Hello my dears,

as my friends among the dividend investors usually get the short end of the stick when it comes to my company presentations.

Today I have a nice stock from our neighboring country, the Netherlands.

As a note, you should perhaps keep an eye on the debt.

However, it is being reduced, and I think a company with a 400-year history can assess this well.

But now we can start with $VPK (-0,49 %) .

I am particularly looking forward to the assessment of the value and dividend investors, who in my opinion are critical.

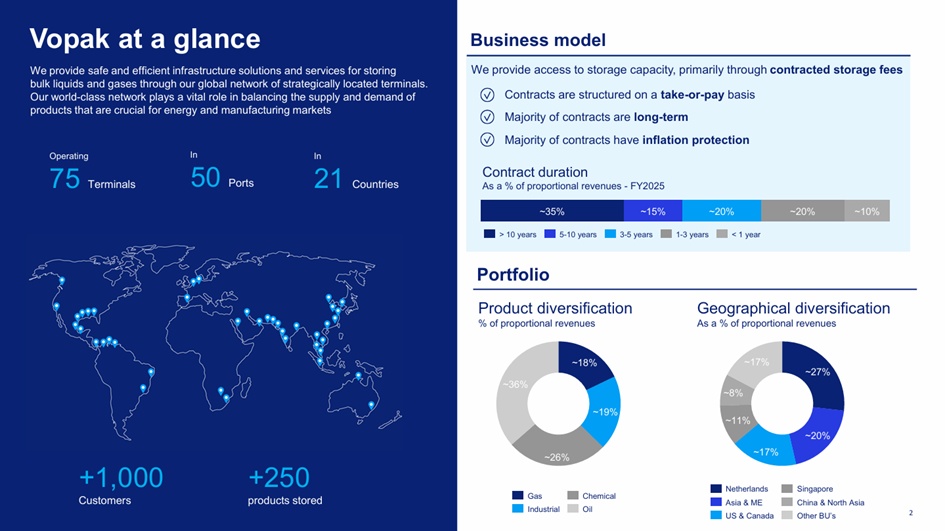

Royal Vopak N.V. is the world's leading independent tank storage company. The group operates a global network of terminals at strategic locations along the major trade routes. With over 400 years of history and a strong focus on safety and sustainability, Royal Vopak N.V. ensures safe, efficient and clean storage and handling of bulk liquids and gases for its customers. In this way, the group enables the supply of products that are vital to the economy and daily life, from oil, chemicals, gases and LNG to biofuels and oils.

Number of employees: 4,901

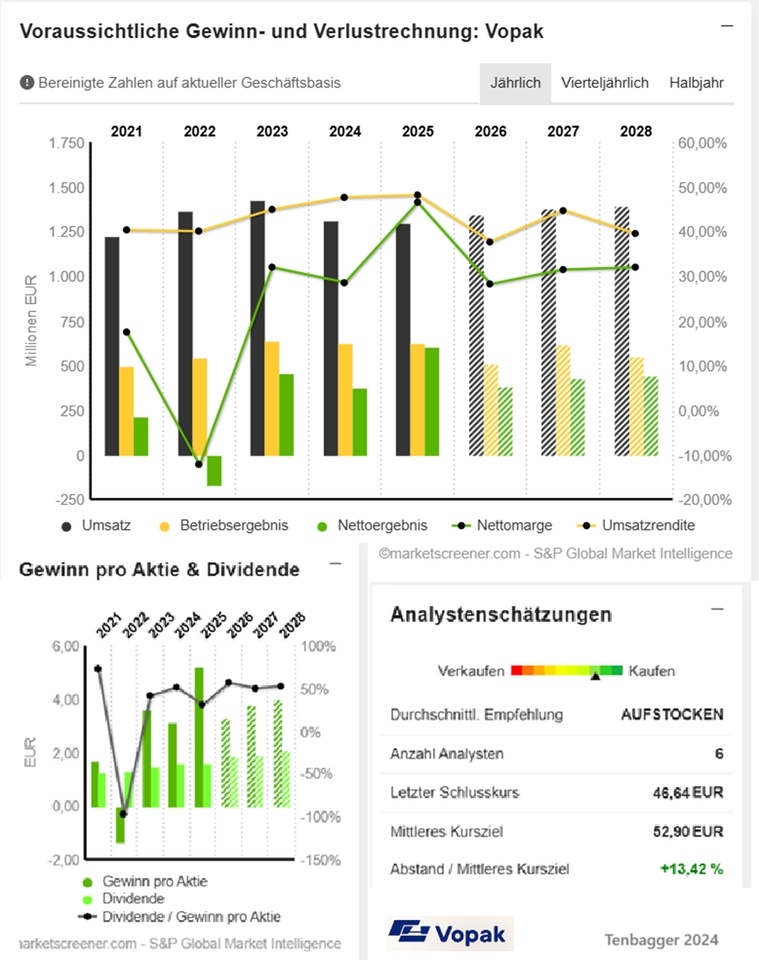

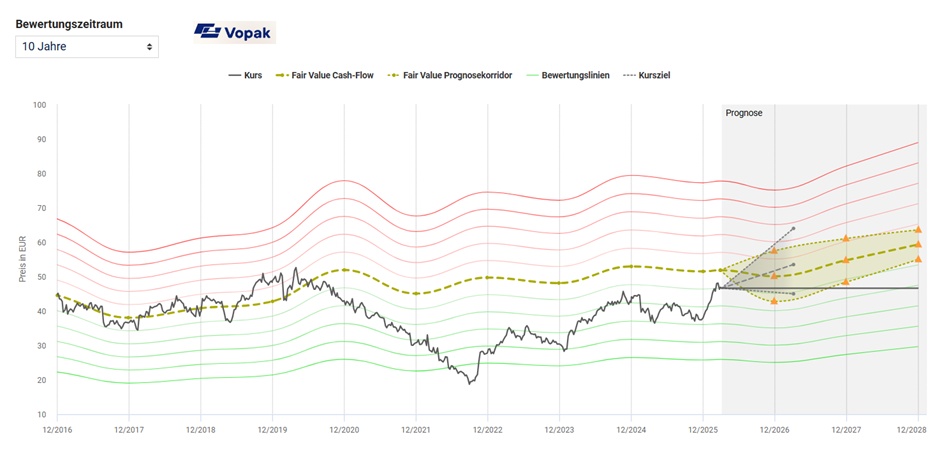

The key figure with the highest stability for the Royal Vopak share is the operating cash flowwhich is used below for the valuation. The KCV calculated from this key figure KCV (price/cash flow ratio) calculated from this ratio is 6.85 which is 0.76 points below the historical average of 7.61 for the last 10 years. From this perspective, the Royal Vopak share appears to be favorably valued to be favorably valued.

Multiplied by the operating cash flow per share of EUR 6.81 over the last 4 quarters, this results in a fair value of EUR 51.85 for the Royal Vopak share. fair value of EUR 51.85. The current share price of EUR 46.64 is 10.0% below this fair value, which corresponds to an undervaluation of the share.

📘 MASTER TABLE VOPAK 2025-2028

All values in € million, except per-share key figures and multiples.

1) Key financial figures

📊 Income statement, cash flow, balance sheet, profitability

2) Valuation ratios

💹 Multiples & valuation

Year Dividend Yield

2024 1,6 3,76 %

2025 1,6 4,22 %

2026 1,872 4,01 %

2027 1,896 4,07 %

2028 2,093 4,49 %

Market value 5,345

Number of shares (in thousands) 114,608

Date of publication 25.02.2026