To give you a good start to the trading week, there will be a second company presentation this evening.

Dynamic sales and profit growth meets an annually growing dividend - a rare combination of scaling and shareholder return.

Hello my dears,

Yesterday dear @Dividendenopi promised me a jar of homemade jam. That's why I went looking for another dividend stock.

The stock I found in Sweden surprised me.

And here I ask myself, is this the Juan's conclusion once again too euphoric.

Is there a fly in the ointment here that we have overlooked, or have investors simply been blind so far?

Many people often accuse Juan of being too young and optimistic in his valuations.

That's why I'm looking forward to your comments all the more.

I am urgently awaiting comments from.

@Dividendenopi , @Raketentoni , @Get_Rich_or_Die_Tryin , @Aktienhauptmeister

If no long hair is found here, I will consider liquidating my Mercedes Benz position and investing here. (no investment advice)

Disruptor in iGaming technology and game development

Hacksaw is active in the entire B2B iGaming value chain, from game development to distribution. Our clients are among the largest private and public iGaming operators in the industry.

Innovating the industry with our state-of-the-art RGS

Hacksaw's scalable and modular remote gaming server (RGS) platform, built on a modern codebase, enables rapid game development and distribution. The games developed by Hacksaw consist of digital slot machines, scratch cards and instant win games. Their momentum is driven by successful game launches and continued engagement from a growing player base.

Founded in 2018

Hacksaw was founded in 2018 and initially focused on developing the RGS platform. Since then, they have released a steady stream of games, such as digital slots, scratchcards and instant win games, built on the RGS and launched them in a growing number of jurisdictions. Furthermore, in 2023, they launched their RGS on a B2B basis, allowing third-party game studios to create games on their modern tech platform and distribute them across Hacksaw's wide distribution network.

Growth strategy

Hacksaw has historically grown with healthy profitability and is pursuing a strategy for continued profitable growth. They want to further strengthen their market position in the global iGaming market. The strategy consists of four main components:

- Product innovation

- Product innovation includes the introduction of new games and the ongoing development of the RGS platform to ensure a competitive, high-quality and differentiated product offering.

- Increasing commercialization

- Increased commercialization includes upselling to existing customers, acquiring new customers and commercial excellence as well as accelerating the roll-out of OpenRGS™ to external game developers.

- Increased global presence

- Leverage newly regulated markets and position for growth in markets where local licensing requirements are expected.

- Expanded scope

- Expansion into adjacent areas and further scalability of the business model.

Long-term financial targets and capital allocation policy

- Sales target>30% annual growth rate

- EBIT margin>80%

- Capital allocation policy>75%

of net profit to shareholders through dividends and/or share buy-backs

Hacksaw aims to return at least 75% of net profit to shareholders through dividends and/or share buybacks.

COMPANY PERFORMANCE

Hacksaw-Company-introduction-FY-2025-1.pdf

Hacksaw Gaming exceeds analysts' expectations in the first quarter

28,04,2026

(en.investing.com)

Hacksaw Gaming has reported 1st quarter significantly exceeded analysts' expectations. The turnover rose to € 57.6 millionwhich was 28 % YoY or 37% adjusted for currency effects and 5% above the consensus above consensus. Compared to the previous quarter, sales increased by a further 5 % increase.

The adjusted EBIT reached € 47.4 millionan increase of 27% YoY and 6% QoQand was 8 % above the analysts' estimate. The EBIT margin of 82.4 % also exceeded expectations.

In operational terms, Hacksaw published 27 new gamesexpanded the OpenRGS platform to 320 titles and increased the daily game rounds by 27 %. At the end of the quarter, the company had 176 million in net liquidity.

In terms of valuation, Hacksaw is currently valued at 7.7 times EV/EBITDA (2026) traded. The company confirms its long-term targets: >30% sales growth and >80% EBIT margin. In addition at least 75 % of the net profit flow back to shareholders via dividends or buybacks.

- NEWS

Hacksaw Gaming debütiert im Libanon mit BetArabia | Hacksaw Gaming

Friday, May 29, 2026

Hacksaw Gaming kündigt Partnerschaft mit Swiss Casinos an

- Dienstag, 12. Mai 2026

- Hacksaw begrüßt Aloha Gaming als neues Partnerstudio bei OpenRGS

- Hacksaw Gaming erweitert seine OpenRGS-Plattform weiter mit der Ergänzung von Aloha Gaming, einem Studio, das sich auf mutige, echte 3D-Slot-Erlebnisse mit innovativen Spielmechaniken spezialisiert hat.

Hacksaw Gaming kündigt Partnerschaft mit Mozzartbet in Rumänien an

MORE GREAT NEWS

Neueste Nachrichten | Hacksaw Gaming

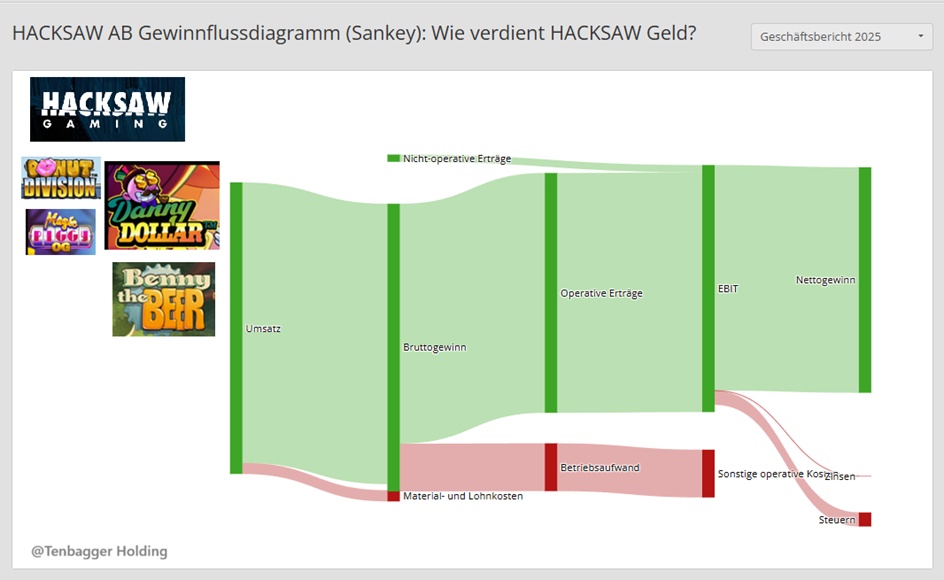

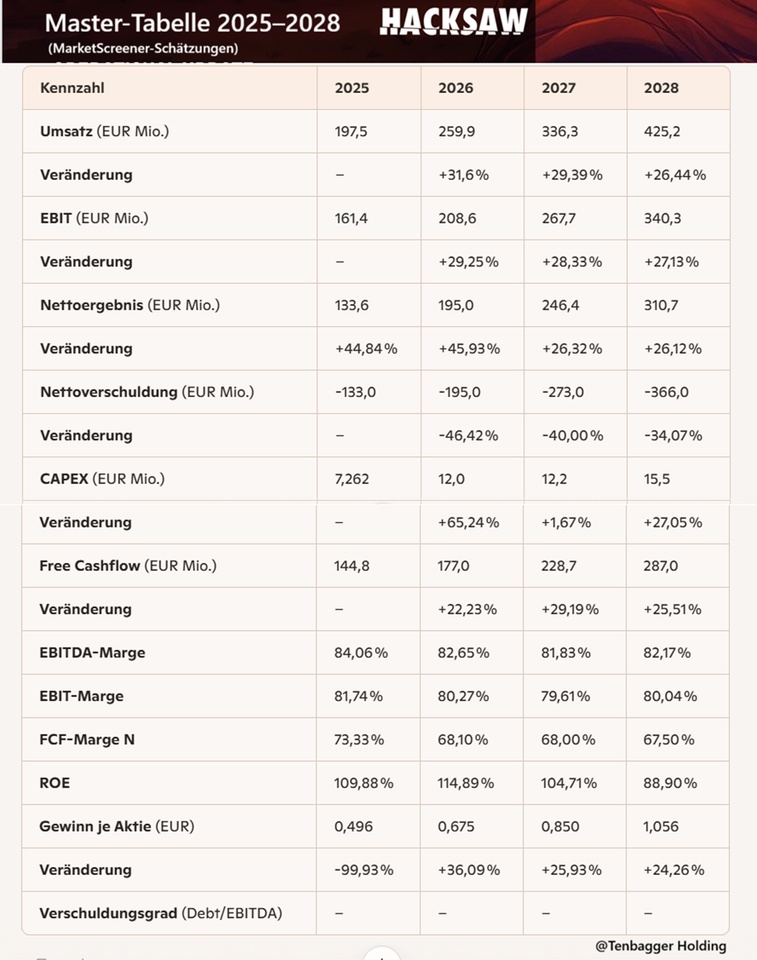

Juan's conclusion on the key financial figures

(Basis: MarketScreener data from your current tab )

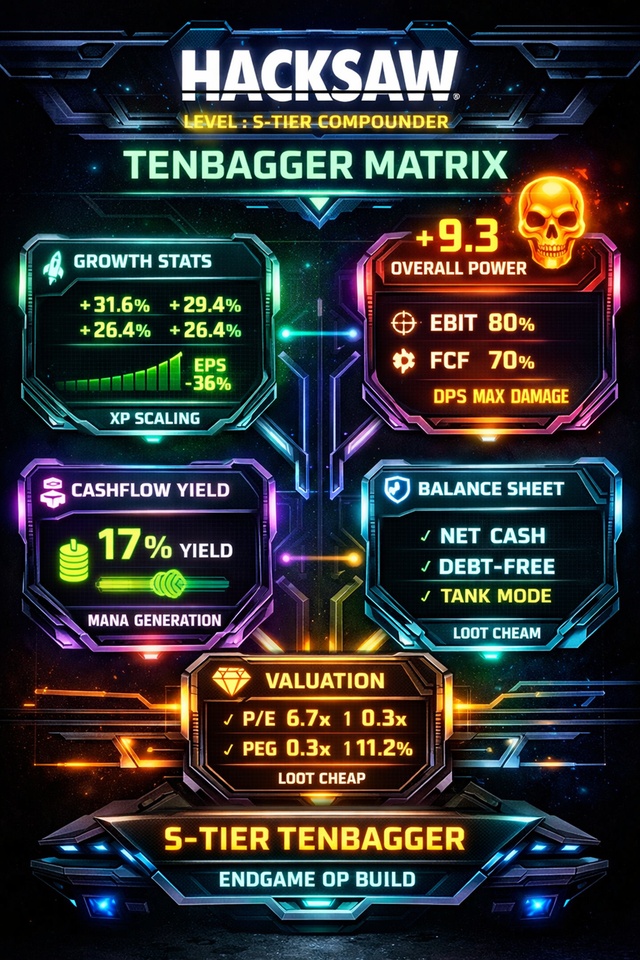

In a nutshell: Hacksaw delivers an extremely scalable, highly profitable growth model - with margins that seem almost "unrealistically good" in the software/iGaming world. The 2025-2028 forecasts show strong growth, rising cash flows, falling debt and an ROE that plays in the Champions League.

🔹 Juan's look at the figures for 2025-2028

1) Growth & scaling

- Double-digit sales growth every year - +31,6 %, +29,4 %, +26,4 %.

- EBIT increases almost in step - a sign of real operational scaling.

- Net profit grows even faster than sales → Model becomes more efficient.

2) Profitability at top level

- EBITDA margin 82-84 %, EBIT margin ~80 % → This is software premium class.

- FCF margin remains >67 % → Cash machine.

- ROE remains extremely high (88-115 %) - return on capital is exceptional.

3) Cash flow & balance sheet

- Free cash flow increases from 144.8 → € 287 million.

- Net debt becomes more negative every year → Net cash position grows massively.

- CAPEX remains low → Model is capital poor.

4) Per share

- EPS grows solidly: 0,496 → 1,056 €.

- The extreme -99.93 % change in 2025 is a base effect by the distorted 2024 EPS (758).

🔹 Juan's overall assessment

Hacksaw is a prime example of a highly scalable, high-margin digital model. Growth + margins + cash flows + decreasing debt = Quality profile at a very high level. If the momentum holds, Hacksaw will remain a top-tier compounder in the iGaming B2B segment.

Market value 2,052

Number of shares (in thousands) 289,196

Date of publication 17,02,2026

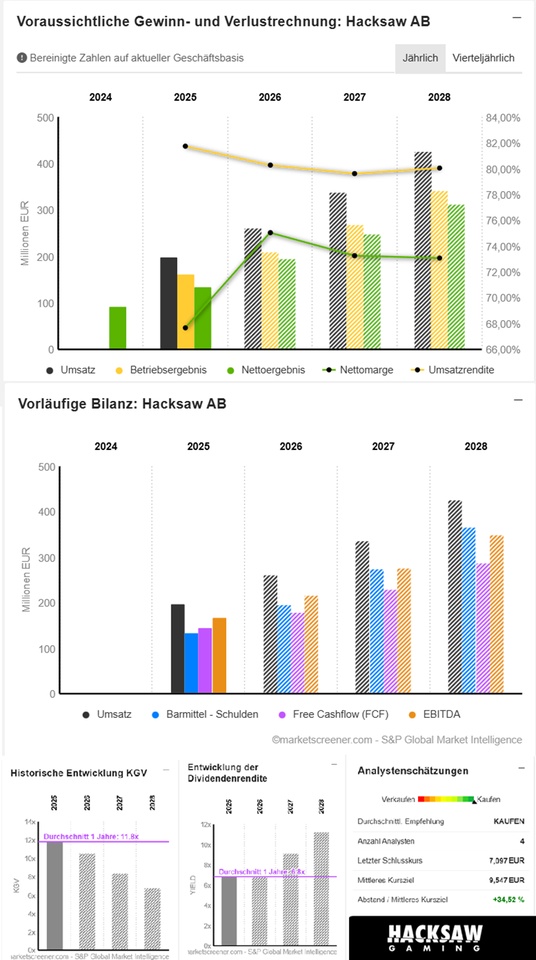

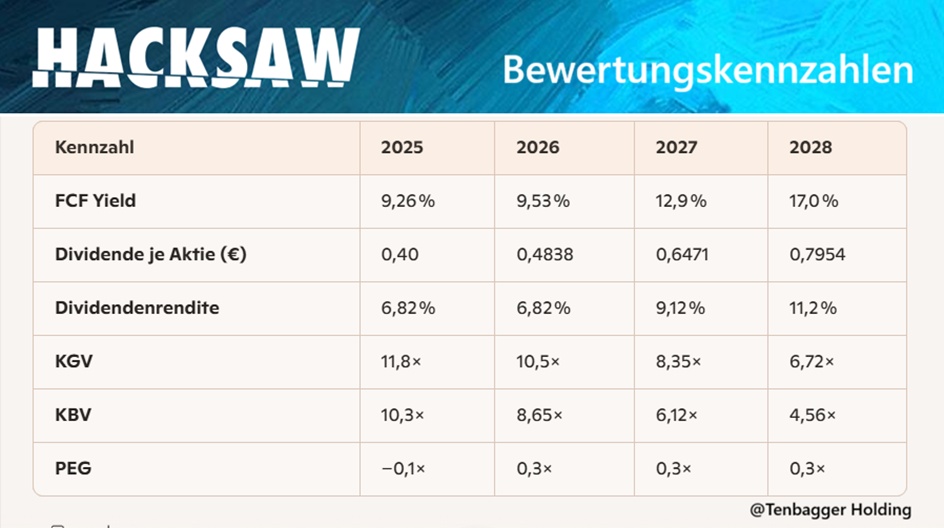

Juan's conclusion on the valuation ratios

(Basis: your current MarketScreener tab)

In a nutshell: Hacksaw looks like a quality stock that is simultaneously fast-growing and undervalued at the same time. The valuation metrics show a profile that typically only true compounders deliver.

🔹 Juan's view on the 2025-2028 valuation

1) FCF power meets attractive valuation

- A FCF yield of 9-17 % is exceptional for a fast-growing digital model.

- This means that the market is pricing growth growth far too conservatively too conservatively.

2) Dividend increases cleanly with

- Dividend per share grows every year → Shareholder return is steadily increasing.

- Dividend yield increases to 11 % → rare for a growth stock.

3) Multiples fall - even though the company is growing

- P/E ratio falls from 11.8× to 6.7× → Classic "multiple compression sweet spot".

- P/B ratio falls from 10.3× to 4.6× → Valuation becomes increasingly favorable relative to equity.

4) PEG shows clear undervaluation

- PEG by 0,3× → Market massively underestimates earnings growth.

- 2025 PEG is negative due to distorted EPS base effect.

🔹 Juan's overall assessment

Hacksaw combines growth, cash flow strength and falling multiples - a rare trio. The valuation ratios speak a clear language: The market is lagging operating reality. For Juan, this is a classic profile of an undervalued undervalued high-quality compounder.

🔶 Juan's conclusion (short & clear)

Hacksaw shows a valuation profile that rarely so clean clean: falling multiples, rising cash flows, growing dividends and an FCF yield that is expected to reach 17 % in 2028.

For Juan, this is a classic profile of a potential compounder with tenbagger DNA.

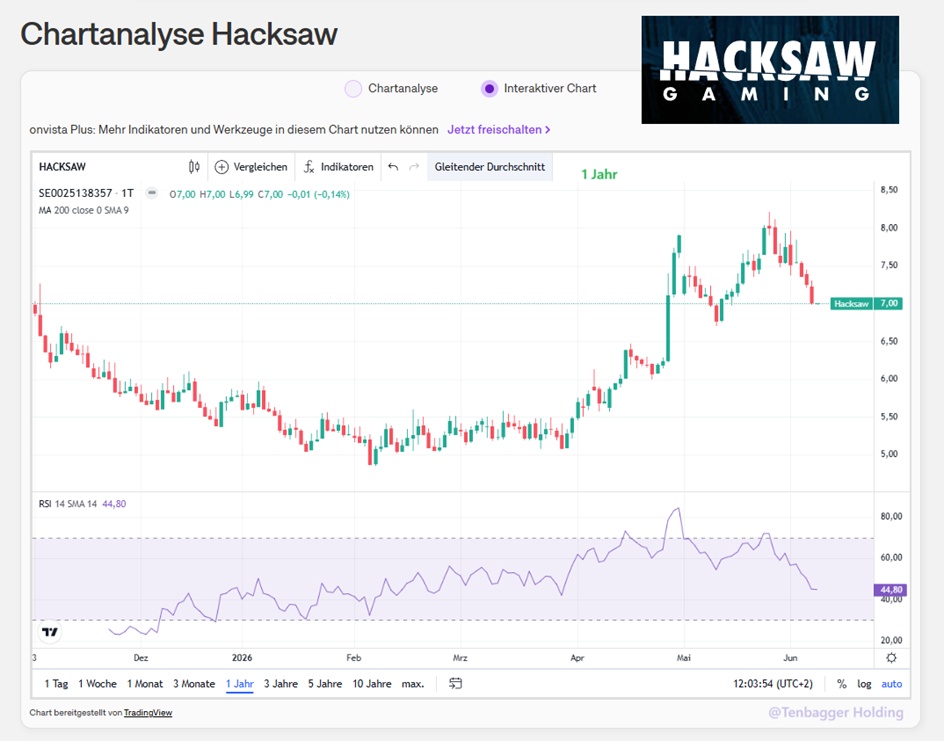

05.06.2026, 22:02:56 -

Tradegate BSX (EUR)

7.110 EUR