After heavy losses Nemetschek has made an impressive comeback. Is this the start of a sustained recovery? How should the takeover of HCSS be assessed?

What's behind Nemetschek

Nemetschek is one of the world's leading providers of software for the construction and real estate industry. Around six million users worldwide work daily with solutions from the portfolio of the company's 16 brands.

The business model follows a compelling logic: anyone who designs, builds or operates a building needs software. And Nemetschek supplies it for each of these steps. The company is divided into four segments: Design, Build, Manage and Media.

In the Design segment, everything revolves around planning and architecture. Here Nemetschek offers software under the brands Allplan, Graphisoft and dRofus in particular in the area of Building Information Modeling (BIM), which architects, engineers and planning offices use to model and coordinate buildings in three dimensions.

This area accounted for 45% of the Group's business in the last financial year.

The Build segment (Build & Construct) focuses on the construction process itself. The solutions support construction companies in project management, collaboration on the construction site, document management and mobile and cloud-based applications.

The Bluebeam brand is the flagship here - a collaborative tool that is used on construction sites worldwide to check, comment on and approve plans.

This segment accounted for 40% of the Group's business in the last financial year.

A further 10 % was generated in the Media segment and 4 % in the Manage segment. However, the acquisition of HCSS will increase sales in the Build segment by around half, further reducing the weight of the two smallest Group divisions.

The Design and Build segments account for the majority of the Group's business.

Acquisition of HCSS calculated

The takeover of HCSS has been the dominant topic of late. At first glance, the valuation of HCSS might seem exaggerated, but in the end Nemetschek is putting comparatively little money on the table.

Nemetschek is taking over the debts of HCSS amounting to 450 million euros and will receive a new subsidiary in return, which will be integrated into the Build & Construct segment. In return, the previous owner, Thoma Bravo, joins Nemetschek and receives 28% of the Build & Construct segment.

The Build & Construct segment of the Nemetschek Group and HCSS have comparable and attractive growth and profitability profiles.

Last year, Nemetschek's Build & Construct segment generated sales of EUR 476 million and HCSS USD 215 million.

If the turnover is put in proportion, this corresponds exactly to the split of the deal of 72% and 28%.

The deal is fair for both sides. For Nemetschek and the new subsidiary, it opens up new growth paths, access to new customers and much more.

Outlook and valuation

The update on the first quarter of the current financial year is expected to be presented on April 30. We will then know for sure whether the positive trends have continued, which is to be expected.

In the last financial year, turnover increased by 23% to EUR 1.19 billion. Almost the entire business is now based on recurring income and is therefore easy to plan.

At the same time, profitability has improved, with the EBIT margin rising from 23.5% to 25%.

Profit climbed by 25% to EUR 217.2 million, or from EUR 1.52 to EUR 1.88 per share.

Free cash flow increased by 33% to 389.5 million euros.

Net debt was reduced from 294.6 to 107.5 million euros. Nemetschek was almost debt-free before the takeover of HCSS and should therefore be able to afford the deal without any problems.

Prior to the acquisition, revenue growth of 14-15% and an increase in the EBITDA margin from 31.2% to 32-33% were forecast for 2026.

This is in line with the consensus estimates, which predict a 24% jump in earnings to EUR 2.32 per share for 2026.

This puts Nemetschek at a P/E ratio of 28.4, compared to a long-term average of over 40. The same applies to the last few years

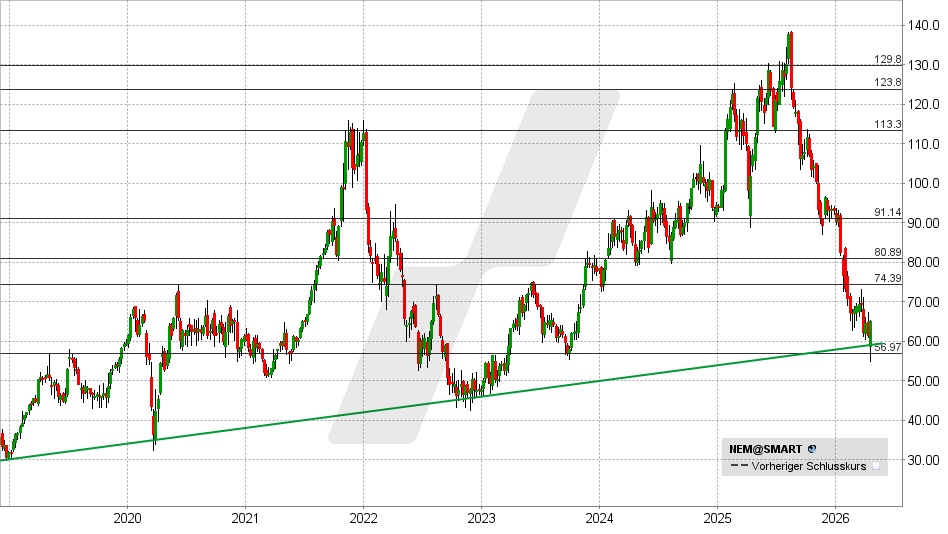

Nemetschek share: Chart from 17.04.2026, price: EUR 66.50 - abbreviation: NEM | Source: TWS

Nemetschek has recorded significant price losses and lost half of its value. However, the overall chart picture remains bullish, as the long-term upward trend is intact.

If a sustained rise above 66 euros is now achieved, this could trigger a recovery towards 70 or 74 euros. Above this level, there would be a procyclical Kaufsignal.

If, on the other hand, the share falls below EUR 57 at the end of the week, further losses towards EUR 45 must be expected.

Source