Raketentoni , @Get_Rich_or_Die_Tryin , @Aktienhauptmeister

If no long hair is found here, I will consider liquidating my Mercedes Benz position and investing here. (no investment advice)

Disruptor in iGaming technology and game development

Hacksaw is active in the entire B2B iGaming value chain, from game development to distribution. Our clients are among the largest private and public iGaming operators in the industry.

Innovating the industry with our state-of-the-art RGS

Hacksaw's scalable and modular remote gaming server (RGS) platform, built on a modern codebase, enables rapid game development and distribution. The games developed by Hacksaw consist of digital slot machines, scratch cards and instant win games. Their momentum is driven by successful game launches and continued engagement from a growing player base.

Founded in 2018

Hacksaw was founded in 2018 and initially focused on developing the RGS platform. Since then, they have released a steady stream of games, such as digital slots, scratchcards and instant win games, built on the RGS and launched them in a growing number of jurisdictions. Furthermore, in 2023, they launched their RGS on a B2B basis, allowing third-party game studios to create games on their modern tech platform and distribute them across Hacksaw's wide distribution network.

Growth strategy

Hacksaw has historically grown with healthy profitability and is pursuing a strategy for continued profitable growth. They want to further strengthen their market position in the global iGaming market. The strategy consists of four main components:

- Product innovation

- Product innovation includes the introduction of new games and the ongoing development of the RGS platform to ensure a competitive, high-quality and differentiated product offering.

- Increasing commercialization

- Increased commercialization includes upselling to existing customers, acquiring new customers and commercial excellence as well as accelerating the roll-out of OpenRGS™ to external game developers.

- Increased global presence

- Leverage newly regulated markets and position for growth in markets where local licensing requirements are expected.

- Expanded scope

- Expansion into adjacent areas and further scalability of the business model.

Long-term financial targets and capital allocation policy

- Sales target>30% annual growth rate

- EBIT margin>80%

- Capital allocation policy>75%

of net profit to shareholders through dividends and/or share buy-backs

Hacksaw aims to return at least 75% of net profit to shareholders through dividends and/or share buybacks.

COMPANY PERFORMANCE

Hacksaw-Company-introduction-FY-2025-1.pdf

Hacksaw Gaming exceeds analysts' expectations in the first quarter

28,04,2026

(en.investing.com)

Hacksaw Gaming has reported 1st quarter significantly exceeded analysts' expectations. The turnover rose to € 57.6 millionwhich was 28 % YoY or 37% adjusted for currency effects and 5% above the consensus above consensus. Compared to the previous quarter, sales increased by a further 5 % increase.

The adjusted EBIT reached € 47.4 millionan increase of 27% YoY and 6% QoQand was 8 % above the analysts' estimate. The EBIT margin of 82.4 % also exceeded expectations.

In operational terms, Hacksaw published 27 new gamesexpanded the OpenRGS platform to 320 titles and increased the daily game rounds by 27 %. At the end of the quarter, the company had 176 million in net liquidity.

In terms of valuation, Hacksaw is currently valued at 7.7 times EV/EBITDA (2026) traded. The company confirms its long-term targets: >30% sales growth and >80% EBIT margin. In addition at least 75 % of the net profit flow back to shareholders via dividends or buybacks.

- NEWS

Hacksaw Gaming debütiert im Libanon mit BetArabia | Hacksaw Gaming

Friday, May 29, 2026

Hacksaw Gaming kündigt Partnerschaft mit Swiss Casinos an

- Dienstag, 12. Mai 2026

- Hacksaw begrüßt Aloha Gaming als neues Partnerstudio bei OpenRGS

- Hacksaw Gaming erweitert seine OpenRGS-Plattform weiter mit der Ergänzung von Aloha Gaming, einem Studio, das sich auf mutige, echte 3D-Slot-Erlebnisse mit innovativen Spielmechaniken spezialisiert hat.

Hacksaw Gaming kündigt Partnerschaft mit Mozzartbet in Rumänien an

MORE GREAT NEWS

Neueste Nachrichten | Hacksaw Gaming

Juan's conclusion on the key financial figures

(Basis: MarketScreener data from your current tab )

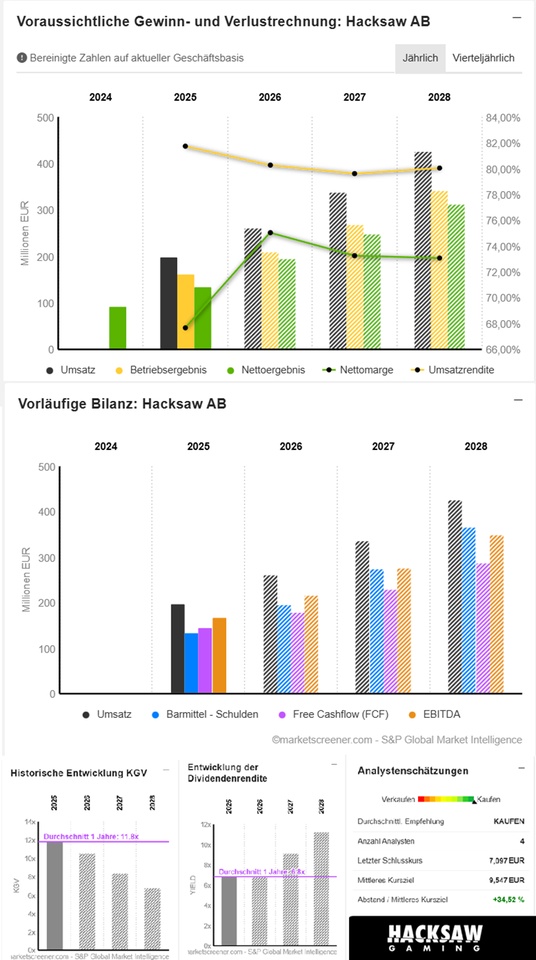

In a nutshell: Hacksaw delivers an extremely scalable, highly profitable growth model - with margins that seem almost "unrealistically good" in the software/iGaming world. The 2025-2028 forecasts show strong growth, rising cash flows, falling debt and an ROE that plays in the Champions League.

🔹 Juan's look at the figures for 2025-2028

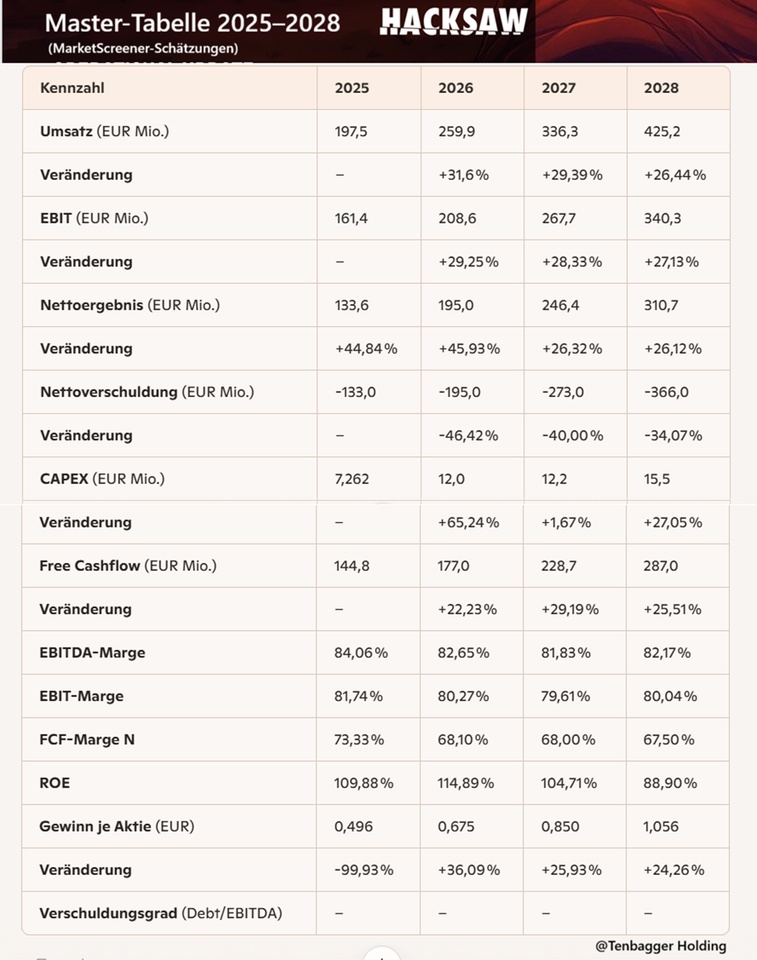

1) Growth & scaling

- Double-digit sales growth every year - +31,6 %, +29,4 %, +26,4 %.

- EBIT increases almost in step - a sign of real operational scaling.

- Net profit grows even faster than sales → Model becomes more efficient.

2) Profitability at top level

- EBITDA margin 82-84 %, EBIT margin ~80 % → This is software premium class.

- FCF margin remains >67 % → Cash machine.

- ROE remains extremely high (88-115 %) - return on capital is exceptional.

3) Cash flow & balance sheet

- Free cash flow increases from 144.8 → € 287 million.

- Net debt becomes more negative every year → Net cash position grows massively.

- CAPEX remains low → Model is capital poor.

4) Per share

- EPS grows solidly: 0,496 → 1,056 €.

- The extreme -99.93 % change in 2025 is a base effect by the distorted 2024 EPS (758).

🔹 Juan's overall assessment

Hacksaw is a prime example of a highly scalable, high-margin digital model. Growth + margins + cash flows + decreasing debt = Quality profile at a very high level. If the momentum holds, Hacksaw will remain a top-tier compounder in the iGaming B2B segment.

Market value 2,052

Number of shares (in thousands) 289,196

Date of publication 17,02,2026

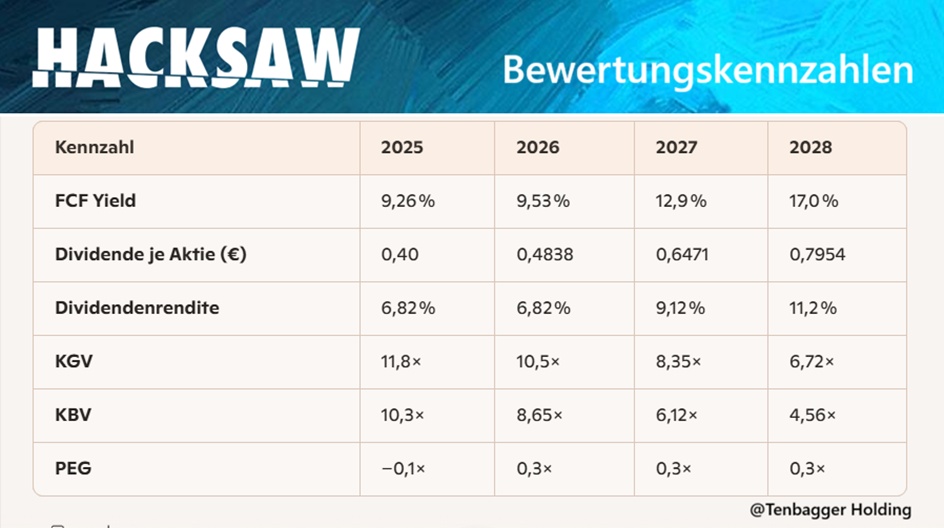

Juan's conclusion on the valuation ratios

(Basis: your current MarketScreener tab)

In a nutshell: Hacksaw looks like a quality stock that is simultaneously fast-growing and undervalued at the same time. The valuation metrics show a profile that typically only true compounders deliver.

🔹 Juan's view on the 2025-2028 valuation

1) FCF power meets attractive valuation

- A FCF yield of 9-17 % is exceptional for a fast-growing digital model.

- This means that the market is pricing growth growth far too conservatively too conservatively.

2) Dividend increases cleanly with

- Dividend per share grows every year → Shareholder return is steadily increasing.

- Dividend yield increases to 11 % → rare for a growth stock.

3) Multiples fall - even though the company is growing

- P/E ratio falls from 11.8× to 6.7× → Classic "multiple compression sweet spot".

- P/B ratio falls from 10.3× to 4.6× → Valuation becomes increasingly favorable relative to equity.

4) PEG shows clear undervaluation

- PEG by 0,3× → Market massively underestimates earnings growth.

- 2025 PEG is negative due to distorted EPS base effect.

🔹 Juan's overall assessment

Hacksaw combines growth, cash flow strength and falling multiples - a rare trio. The valuation ratios speak a clear language: The market is lagging operating reality. For Juan, this is a classic profile of an undervalued undervalued high-quality compounder.

🔶 Juan's conclusion (short & clear)

Hacksaw shows a valuation profile that rarely so clean clean: falling multiples, rising cash flows, growing dividends and an FCF yield that is expected to reach 17 % in 2028.

For Juan, this is a classic profile of a potential compounder with tenbagger DNA.

05.06.2026, 22:02:56 -

Tradegate BSX (EUR)

7.110 EUR

+ 4

77

8 Commentaires

Get_Rich_or_Die_Tryin@Get_Rich_or_Die_Tryin

1H

•

22

•Voir toutes les 5 autres réponses

3J·

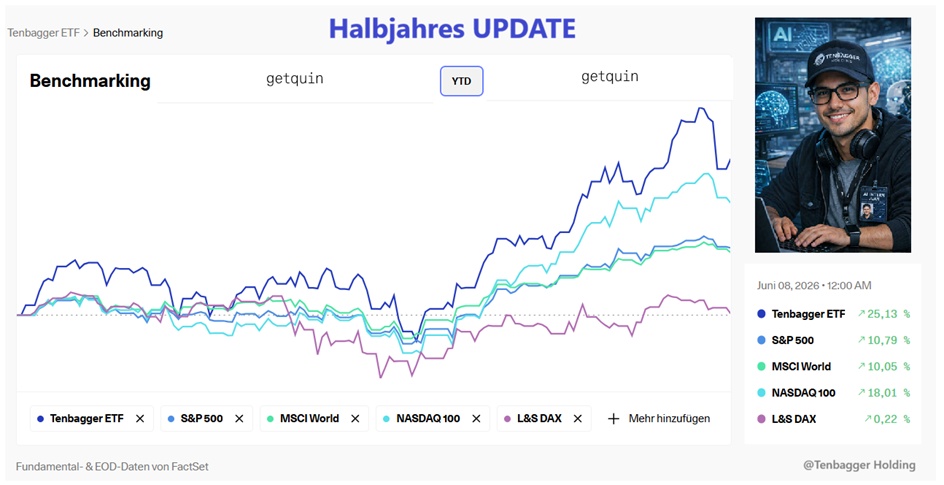

5 month UPDATE

Hello my dears,

The half-year is almost over, so I would like to give you an update.

If you like this type of update, please send me a 👍 to confirm.

There was a rebalancing today.

- Mercedes and Linde were sold -

- As soon as @Dividendenopi the check of $HACK (+0,6 %) HACHSAW has been completed, the stock will flow into my portfolio.

The background would be:

- Dividend stocks are exchanged in order to achieve a better dividend yield with the expected share price performance.

I am satisfied with the half-year results.

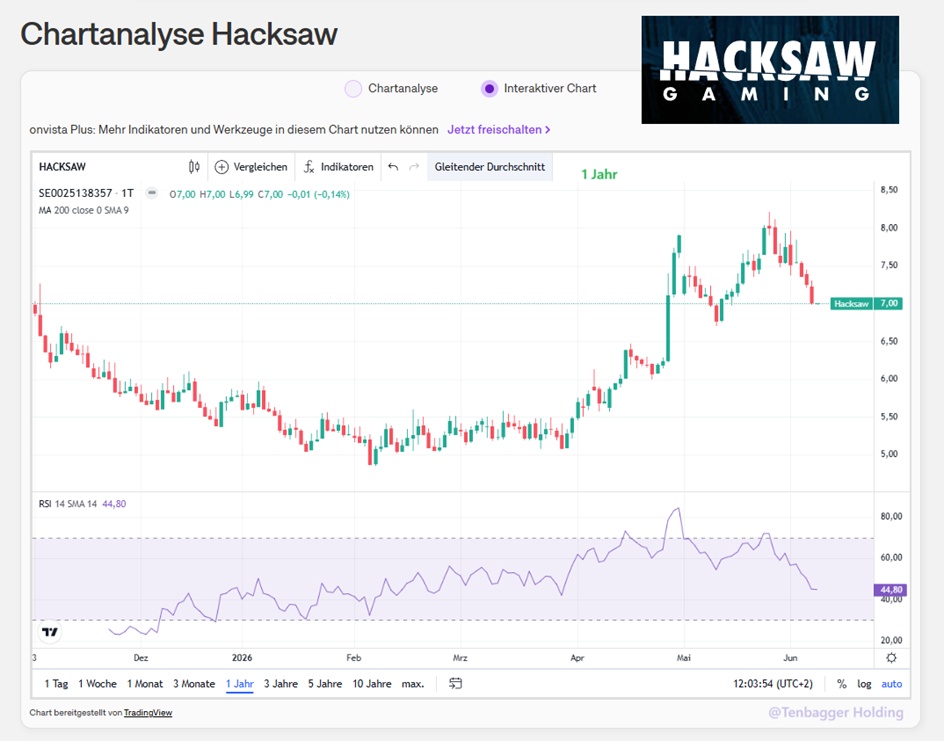

As you can see from the chart on Friday:

- Is my portfolio significantly more volatile, whether up or down -.

So this is not a portfolio that should be suitable for everyone.

Dear all, how satisfied are you with your YTD results?

6363

37 CommentairesI don't know. My semester isn't even over yet🤔

•

77

•3J·

"Growth engine with increasing dividend power."

To give you a good start to the trading week, there will be a second company presentation this evening.

Dynamic sales and profit growth meets an annually growing dividend - a rare combination of scaling and shareholder return.

Hello my dears,

Yesterday dear @Dividendenopi promised me a jar of homemade jam. That's why I went looking for another dividend stock.

The stock I found in Sweden surprised me.

And here I ask myself, is this the Juan's conclusion once again too euphoric.

Is there a fly in the ointment here that we have overlooked, or have investors simply been blind so far?

Many people often accuse Juan of being too young and optimistic in his valuations.

That's why I'm looking forward to your comments all the more.

I am urgently awaiting comments from.

@Dividendenopi , @Raketentoni , @Get_Rich_or_Die_Tryin , @Aktienhauptmeister

If no long hair is found here, I will consider liquidating my Mercedes Benz position and investing here. (no investment advice)

Disruptor in iGaming technology and game development

Hacksaw is active in the entire B2B iGaming value chain, from game development to distribution. Our clients are among the largest private and public iGaming operators in the industry.

Innovating the industry with our state-of-the-art RGS

Hacksaw's scalable and modular remote gaming server (RGS) platform, built on a modern codebase, enables rapid game development and distribution. The games developed by Hacksaw consist of digital slot machines, scratch cards and instant win games. Their momentum is driven by successful game launches and continued engagement from a growing player base.

Founded in 2018

Hacksaw was founded in 2018 and initially focused on developing the RGS platform. Since then, they have released a steady stream of games, such as digital slots, scratchcards and instant win games, built on the RGS and launched them in a growing number of jurisdictions. Furthermore, in 2023, they launched their RGS on a B2B basis, allowing third-party game studios to create games on their modern tech platform and distribute them across Hacksaw's wide distribution network.

Growth strategy

Hacksaw has historically grown with healthy profitability and is pursuing a strategy for continued profitable growth. They want to further strengthen their market position in the global iGaming market. The strategy consists of four main components:

- Product innovation

- Product innovation includes the introduction of new games and the ongoing development of the RGS platform to ensure a competitive, high-quality and differentiated product offering.

- Increasing commercialization

- Increased commercialization includes upselling to existing customers, acquiring new customers and commercial excellence as well as accelerating the roll-out of OpenRGS™ to external game developers.

- Increased global presence

- Leverage newly regulated markets and position for growth in markets where local licensing requirements are expected.

- Expanded scope

- Expansion into adjacent areas and further scalability of the business model.

Long-term financial targets and capital allocation policy

- Sales target>30% annual growth rate

- EBIT margin>80%

- Capital allocation policy>75%

of net profit to shareholders through dividends and/or share buy-backs

Hacksaw aims to return at least 75% of net profit to shareholders through dividends and/or share buybacks.

COMPANY PERFORMANCE

Hacksaw-Company-introduction-FY-2025-1.pdf

Hacksaw Gaming exceeds analysts' expectations in the first quarter

28,04,2026

(en.investing.com)

Hacksaw Gaming has reported 1st quarter significantly exceeded analysts' expectations. The turnover rose to € 57.6 millionwhich was 28 % YoY or 37% adjusted for currency effects and 5% above the consensus above consensus. Compared to the previous quarter, sales increased by a further 5 % increase.

The adjusted EBIT reached € 47.4 millionan increase of 27% YoY and 6% QoQand was 8 % above the analysts' estimate. The EBIT margin of 82.4 % also exceeded expectations.

In operational terms, Hacksaw published 27 new gamesexpanded the OpenRGS platform to 320 titles and increased the daily game rounds by 27 %. At the end of the quarter, the company had 176 million in net liquidity.

In terms of valuation, Hacksaw is currently valued at 7.7 times EV/EBITDA (2026) traded. The company confirms its long-term targets: >30% sales growth and >80% EBIT margin. In addition at least 75 % of the net profit flow back to shareholders via dividends or buybacks.

- NEWS

Hacksaw Gaming debütiert im Libanon mit BetArabia | Hacksaw Gaming

Friday, May 29, 2026

Hacksaw Gaming kündigt Partnerschaft mit Swiss Casinos an

- Dienstag, 12. Mai 2026

- Hacksaw begrüßt Aloha Gaming als neues Partnerstudio bei OpenRGS

- Hacksaw Gaming erweitert seine OpenRGS-Plattform weiter mit der Ergänzung von Aloha Gaming, einem Studio, das sich auf mutige, echte 3D-Slot-Erlebnisse mit innovativen Spielmechaniken spezialisiert hat.

Hacksaw Gaming kündigt Partnerschaft mit Mozzartbet in Rumänien an

MORE GREAT NEWS

Neueste Nachrichten | Hacksaw Gaming

Juan's conclusion on the key financial figures

(Basis: MarketScreener data from your current tab )

In a nutshell: Hacksaw delivers an extremely scalable, highly profitable growth model - with margins that seem almost "unrealistically good" in the software/iGaming world. The 2025-2028 forecasts show strong growth, rising cash flows, falling debt and an ROE that plays in the Champions League.

🔹 Juan's look at the figures for 2025-2028

1) Growth & scaling

- Double-digit sales growth every year - +31,6 %, +29,4 %, +26,4 %.

- EBIT increases almost in step - a sign of real operational scaling.

- Net profit grows even faster than sales → Model becomes more efficient.

2) Profitability at top level

- EBITDA margin 82-84 %, EBIT margin ~80 % → This is software premium class.

- FCF margin remains >67 % → Cash machine.

- ROE remains extremely high (88-115 %) - return on capital is exceptional.

3) Cash flow & balance sheet

- Free cash flow increases from 144.8 → € 287 million.

- Net debt becomes more negative every year → Net cash position grows massively.

- CAPEX remains low → Model is capital poor.

4) Per share

- EPS grows solidly: 0,496 → 1,056 €.

- The extreme -99.93 % change in 2025 is a base effect by the distorted 2024 EPS (758).

🔹 Juan's overall assessment

Hacksaw is a prime example of a highly scalable, high-margin digital model. Growth + margins + cash flows + decreasing debt = Quality profile at a very high level. If the momentum holds, Hacksaw will remain a top-tier compounder in the iGaming B2B segment.

Market value 2,052

Number of shares (in thousands) 289,196

Date of publication 17,02,2026

Juan's conclusion on the valuation ratios

(Basis: your current MarketScreener tab)

In a nutshell: Hacksaw looks like a quality stock that is simultaneously fast-growing and undervalued at the same time. The valuation metrics show a profile that typically only true compounders deliver.

🔹 Juan's view on the 2025-2028 valuation

1) FCF power meets attractive valuation

- A FCF yield of 9-17 % is exceptional for a fast-growing digital model.

- This means that the market is pricing growth growth far too conservatively too conservatively.

2) Dividend increases cleanly with

- Dividend per share grows every year → Shareholder return is steadily increasing.

- Dividend yield increases to 11 % → rare for a growth stock.

3) Multiples fall - even though the company is growing

- P/E ratio falls from 11.8× to 6.7× → Classic "multiple compression sweet spot".

- P/B ratio falls from 10.3× to 4.6× → Valuation becomes increasingly favorable relative to equity.

4) PEG shows clear undervaluation

- PEG by 0,3× → Market massively underestimates earnings growth.

- 2025 PEG is negative due to distorted EPS base effect.

🔹 Juan's overall assessment

Hacksaw combines growth, cash flow strength and falling multiples - a rare trio. The valuation ratios speak a clear language: The market is lagging operating reality. For Juan, this is a classic profile of an undervalued undervalued high-quality compounder.

🔶 Juan's conclusion (short & clear)

Hacksaw shows a valuation profile that rarely so clean clean: falling multiples, rising cash flows, growing dividends and an FCF yield that is expected to reach 17 % in 2028.

For Juan, this is a classic profile of a potential compounder with tenbagger DNA.

05.06.2026, 22:02:56 -

Tradegate BSX (EUR)

7.110 EUR

+ 4

3535

38 Commentaires

This is a really nice share for the dividend topi, thank you very much for your effort and for presenting it. Of course, that's an extra jar of jam 😇😉. I don't need to say much more about the figures, they speak for themselves and have already been commented on in detail. The topic of regulation has been addressed. In IGaming, this is a very fragmented issue and each market has its own requirements. Hackshaw is already well organized here and has the relevant experience. In the long term, this leads to customer loyalty, less competition due to barriers to entry and corresponding margins. This is where the capex is increasingly flowing, especially in the modularization of the platform to open up the various markets and pay the license fees. I see the expanded focus on the USA and Brazil as positive and will have a corresponding impact on the overall result. However, regulation is not only a risk factor but also a moat. Smaller providers, even if they are regionally limited, will hardly be able to overcome these hurdles and the large established providers will dominate the market. Countries such as the UK, Sweden, Ontario and soon Brazil offer clear rules, predictable revenues and reliable partners in the form of licensed casinos. This is predictable and leads to better multiples. Of course, a change in regulations can also temporarily dampen growth, but I don't see this as a sticking point. The second point that was mentioned is the departure of CEO and founder Källberg. This is temporarily causing a certain amount of uncertainty, as can be seen from the share price performance. The market just doesn't like surprises. I don't see this as dramatic and it does happen in such phases. There were also no negative signals, communication was clear, there were no compliance problems, no scandal, no operational crisis. Källberg built up the organization, carried out a successful IPO and the figures were great. The build-up phase is now complete and the company is moving one step further, with a clear focus on further significant growth. The change may well have been strategic. Away from the founding genes, towards corporate genes. Of course, a lot depends on the successor, ideally with experience in the industry. And the future strategic direction can already be seen. The interim CEO with M&A experience and the founding of Hackshaw Ventures indicate the direction in which things will increasingly be heading. For me at least, the brief uncertainty is a good time to put my foot in the door and get in with a first tranche.

•

55

•

4Sem.·

The "Garbage Collector" Portfolio 🚮 - 2ⁿᵈ pick - Flutter Entertainment

Today I decided to sell a good performer of mine and reallocate profits into the right now hated sector of gambling.

Gambling as a sector is going through a lot of pressure right now mainly because of 2 factors:

- Competitors in the predictions markets space like Polymarket and Kalshi

- Increasing Tax and regulation concerns

Big companies like $DKNG (+2 %) , $PENN (+1,35 %) , $ENT (+0,76 %) and $FLTR (+0,51 %) are collapsing in the stock market because of these fears.

Why I chose to buy Flutter Entertainment $FLTR (+0,51 %) then?

Flutter operates both online betting and in retail stores around the world.

It operates more or less like a serial acquirer in the gambling sector.

1) Flutter is market leader in mutiple markets around the world and is currently using the cash flow produced from mature and profitable markets like Italy, Uk, Australia and Ireland to finance is expansion in high-growing markets like Brasil and the USA.

Fanduel has over 40% marketshare in the USA and NSX Group (owned by Flutter) is the leading brand in Brasil.

It is market leader in a lot of developing countries like Turkey and Morocco throught the brand Sisal, in Georgia and Armenia through the brands Adjarabets.

Brazil and USA only recently allowed online gambling bets that's why Flutter is spending a lot of money to quickly capture market share in both these new 2 countries.

2) It recently started a parternship with financial giant $CME (+0,63 %) to provide market prediction directly in Fanduel to compete against Polymarket

3) The Turkey case: Recently Turkey decided to close all illegal online betting websites and that cause an increase of revenue of over 30% for Flutter in the region.

Flutter is a highly regulated entity who collaborate not only with professional leagues but also with nations across the world and that alone made Flutter the favourite default choice.

4) $AMZN (+0,81 %) Partenrship: In the USA now you can bet directly into the Prime app ecosystems during sports events increasing the fluidity and the experience for customers.

5) The Morocco case: in Morocco it operates through the brand Sisal but government allow only the national lottery. Flutter only provides the software and all the payout is in the hand of the local government.

That's a high recurring, high margin revnue model that can be potentially exported in other markets

6) Margin compression: Flutter is investing heavily in USA and Brazìl and that's why margin are compressing, however this are temporary costs linked to promotions, advertising etc...

7) The India case: India recently banned online betting in every form and Flutter lost a big market there.

However it still operates as a gaming platform with mobile phone games (with no money bets) and hoping that one day regulation will change.

If regulation changes in the future Flutter already has customers, games and distribution.

It is currently using the indian market as a test market for different type of games.

Yes, it is an unprofitable market for obvious reasons.

8) Flutter has the biggest selection of high quality casino games produced by market leaders like $HACK (+0,6 %) and $EVO (+1,58 %) and it's the platform who offers most games.

Casino games are important because they represent the most profitable chunk of the revenue.

9) Macroevents like the Football world cup will instantly increase demand for betting in all markets.

It's the biggest competition in the world and now for the firs time it has more teams who partecipates than ever.

10) Online betting has a TAM of approximately 300bln$ worldwide, flutter currently has 16bln$ revenue so the unpenetrated market opportunities are still huge.

Flutter is also the only gambling company who operates as a serial acquirer around the world and have a presence in almost every country in the world.

11) Recently England increased taxes on betting and that hit direclty Flutter's EBITDA margins, however the compnay is still profitable and market regulation is an intrinsic risk in the sector that cannot be erased, but only reduced thanks to geographic diversification.

12) The company is trading at the same price it was trading in 2017 however the business as a whole improved a lot both in terms of revenue and geographic expansions.

13) Debt is high due to the acquisitions like Snai in Italy, Fanduel in Usa and NSX in Brasil.

During the conference call Management said that it stopped the acquistion spree and is now focused to pay down debt and increase profitability.

It started by removing bonus and decreasing marketing costs in the USA, Italy and UK.

Even after cutting marketing costs customers still increased (On the earnings presentation it shows a decrease in number of users because they removed the indian market due to regulations, if you adjust the data it shows a significative increase).

55

1Mo·

scam or tenbagger

Nice rise after figures today at $HACK (+0,6 %)

The company has almost no debt, a PEG of 0.4 and a net margin of 76%, which is quite high for a gaming company. I'm still looking for the hook at 12 P/E and net income of +51% YoY, but haven't been able to find anything yet.

Other key figures:

-79 new deals in the quarter

-12 new own games, 15 third-party titles

-New license in Connecticut (USA) - Important step into a regulated market

-Investment in Jinx Gaming to strengthen the ecosystem

1Mo·

Shares Screener

Good evening,

Since this is also about shares such as $MILDEF (+0,81 %) of the good @Tenbagger2024 I wanted to show you the results of my stock search. Once a quarter I screen for stocks with the desired prerequisites. Maybe there is something for one or the other, just to whet your appetite. I always find companies with less than 5 billion Mcap particularly interesting, as relatively little capital is needed to move the share price. In addition, these companies are often under the radar of many analysts/investors. The following was entered in the search mask:

Revenue Forward 2Y CAGR >> at least +20%

EBITDA Forward 2Y CAGR >> at least +20%

PEG between 0.2 and 1.0 (company potentially undervalued -> growing faster than its valuation justifies)

Region: US / Sweden

I myself found the list exciting:

bounced off the top of the 200

new impulse after long -71% correction

new higher highs after 2 years of correction. RSI also turns upwards.

Monthly chart with massive momentum. Chart reminds of $DTE (-2,02 %)

Still no signs of bearish divergences in the monthly.

+ 6

77

7 Commentaires

1Mo

You know that if something is too good to be true, then it usually isn't true. 🤷

•

55

•1Mo·

Shares Screener

Good evening,

Since this is also about shares such as $MILDEF (+0,81 %) of the good @Tenbagger2024 I wanted to show you the results of my stock search. Once a quarter I screen for stocks with the desired prerequisites. Maybe there is something for one or the other, just to whet your appetite. I always find companies with less than 5 billion Mcap particularly interesting, as relatively little capital is needed to move the share price. In addition, these companies are often under the radar of many analysts/investors. The following was entered in the search mask:

Revenue Forward 2Y CAGR >> at least +20%

EBITDA Forward 2Y CAGR >> at least +20%

PEG between 0.2 and 1.0 (company potentially undervalued -> growing faster than its valuation justifies)

Region: US / Sweden

I myself found the list exciting:

bounced off the top of the 200

new impulse after long -71% correction

new higher highs after 2 years of correction. RSI also turns upwards.

Monthly chart with massive momentum. Chart reminds of $DTE (-2,02 %)

Still no signs of bearish divergences in the monthly.

+ 6

1414

19 Commentaires

Thank you my dear. You always discover new great companies that way. I already had Babcock & Wilcox in the pipeline last year, but unfortunately I didn't get in.

•

22

•Titres populaires

Meilleurs créateurs cette semaine

Données en temps réel par LSX · Données financières de FactSet